Cannapocalypse: Version 2

I think Canopy Growth ($CGC) and Aurora Cannabis ($ACB) should notify the makers of the Oxford English Dictionary that the word “earnings” has been redefined to mean “losses”. Both firms have been supposed “leaders” in the industry, and have let stakeholders down in the past quarter.

My disappointment in these two companies isn’t rooted in the fact that they took losses – that’s a part and parcel of any new business venture – but that both firms have failed to forge something essential for good business: a vision delineating a clear path to profitability.

Aurora Cannabis

- Net revenue: CAD $75.2 million, below estimated o CAD $90.6 million.

- Sales in recreational markets tumbled 33% to CAD $30 million.

- Adjusted Loss: CAD $39.7 million, expected CAD $20.8 million.

So much for a company who in the very last quarter said that it “continues to track toward positive adjusted Ebitda,” citing “near-term challenges to achieving positive adjusted EBITDA.”

Aurora also added that it has reached an agreement with investors who hold CAD $155 million of its March 2020 convertible debentures to convert early at a lower price. Simply put, if you were an investor, good luck holding the bag.

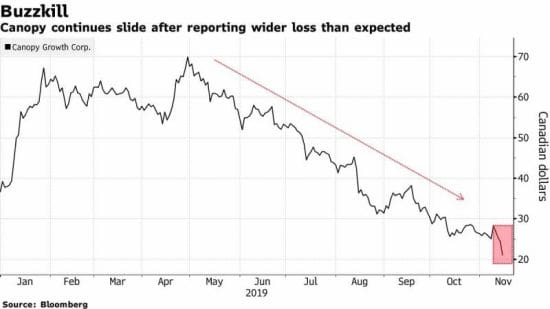

Canopy Growth

- Net revenue: CAD $76.6 million, below estimated o CAD $102.3 million

- Adjusted Loss: CAD $155.7 million, expected CAD $96.1 million

- $CGC harvested ~40,000kg of flower but sold ~11,000 kg

Constellation Brands ($STZ) is a major stakeholder in the company and is already underwater on its stake. The Corona maker must ask itself whether cannabis will make a comeback or if it’s time to chop off the arm to save the body.

The one thing that cannabis companies didn’t account for is that legalisation didn’t necessarily mean that suddenly every consumer would start using pot, but rather, that individuals who were already consuming product would now walk into a store or order online instead of calling their “dealer”.

To make a profit, firms must either cut costs or boost revenues, or do both. Given that large scale infrastructure is required to set up a factory, and extensive regulatory approval is required to produce cannabis, land and factories are either fixed costs or sunk costs.

Canopy might have the highest revenue per gram in the business, but if it’s sitting on thousands of kilograms of flower that it can’t sell, it’s time to either expand to international markets or find a way to fund the resurgence of the ‘70s era hippie movement.

It’s time industry players took a step back to rethink the “growth at all costs” strategy when aggressive spending is coming back to haunt them. The firms think they can club together $32 million dollars worth of returned product and call it a “write-down”, but we’re watching, and here’s the post-mortem.

Walmart ($WMT) Earnings

One of the ways a hedge fund analyst decides to make money is by looking at the historical financial data of a company’s earnings and making growth assumptions about costs, revenues, and profits, to engage in a discounted cash-flow analysis to arrive at a present value of a company. Then, they would make trading decisions on the basis of that investment analysis.

If you’d like to be more sophisticated, you’d like to go a level deeper to justify your growth assumptions. Why you should assume growth at 5% instead of 3%, 10%, or even 3.247%? These are complicated questions and there is no blanket answer to solve the pressing problem of valuing a company precisely.

It is a truth universally acknowledged that a hedge fund in need of a trading idea will look at satellite data of a Walmart parking lot to see how good the quarter will be. I’m sure someone must have looked at all the cars in parking lots in the past quarter, and gone – “more cars mean more customers mean more profits”. The firm reported earnings today and here are the stats:

- Earnings per share: $1.16, adjusted, vs. $1.09 expected

- Revenue: $127.99 billion vs. $128.65 billion expected

- U.S. same-store sales: up 3.2% vs. growth of 3.1% expected

This is an earnings report that shows the firm made money, matched estimates, and raised its forecast before the holiday season. Despite these results, the stock traded down towards the end of the day as investors showed concern about Walmart’s rising costs of new initiatives and slow growth in diversifying sales.

Powell: “We have it under control”

Federal Reserve Chairman Jerome Powell suggested that the reserve’s enterprise of “not QE” is working as expected, and that interest rates are back under control.

The Fed has been injecting billions into the money markets since September 17, when the overnight interest rate jumped to 10% from around 2%, signalling a liquidity crunch. Fed’s response was to buy treasure bills to add reserves into the system. While this may have calmed the repo rate crisis, it also signalled to some investors that this was disguised quantitative easing, and just because you don’t call it that doesn’t make it so.

The Fed is yet to go a few more rounds to conduct repo operations in the coming month. In the midst of a trade war that is about to be done and dusted, Powell assured the markets that things in the money markets are under control.

A reporter asked the chairman for comments about Trump’s direct comments on the operations of the reserve. Even though Powell declined to respond directly, he asserted that it’s important for everyone to know that the Fed’s work is done on a “nonpartisan, nonpolitical basis”.

Powell is a lawyer by training, and his statements are somewhat along the lines of “we neither confirm nor deny” that we have a long term plan to solve the repo crisis. Fed’s policies seem to be working, for now. Unless, you know, the trade war lasts for twenty years(?) as Jack Ma believes, and we have hyperinflation.

What we’re talking about

- Canopy Growth ($WEED.T) financials are catastrophic, $74m loss, $32m in returned product/writedowns

- Delta 9 Cannabis ($DN.T) keeps moving quietly towards profitability

-

ePlay Digital’s ($EPY.C) Big Shot mobile basketball game set to advertising revenue mode

-

Isracann Biosciences ($IPOT.C) gets an operations project roadmap for production