Supreme (FIRE.T) is an office darling for a few reasons, but none more so than the fact it’s a company you can be proud recommending to friends and family. I know I am.

The company’s mission statement is sustaining disciplined growth while delivering high-quality products. Disciplined growth. The wingbeats of cherubs never sounded so sweet.

Listen, I don’t mean to be gratuitous but I will–you’ll understand why when I break down the company’s balance sheet.

Let’s talk products first. The company’s Khalifa Kush Enterprises line of oils are named after the Grammy-nominated recording artist and Pittsburgh native, Wiz Khalifa, an avowed cannabis enthusiast.

Khalifa’s Khalifa Kush line, though only available in the U.S. and not a Supreme product, is highly popular wherever it’s consumed, but don’t just take my word for it.

Being a lifelong cannabis aficionado, Khalifa only smokes the best and it’s safe to assume he only wants his name on the best products. And Supreme wants to compete with the big boys, a goal assisted by the flattening effect Canada’s ban on advertising has on the sector.

And since Supreme is to be the exclusive distributor of Khalifa’s branded products within the Canadian and international markets besides the U.S., I have no doubt those products will be just as popular.

What’s more, Supreme paid a total of $9.2M for the rights to manufacture and distribute these products through a combination of cash and shares.

The fundamentals: disciplined growth

In Q2 2019, Supreme had a net revenue line of nearly $10M, up five times from the same period in 2018.

Granted, recreational cannabis wasn’t legalized until Q4 2018 so it’s not like Supreme became five times better, but the key here is responsible growth.

Ultimately, this is a ‘growth by any means’ strategy and, if I was an ACB shareholder, I’d be on the next earnings call asking management to justify why I’m footing the bill for their purchases.

Here is an example of irresponsible growth by industry leader Aurora Cannabis (ACB.T) to put Supreme’s accomplishments in perspective:

In 2018, Aurora “issued approximately 69.3 million common shares and paid approximately $134 million” for CanniMed, acquired Whistler MMJ “in an all-share transaction valued at up to approximately $175 million and acquired MedReleaf “in an all-share transaction valued at approximately C$3.2 billion on a fully diluted basis.”

Instead of slowly building revenues as a way of affording M&A–I would’ve even accepted a revolving credit facility–Aurora just printed more shares, watering down shareholder value. This isn’t inherently bad, but Aurora now has triple the share count of Canopy Growth (WEED.T) as a result.

Ultimately, this is a ‘growth by any means’ strategy and, if I was an ACB shareholder, I’d be on the next earnings call asking management to justify why I’m footing the bill for their purchases.

Not to crib too much from my previous work, but this next part of Aurora’s release about the acquisition of Whistler MMJ really needs to be seen to be appreciated:

Management is in the process of gathering the relevant information that existed at the acquisition date to determine the fair value of the net identifiable assets acquired and liabilities assumed. As such, the initial purchase price was provisionally allocated based on the Company’s estimated fair value of the identifiable assets acquired and the liabilities assumed on the acquisition date. The values assigned are, therefore, preliminary and subject to change. Management continues to refine and finalize its purchase price allocation for the fair value of identifiable intangible assets, property plant and equipment, and goodwill.

I don’t mean to be a bad-faith actor, but I can’t help but interpret this as ‘we didn’t do our homework so we’ll figure our this asset’s value later.’

Again, share-based acquisitions aren’t inherently bad as you’ll see–Supreme has done their fair share–but billion dollar companies have options besides diluting shareholder value.

Supreme isn’t a $10B company, it’s a $400M company with a lot of room to grow. We know that because, although it may seem like it does the same things as cannabis giants like Aurora and Canopy, there is a slight but important difference: Supreme isn’t riddled with debt.

The acid test, or quick ratio, is a good little metric to judge a company’s exposure in the case of an emergency.

A 2:1 quick ratio means a company has twice the on-hand liquid assets necessary to take care of their liabilities should they need to. A 4:1 quick ratio means a company has enough liquid assets to cover their liabilities four times over. Supreme’s ratio is the latter.

Now let’s go over property plant and equipment (PPE). Supreme has increased is PPE by over 50% since Q2 2018 from $101M to $166M. The company’s production capacity will soon by 50,000 kilograms per year once their 440,000 square foot facility is fully built out.

Then there’s Lesotho-based Medigrow which will be producing inexpensive oil for European markets and Blissco, the B.C.-based and eco-friendly extractor. Supreme has their plan for world domination set out.

And they aren’t burning through share capital to do it: Supreme has more cash on hand now than they did in Q2 2018 ($75M vs $56M).

So that’s the good. The not so good, and there’s always something, is the convertible debenture which matures on Nov. 14, 2019.

Supreme raised $40M in November 2017 through unsecured debentures which convert at a price of $1.60. But while that’ll cause some share dilution, it’s a one off.

The good:

- Goodwill and intangible assets make up an insignificant amount of their asset line compared to Canopy and Aurora

- High-quality, premium offerings which compete with the big boys

- Increasing revenue

- Impressive quick ratio

- Trading at a world-class 10X P/S multiple

The ‘meh’:

- Convertible debenture coming up.

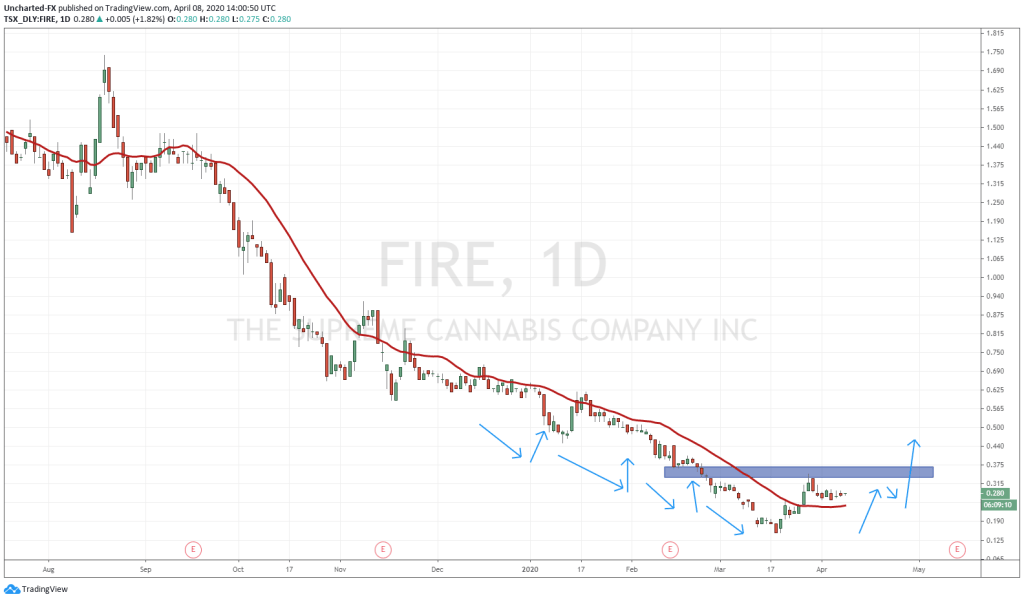

- If you’re looking for a bottom, you might be waiting a while

Sold yet? The market seems to be. Supreme is up 12.3% today. We think it’s a go.

–Ethan Reyes

Full disclosure: SUpreme Cannabis is an equity.guru marketing client.