Two things have changed about Canadian dinner parties over the last few years.

Two things have changed about Canadian dinner parties over the last few years.

The first is, people are less inclined to bring a sassy red and more inclined to bring edibles.

And the second thing is, everyone’s going to Portugal.

Like, everyone. They’re digging the food. They’re digging the history. They’re digging the view.

And they’re digging – literally – the copper and gold.

Karim Rayani liked the joint so much he moved his family there and bought a bunch of historic producer mine projects that North Americans had long forgotten about.

“It’s pretty great out there, but the thing folks forget [about Portugal] is it’s an incredible mining jurisdiction. In 2019 it was considered the 5th best spot in the world to build a mine,” he tells me. “So I went through the data and found some really special locations,” he adds.

He ain’t lying. Rayani bought a bunch of old mines on some beautiful land.

And when I say a bunch (technical hats on, friends):

Borba 2 Copper Gold Projects: The Borba 2 exploration license spans an area of 318 square kilometers and includes several past-producing mines with significant copper and gold findings. It features historic mines and new targets that promise copper and gold mineralization. These include:

- Miguel Vacas Copper Mine (Borba 2): Miguel Vacas is a historical copper mine that ceased operations in 1986 but left behind promising high grades of copper averaging 1.2-1.4%. The mine has shown significant potential through near-surface drilling results, indicating robust opportunities for redevelopment and mineral extraction.

- Mostardeira Copper Gold Project (Borba 2): Located near Estremoz, this project includes a copper-gold mine historically mined for high-grade copper along a significant shear zone. Recent sampling has shown high-grade intervals of gold and copper, suggesting substantial untapped potential in the region.

- Almagreira Gold Project (Borba 2): The Almagreira Gold Project is characterized by gold epithermal mineralization within altered volcanics and carbonates, indicating a substantial mineralized structure. The project remains open for exploration, with potential extensions along strike and at depth.

- Bugalho Gold Copper Mine (Borba 2):This project features primary and supergene copper mineralization along with significant gold occurrences, located within quartz-carbonate breccia matrices. The high-grade mineralization demonstrated in dump samples underscores its prospective value and exploration potential.

And if that’s not enough for you, there’s more:

Barrancos Projects (including Aparis Copper Mine and Lirio Gold Project): The Barrancos properties cover 74 square kilometers in south-central Portugal and include the Aparis Copper Mine, a past producer with an extensive vein system and significant historical copper grades. The Lirio Gold Project, part of the Barrancos area, shows potential as a significant gold system with historical high-grade gold and copper intersections indicating a large-scale mineralized system.

I know, y’all aren’t keeping up, so let’s break this down in layman’s terms.

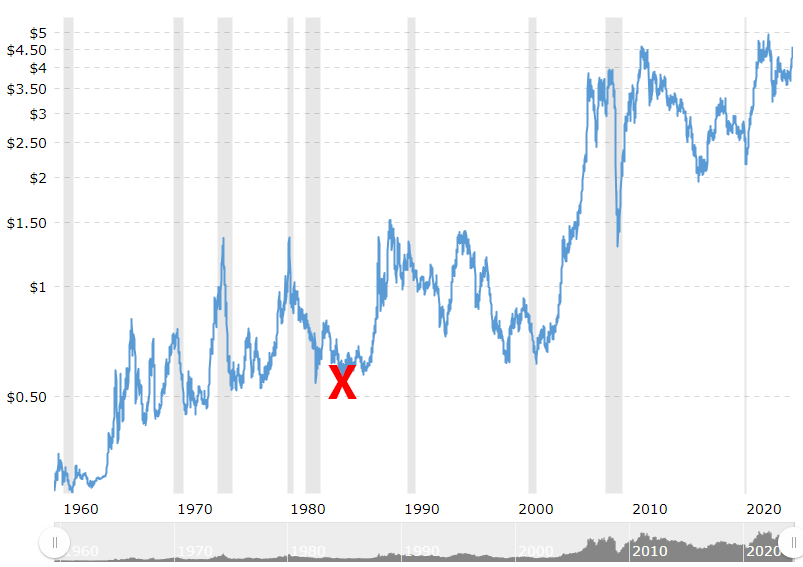

Back in the day, when copper was a lot cheaper, this mine was producing for its owners, but eventually it became uneconomic (see the red X below) and they shelved it.

