Here at equity.guru, we see the way things are going. Weed stocks are trending down, so we want to highlight companies poised to succeed in the long-term (*cough Cannabis 2.0 *cough).

Heritage Cannabis Holdings (CANN.C) is a company which hasn’t gotten the love it deserves lately, and that’s bad.

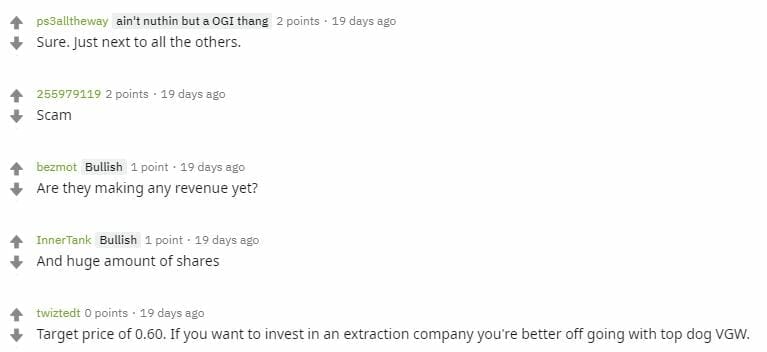

Just look at some of the nasty things those Reddit Debbie-downers have been saying about the upside of Heritage’s $35M deal vaporizer supply with Cronos Group (CRON.T).

I’m sweet on Heritage, so let’s address these concerns point by point:

- Although there are plenty of deals being signed in the sector, Heritage has a clean-as-can-be balance sheet with almost no debt and no convertible debentures to be found;

- “The word I’m searching for, I can’t say because there’s preschool toys present;“

- The company has been pre-revenue until now, but I have a feeling the next round of financials will silence the naysayers;

- This is largely psychology–fundamentals outweigh whether or not a stock ‘looks cheap’ due to dilution;

- I see more upside, and likelihood, of CANN going from $0.24 to $0.60 than VGW from $3 to $6.50.

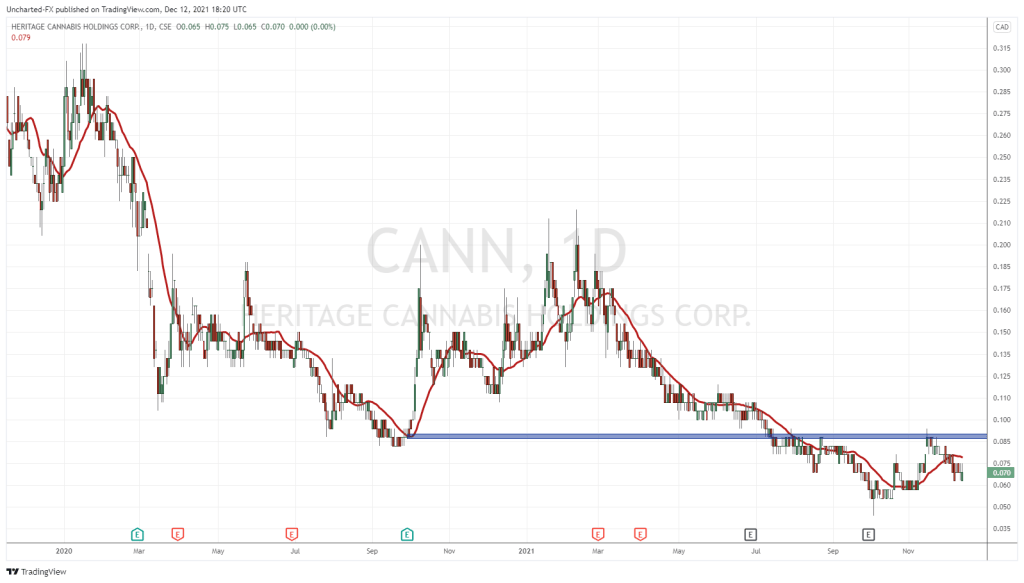

Down from its year-high of $0.72, Heritage stock is far from overbought. But it’s shed about as much as the rest of the sector has since the bloodletting started in March.

