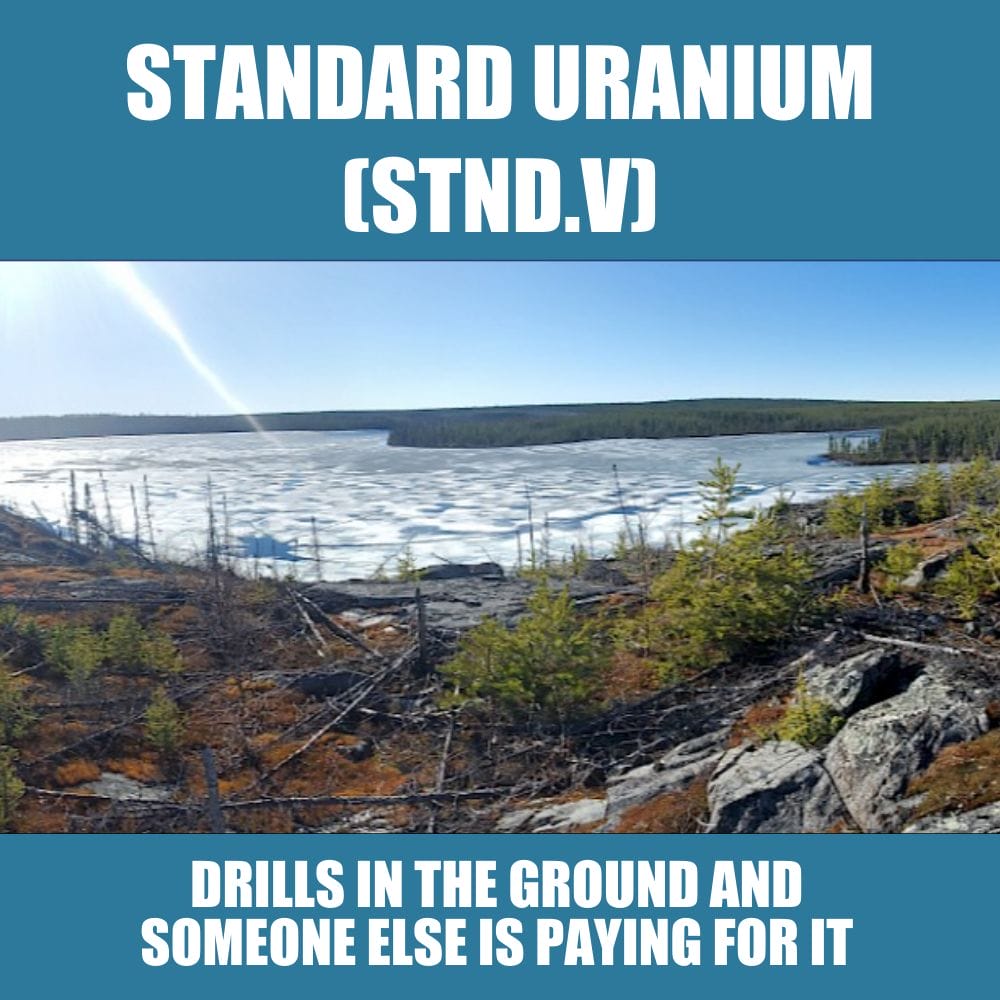

The heart of Northern Saskatchewan’s eastern Athabasca basin is a cold, desolate place. The crusty ground crunches under foot, even when the snow isn’t two feet thick. The greenery would be more aptly described as brownery.

There are no mountains in the distance to stop you getting turned around and, while there are people about, they’re generally sparse, sore, overworked, living in tents and, at this time of year anyway, fighting back the icy chill of the tundra.

This is not a place you go to kill time. This is a place that takes feeling out of your fingers and months off your life, months freely traded in the hope they’ll be one day exchanged for treasure.

And when you turn on the spectrometer, a device for measuring nearby radiation, a clue as to why there’s not a lush thick forest all over the landscape and why those tired, sore, grumpy men have gathered here can be quickly detected.

