We start off this round up with something that hits close to home. On Monday, I had to head out in the crazy rain storm here in Vancouver and the Lower Mainland. I was heading down the local street with my wipers on full speed. As soon as I got close to the intersection, I saw a view that I thought I would never ever see. Now I live on a high hill, so I was driving downhill. At the bottom of the hill is the intersection, and what greeted me was a do not enter sign, with a vehicle half submerged under water. Wild stuff since I frequent this road almost everyday.

The rest of the time, I had to hope the route to my destination wouldn’t change as there were tons of road closures due to flooding. Just 30 minutes away from me is the city of Abbotsford. You all probably saw this:

It is pretty crazy. Farmland has been submerged under water. News is that food shortages and gas shortages could be a thing in Vancouver, since the highway that connects us to the rest of Canada is damaged. Railroads have been damaged, and apparently our port is closed right now. Nobody knows how long it will take for the railroad to be fixed, but I think the port can re-open fairly quickly. It hasn’t stopped people from stocking up on supplies. No milk, meat and a lot of empty shelves at my local Superstore.

:format(jpeg)/cloudfront-us-east-1.images.arcpublishing.com/tgam/UTIZKH3YEFFMDLEQIXAOP4K4UU.JPG)

I don’t want to be the guy that said “I told you so”, especially when it is something that is impacting many people’s lives… but unfortunately, I think other parts of the world will be seeing similar things. Here again is the inaugural Sector Roundup where I outlined the bullish case for Agriculture, and why I am going all in. Ironically, that article came out when the Lower Mainland was seeing record temperatures of 40 Celsius plus. Take a look at my four bullish reasons.

In other news, farmland has risen 18% this year. The most in nearly a decade, and continuing to surge with no end in sight.

Farmland values jumped 18% from a year ago during the third quarter of 2021 in the Seventh Federal Reserve District, a five-state region including all of Iowa and most of Illinois, Indiana, Michigan and Wisconsin, according to the Chicago Fed.

The gains come as farmers were bolstered by high incomes and low interest rates, and after corn and soybean futures climbed to multiyear peaks in Chicago amid adverse weather for crops.

Now, the high farmland prices are adding to concerns about inflation, with rising costs for raw materials and transportation leading to increases in food prices.

Two points to bring up. First, I mentioned the idea of investing in agricultural land when I highlighted the company Farmland Partners (FPI), who invest in Agricultural land.

Secondly, there was a book by James Rickards titled “Aftermath: Seven Secrets of Wealth Preservation in the Coming Chaos” which came out in 2019. He interviews a member of a wealthy Italian family that has kept their wealth preserved for about 500 years. This is just me, but I would guess it was a De Medici. Anyways, the three assets the elites invest in for maintaining wealth through centuries are Gold, Artwork and Agricultural land. If it was a De Medici, I guess it helps owning banks too. The point is that real wealth has been investing in agriculture for a long time. Before I delved deeper into this space, there was a conference I attended years ago, and the top investment was $100,000 minimum investment in ag land that produced mangoes and various other fruits, as well as lumber. Oh and let’s not forget that Bill Gates became the largest private owner of farmland in the US.

Good farmland is a great asset. I have friends who made millions in crypto and have kicked it to Mexico and parts of South and Central America to buy farmland and grow their own food. Living the life.