When copper was sudenly less attractive following a drop off in prices, according to Rayani, a long line of explorers came to test the property as a gold resource.

“The Rio Tinto group explored the area for epithermal gold deposits during the early 1980s. They were followed by Carnon Holdings Ltd. in the early 1990s, by Auvista Minerals during a few years between 1996 and 1998, then by Rio Narcea Gold Mines in a joint venture with Kernow Resources (2005 to 2007) and more recently by Colt Resources until 2017.”

The gold push didn’t bring fruit, but along the way it seemed like everyone forgot the girl they came to see originally.

Copper prices have evolved in the 35 years since.

The $0.60 per lb of the early ’80’s is a whopping $4.56 today.

SO LET’S GO GET SOME.

On the Miguel Vacas project, there’s a non-compliant internal resource estimate from back when production was happening that looks tasty, if you believe in the numbers.

-

- Oxide Ore: Approximately 1.2 million tonnes with an average grade of 1.23% copper, located from the surface to a depth of 80 meters.

- Sulphide Ore: Estimated at 4.4 million tonnes with an average grade of 1.24% copper, extending from 80 meters to 250 meters depth.

Getting a decent grade wasn’t easy back in the day – initial grades were around 0.7%, which is poor, before the miners finally zeroed in on a much tastier 1.4%.

To be clear – any copper grades of more than 1% over 100m are considered high grade, so Rayani’s job here isn’t so much to pull the handle on the resource slot machine and dive into the unknown, but reinforce what he already knows, modernize that resource estimate, fill in the spaces between some holes, and move forward quickly now that the price of copper is on the upward move.

Of the historic drilling, the highlights include:

- Hole MV04:

- Copper Grade: 0.79% Cu

- Width: 6.00 meters

- Our Classification: Decently economic, as the grade is between 0.3% and 0.5%, and the width is above the minimum 5 meters we require for economic indications on the hole.

- Hole MV05:

- Copper Grade: 1.72% Cu

- Width: 2.00 meters

- Our Classification: High grade, as the grade is greater than 1.0% but the width does not meet the minimum 5 meters we require for to call a hole a Bonanza grade.

- Hole MV10:

- Copper Grade: 1.47% Cu

- Width: 6.40 meters

- Our Classification: Bonanza hole, as the grade exceeds 1.4% and the width is above the minimum 5 meters we require for a hole to be considered a beauty.

Again though, all of that is non-compliant historic data. The drillers may have been drunk, you don’t know.

So, as an investor, what you’d ideally want is for CEO Rayani to get with the drilling ASAP and make that historic data new again.

During the next two seasons, Europacific Metals plans to conduct a robust exploration project on the concession. This will include geological mapping and rock-soil sampling, as well as induced polarization and/or electromagnetic over selected areas. Miguel Vacas will be a primary target and a plan has been made to start a drill program involving 1,000 m of drilling.

To be even more precise:

“Eleven holes are now being planned to confirm the extensions and quality of the oxidized blanket amenable for an open-pit heap leaching operation. The immediate goal is to come to market with an initial resource estimation — which, if confirmed may enable a successful operation in the short term while the sulphide parts of the system are assessed by deeper drilling at a later stage.”

That’s actually EXACTLY what I’d want out of this collection of projects. You’ve got all the upside of that massive land package for down the road, and the question of ‘what lies beneath’, but in the short term, let’s bang out a resource on the shallow stuff that shows exactly what’s verifiable, and hey – if it looks good, maybe even get the production going again.

And, if we trip over a little gold along the way, prices on that aren’t terrible right now.

In fact, there’s a decent sized local community of marble extractors in the area, which means mining equipment is readily available as needed, which only adds to the ability to move quickly.

Just to repeat: The Miguel Vacas is just one of the projects in the grab bag.

Oh. And the market cap on this collection of Euro copper targets?

$2.3 million.

Volume rolling.

That’s all.

— Chris Parry

FULL DISCLOSURE: EuroPacific Metals is an Equity.Guru marketing client and we will likely be buying on dips.