This joint is just a bit radioactive.

Standard Uranium (STND.V) does business here.

18 months ago, Standard was in peril.

A particularly odd winter, where temperatures swung wildly from overly warm to overly cold several times, saw the ice shift enough to break STND’s only drill, right in the middle of an all-or-nothing drill program at the company’s all-or-nothing project.

It was devastating. The share price plummeted. Their market cap was into dangerous territory. The company was on a knife edge.

The core group met to figure out their options. Bigger companies were sniffing around, trying to headhunt their technical staff. The uranium sector, and the resource world in general, were not booming.

The easiest move would have been to walk away. Most people would have walked away.

I told CEO Jon Bey at the time, “Nobody will complain if you peace out. You should probably peace out. But if you turn it around, you’ll be a legend. If you even bother trying to make it right, people will notice. People will know you as a guy they can deal with. You’ll wear that win a lot longer then you will any loss.”

At the recent Vancouver Resource Investment Conference, Jon Bey was walking the room proudly, knowing that – sure, he scraped bottom – but he’s built back, in rapid time, from a company with one project that didn’t happen for him to a company with ELEVEN projects, with five planned drill programs in 2024, including four joint venture earn-in partnerships on their Sun Dog, Canary, Atlantic and Ascent projects, totaling over $31 million in work commitments over the next three years.

Bey kept his technical guys, in no small part because they believe in the company, and they believe in him. Standard has fostered a team culture that has them all fighting for each other, all rowing hard in the same direction, deferring personal opportunities in the belief that if they can just keep the band together, they’ll get their due rewards.

But how good is that technical team exactly?

This good.

The Atlantic project, spanning 3,061 hectares on the east side of the basin, is strategically located due west of IsoEnergy’s Hurricane Zone. The project was acquired via staking in March 2019 and the optionee, Atco Mining Inc., wants to earn a 75% interest in the project over three years through work performed.

But they know uranium projects require a special kind of know-how and experience, so they forged an agreement with STND to come in and do the work, in return for a percentage of expenses and a 2.5% NSR (net smelter royalty) on the project going forward.

That journey began on February 26th, as Standard Uranium’s geological team, led by President & VP of Exploration Sean Hillacre, set drills to pierce the tundra and explore high-priority targets. The Atlantic project’s drill program will run approximately 2,000 to 3,000 meters across four to six drill holes, looking to uncover high-grade uranium mineralization.

In essence, Standard gets to spend zero dollars on the project, has their exploration work paid for, cuts 10% off the top for themselves, and down the road that 2.5% NSRT could be a dandy earner for a long time.

- Market slow? No problem.

- Tough to raise money? No problem.

- Exploration costs high? No problem.

- You want STND’s exploration team to trample snow on your project? PAY THEM.

That’s just one project. There are TEN others.

The significance of Standard Uranium’s exploration efforts extends beyond the borders of the Athabasca basin. It represents a broader trend in the uranium sector, which is experiencing a firming up of investor interest. As the world increasingly turns to nuclear energy as a reliable and clean energy source, the demand for uranium is expected to rise. as it has been doing all year. This upswing in the nuclear energy sector is not just a phase—it’s the beginning of a major shift towards sustainable energy solutions, and STND is showing that they’re not a case of ‘all hat, no stirrups’. They’re not here for show. They’re not oly doing the work, they’re doing it at another company’s expense.

For investors, the activities of Standard Uranium and the overall trends in the uranium sector offer a compelling narrative. As the company continues to defy expectations with its ambitious exploration projects, it highlights the potential for significant returns in the uranium market.

In fact. I’m giving it one of these:

— Chris Parry

FULL DISCLOSURE: I’m conflicted up and down here. I own it. They’re a client. I’ve bought more shares on the open market. I’ve known Jon Bey for half a decade and consider him a top flight dude. Do your own due diligence and set them on your watchlist. If you’re looking for a microcap uranium play that has shown its work and never quit, by all means.