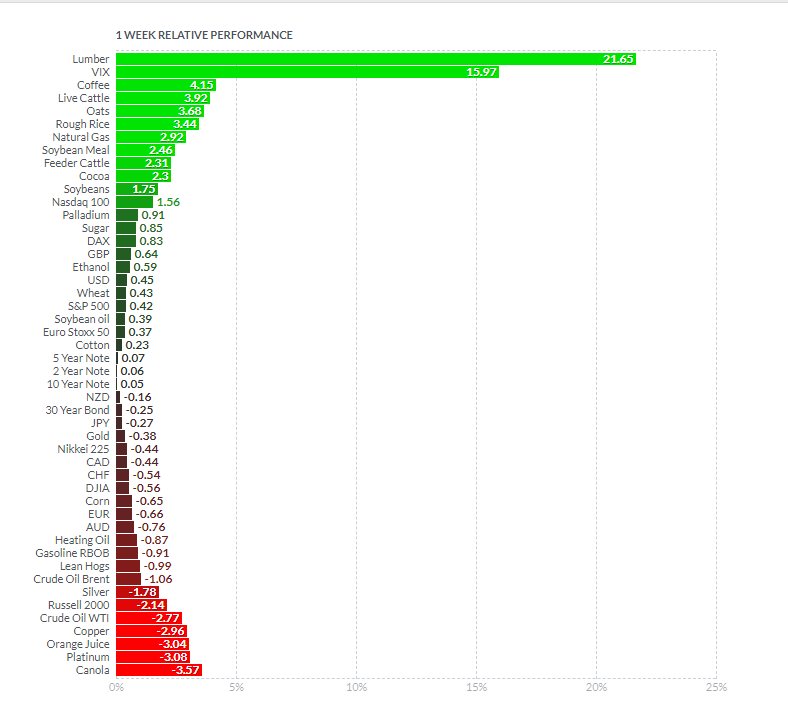

Here are the weekly performances (up to Thursday) for a variety of assets. Look at that. Lumber in number 1 spot. Coffee is up there as well alongside many other ag’s like oats, rice, soybean meal, cocoa etc. Before I forget, I have opened an account with a new brokerage that allows me to trade CFDs on coffee (both Arabica and Robusta), Sugar (both Raw and White), Orange Juice, and Cocoa (Both US and UK), so you will occasionally see analysis on those charts from here on end.

I want to highlight Arabica Coffee. You have all probably heard about rising coffee prices. In fact, I did a caffeinated ag round up just focused on coffee a few weeks ago. Maybe it is time for another in the near future. This week coffee broke out once more. Chance of a pullback before continuing higher, but I am bullish above 2.12 on my CFD chart. The chart and structure looks the same for futures, but the price is obviously different.

Here is Soybeans. We have seen a move in Soybean Meal. Soybean Oil is still basing, but we can confirm a breakout here on Soybeans. I like the double bottom pattern we have, and more importantly, the breakout above a major flip zone (a zone that has been support and resistance in the past). We are now pulling back to retest this breakout zone. Expect to see buyers step in here if a new uptrend is beginning.

Loblaws (L.TO)

With all that’s happening right now, it will be interesting to see if Loblaws can pass $100 per share. As my readers know, this is one of my favorite long term DRIPS play. Just buy a few shares every month. The break above $76 was the big break. The momentum rally afterwards indicated institutional buying. On the road to $100, I have a support way below at $92.00. That is the zone to work with as the stock heads higher.

Loblaws put out earnings and raised their profit outlook on sustained demand for essentials. A stronger case for this here in BC. Here are some earnings highlights:

- Revenue was $16,050 million. This represented an increase of $379 million, or 2.4% when compared to the third quarter of 2020.

- Retail segment sales were $15,831 million. This represented an increase of $367 million, or 2.4% when compared to the third quarter of 2020.

- The two year sales Compound Average Growth Rate (“CAGR”)(5) was 4.5% and 5.5% for Food Retail and Drug Retail, respectively.

- The Company’s e-commerce sales decreased by 0.4% (2020 – 175%) due to the lapping of high e-commerce sales in the third quarter of 2020.

- COVID-19 related costs were approximately $19 million (2020 – approximately $85 million).

- Retail segment adjusted gross profit percentage(2) was 30.7%. This represented an increase of 140 basis points compared to the third quarter of 2020.

- Operating income was $863 million. This represented an increase of $145 million, or 20.2% when compared to the third quarter of 2020.

- Adjusted EBITDA(2) was $1,674 million. This represented an increase of $156 million, or 10.3% when compared to the third quarter of 2020.

- Net earnings available to common shareholders of the Company were $431 million. This represented an increase of $89 million, or 26.0% when compared to the third quarter of 2020. Diluted net earnings per common share were $1.27. This represented an increase of $0.31, or 32.3% when compared to the third quarter of 2020.

- Adjusted net earnings available to common shareholders of the Company(2) were $540 million. This represented an increase of $81 million, or 17.6% when compared to the third quarter of 2020.

- Adjusted diluted net earnings per common share(2) were $1.59. This represented an increase of $0.31, or 24.2% when compared to the third quarter of 2020. The two year adjusted diluted net earnings per common share CAGR(5) was 13.7%.

- The Company repurchased, for cancellation, 3.4 million common shares at a cost of $300 million and 13.6 million common shares at a cost of $1,000 million on a year-to-date basis.