But the company has been ahead of the curve on a few things, and I wasn’t trying to blow vape up your a** when I said the company had a strong balance sheet.

Clint Sharples, CEO, said CANN was even better capitalized than it was according to its latest financials, which listed $13.5M in liquid assets against $4.8M in total liabilities.

Quick ratios are a metric used to determine a company’s ability to cover its liabilities. With a quick ratio of 2.8, CANN is in good shape. This information is out of date anyways: Sharples said his company has enough capital to sustain themselves until the end of 2020 even if they don’t earn a dime all year.

But Sharples said the money has already started rolling in, all thanks to the company’s pivot away from the square footage-focused insanity which dominated the cannabis market of yester-year.

Heritage’s management saw the landscape, noticed everyone pumping out news releases about expansions here and build-outs there, and did some math on how much cannabis the top 25 LPs would be producing once finished construction.

“When we took an honest look at it, we came to a number eight to 10 times, on a conservative basis, would be produced more than would be consumed,” Sharples said.

So they acquired Purefarma Solutions, a highly-experienced cannabis extractor in late 2018 which has won the High Times Cannabis Cup for its concentrates.

Devin Schilling, a PI Financial analyst, called Purefarma one of the most experienced companies in their field.

Then, CANN got to work signing deals, and they’ve been busy on that front.

The company announced a supply and contract manufacturing agreement with Sugarbud (SUGR.V) to “provide extraction, formulation and production services to Sugarbud for the development of pre-filled vape cartridges, utilizing proprietary additive-free formulations.”

While contract size details were not disclosed, Schilling estimates the deal could be worth between $5 and $10 million per year to Heritage depending on the roll-out and uptake of vape pens in Canada.

–Cantech Letter

CANN also announced a supply agreement with Cronos Group in July valued at $35M. They also announced a processing and supply term sheet with Canntab Therapeutics (PILL.C). Then they did one with Zenabis (ZENA.T). Then there’s their JV with Empower Clinics (EPW.C) to set up extraction operations in Oregon.

In the short term, Sharples said his company is going to have its hands full white labeling products for companies like Cronos. That takes them solidly into Q1, ending January 31, and the rest of the year will be growing the company’s revenues as their capacity grows.

Revenue is already trickling in, according to Sharples, and with Cannabis 2.0 right around the corner, now is the time to be thinking about the companies poised to take advantage of a new market–and a renewed enthusiasm about cannabis stocks.

Especially one with an award-winning team like Purefarma to its credit.

Sharples said, although he was personally troubled by the spate of vape-related deaths, he wasn’t worried about blowback hurting his company’s prospects.

“We would favour an overly-regulated market only because it’s better for our business. Because of our vape technology, we are able to put out a product that has zero additives in it where our competitors aren’t.”

Sharples said he was confident saying that, in part, because CANN is currently going through its hemp supply with a fine-toothed comb.

Rosy Mondin, CEO of World Class Extractions (PUMP.C), told EG that one of the major issues facing hemp growers was an inability to properly store CBD flower.

Pesticides and mold are just two issues which toll processors have to deal with: storing CBD outside leads to mold whereas concentration of biomass can put acceptable levels of pesticide over acceptable limits. CANN said they’ve found a workaround.

“What was a very slow CBD production for us how now accelerated quite a bit as we’ve solved the issue here in Canada,” Sharples said.

Look, CANN isn’t a pumper. Sharples said the company isn’t going to put out news releases saying all his employees showed up for work today, and, frankly, he shouldn’t.

But the company is out there signing deals and rolling up their sleeves. Yes, they’re pre-revenue, but look at your favourite loss-magnets out there. Revenues are keeping steady with losses because we got out in front of our skies a little bit.

Heritage has a clean balance sheet, cash-on-hand, no debt and is well-positioned to hit the ground running on concentrates here and in the U.S.

We think Heritage Cannabis is undervalued.

–Ethan Reyes

Full disclosure: Heritage, World Class and Empower Clinics are equity.guru marketing clients.