- The Company invested $330 million in capital expenditures and generated $455 million of free cash flow(2).

Slate Grocery REIT (SGR-UN.TO)

Sticking with the grocery theme, I want to bring up Slate Grocery REIT to your attention. This REIT is an owner and operator of US grocery-anchored real estate. Places that will be busy if some of the things I am predicting come true. The REIT owns and operates approximately U.S. $1.3 billion of critical real estate infrastructure across major U.S. metro markets that communities rely upon for their everyday needs.

The stock has been in an uptrend and is beginning to range now. We are ranging between $12.90 and $13.75. I would wait for the breakout, but this is one REIT that you can consider for your long term portfolio. I am not too big on commercial REITs, but grocery stores and senior homes are ones that have a good long term bullish case.

Nutrien LTD (NTR.TO)

Nutrien announced the redemption of $1.8 Billion of debt securities and the commencement of cash tender offer to purchase their debt securities for an aggregate purchase of $300 million. The table for the mentioned debt securities are listed here.

Another agriculture stock that printed new record highs after breaking above $80. Current price is jumping above $86, and it looks like a move higher is in the cards. The large red candle sort of messes up a flag pattern if I were to draw one. Just await a breakout into new record highs.

AG Growth International (AFN.TO)

Sorry, (well not really) but you have to put up with me praising the technical set up of AG Growth for another week.

This is still such a great new uptrend set up. Breakout confirmed above $30, and now it is about making new higher lows going forward. I don’t want to get too technical, but a higher low is confirmed once we break above recent highs. In the case of AG Growth, that would be a break above $34. We then place stops below the swing (in this case $31) and just ride the uptrend.

CubicFarms Systems (CUB.TO)

Buckle up, there is a lot of news to get through. First off Q3 Earnings. Here are highlights:

- Over $53 Million System Sales Pending Installation

- Additional $17.5 Million HydroGreen System Commitments

- The Company currently has a total of 272 modules pending installation. System sales pending manufacturing and installation are valued at approximately $53 million.

- An additional $17.5 million in HydroGreen Certified Dealer commitments for 2022, representing more than 80 HydroGreen Grow System modules.

- Revenue for the three months ended September 30, 2021, was $191,157. Revenue was $4,453,972 in the nine months ended September 30, 2021, and includes HydroGreen equipment, customer seeds and other consumables, as well as CubicFarm Gardens consulting services sold in the period.

- The Company increased its workforce from 71 to 150 full-time employees and contractors as of September 30, 2021.

- Working capital increased from $15,244,610 as of December 31, 2020, to $19,803,440 as of September 30, 2021, an increase of 30%.

- Net loss for the three months ended September 30, 2021, was $7,964,949, a 111% increase from the same period ending September 30, 2020. For the nine months ended September 30, 2021, the net loss was $18,114,078, an 89% increase from the same period of the previous calendar year.

- Research and development (R&D) expenses of $1,825,097 were incurred in the three months ended September 30, 2021, an increase of 71% from the same period of the previous calendar year.

- General administrative expenses increased 104% to $5,051,894 for the three months ended September 30, 2021, reflecting the continued expansion of the Company’s business and necessary staffing additions.

Three HydroGreen Grow System DGS 66 modules have been sold in Utah totaling $450,000.

“We’re thrilled to welcome Rod Magnuson, the owner and operator of Magnuson Cattle Company, with a herd of 800 cows and 1,200 calves, as our newest HydroGreen Farmer Partner,” said Dan Schmidt, President, HydroGreen. “We owe thanks to his neighbor, our Farmer Partner Mike Rigby, for advocating for the HydroGreen technology. Mike continues to host ranchers from all over the state, sharing the benefits he’s experienced with HydroGreen in a short time. Mike is installing an additional HydroGreen system, shifting from saving the farm to expanding his herd.”

Another initial sales commitment from a new certified dealer of $2.7 Million in HydroGreen sales was also announced. Total sales commitments to date from the HydroGreen Certified Dealer Network include over 98 modules in 2022, valued at over CAD$20.2 million.

Finally, a $20 Million Bought Deal Public Offering of Common Shares was announced. 16,000,000 shares at a price of $1.25. The Offering is expected to close on or about November 24, 2021.

A few weeks ago, I spoke about the breakout above $1.50. We had some momentum but price could not push above previous record highs. The run up to earnings saw price give up the $1.50 support zone. We are down 12% at time of writing on a Thursday. The market does not like the fact that shareholder’s are being diluted with this offering. The positive side is the company will have cash to initiate a catalyst. Technically, the $1.15-$1.20 zone is huge support. A major flip zone. Seeing some buyers step in here, and it would make sense to get in below those shares of $1.25. Let’s see if we can bounce from here and plug the gap.

Organto Foods (OGO.V)

Two news releases from Organto Foods, an integrated provider of branded, private label and distributed organic and non-GMO fruit and vegetable products. First an acquisition of Beeorganic, a year-round provider of fresh fairtrade organic bananas based in the Netherlands. The addition of Beeorganic adds significant depth to the Company’s banana category with numerous growth opportunities in one of the largest fruit categories in the world.

Secondly, Organto extended its range of I AM Organic branded products to Gorillas.io, Europe’s fastest growing company in instant on-demand grocery delivery.

Organto Foods broke a major support below $0.40. Now, we have hit the downside support target of the $0.31 zone. A major support here. Heads up: earnings are coming up. I would wait until earnings come and go before initiating a position. A break of this support and it doesn’t look too good.

Verde Agritech (NPK.TO)

Verde agritech explores for and develops mineral properties primarily in Brazil. The company produces and sells K Forte, a multinutrient potassium fertilizer; and Super Greensand, a fertilizer and a soil conditioner. Verde announced a 169% increase in revenues and revised upward targets for the year. Here are some other highlights from Verde’s Q3 2021 highlights:

- Revenue increased by 169%, to $10,651,000 compared to $3,956,000 in the third quarter of 2020 (“Q3 2020“).

- Revenue in Brazilian Real (“R$“) increased by 206%, to R$45,409,000 compared to R$14,815,000 in Q3 2020.

- Gross margin increased to 77% in Q3 2021, compared to 67% in Q3 2020.

- Operating profit before non-cash events increased by 124%, to $3,665,000 compared to $1,635,000 in Q3 2020.

- Trade and other receivables increased by 141%, to $8,238,000 compared to $3,415,000 in Q3 2020.

- Sales by volume increased by 45%, to 153,674 tonnes sold compared to 105,769 tonnes sold in Q3 2020.

- Net profit increased by 192% in Q3 2021, to $3,183,000, compared to $1,090,000 in Q3 2020.

“Our hard work over the years is yielding consistent growth since production started in 2017. In Q3 2021 the effort was relentless as we sought to meet our heightened target, which was achieved thanks to the high quality and commitment of our team. We will endeavour to maintain an exponential growth expansion for the foreseeable future”, said Cristiano Veloso, Verde’s Founder and CEO.

Another stock chart that I have called a new uptrend. Very nice break above $1.10 and the stock has held the uptrend since then. I remain bullish above $1.40. We are now looking for a break above $1.90 and into new record highs after good earnings and revising forward guidance.

Karnalyte Resources (KRN.TO)

Karnalyte Resources explores for and develops agricultural and industrial potash, nitrogen, and magnesium products in Canada. The company owns 100% interests in Subsurface Mineral Leases KLSA 010, KL 247A, and KL 246 totaling 367 km2 of mineral rights. It also holds interests in the Wynyard potash project located in Wynyard, Saskatchewan; and Proteos nitrogen project located in Central Saskatchewan.

A big pop in the stock a few days after earnings. My thinking is the pop is due to the news of increasing prices and shortages of Potash and Nitrogen. Nonetheless, the downtrend has broken, and we are approaching a major resistance zone of $0.30. We break above that and the stock flies. A nice 90% plus move on the stock this week alone.

Deveron Corp (FARM.V)

Deveron remains in our large triangle pattern technically, with the company releasing Q3 Financial results reporting a 127% year over year revenue growth. Here are some more highlights:

- Revenue in Q3 grew 127% year-over-year to $1,607,569. Revenue in the 9 months rose 94% year-over-year to $4,107,373.

- Gross profit in Q3 grew 128% year-over-year to $1,007,514 and YTD grew 63% year-over-year to $2,650,313.

- Better Harvest was acquired by Deveron prior to Q3/2020 and YTD revenue grew 34% from the prior comparable period to $657,004.

- Successfully launched its carbon services platform. Since the end of Q3/2021, Deveron has announced four contracts for this program.

It has been a great year for the company and the management is really delivering on growth. I am looking forward to the bright future of this company.