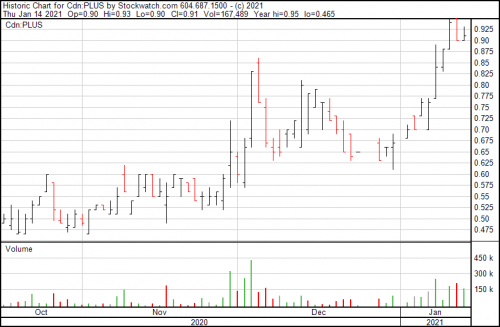

Esteemed California cannabis gummies maker Plus Products (PLUS.C) issued quarterly financials Thursday showing a substantial turnaround as their Nevada and national CBD growth plans take hold.

After a 10c per share loss in Q1, the company presented a mere 1c per share loss in Q2, with $4.3 million in revenue, despite COVID-driven slowdowns in Nevada.

Gross profits climbed to $1.6M in Q2 2020 compared to $0.7M in Q2 2019. Gross profit margin in Q2 2020 was 36%, up from 20% in Q2 2019. Reduced costs per unit derived from operating at increased scale, along with a higher average selling price per unit, drove the improvement in profitability. Operating losses were $(1.4)M in Q2 2020, representing a 71% improvement year-over-year from $(4.6)M in Q2 2019.

Management recently told Equity.Guru their single focus was to bring down costs to ensure a strong base from which to grow, and these figures show that work being properly executed without a notable impact on sales.

I wasn’t entirely convinced they could do it. Here’s what I had to say back in May.

This next quarter will be the one in which Plus has to show its worth.

Regardless of its desire to ramp up sales in new regions, it will need to streamline costs quickly and show the CBD move has legs, if it’s going to justify increases in salaries and marketing.

Note to management: Well played, gentlemen.

You’ve done exactly what you said you would, and during COVID-19 at that.

“The first half of 2020 has been about creating a sustainable economic foundation for the business and continuing to lay the groundwork for current and future growth. We are very happy with the progress we have made on both of these fronts,” stated Jake Heimark, Co-founder and CEO.

“Compared to the second half of 2019, in the first half of this year PLUS grew net revenues 29% from $7.0M to $9.0M, improved gross margin from 19% to 36%, and reduced cash burn 89% from $18.9M to $2.1M.

At the current numbers, PLUS has enough cash in hand to cover a whopping three years of runway.

That’s a full three years before they have to go back to the market for financing, even if sales stay exactly where they are.

I’m going to suggest that PLUS just removed a whole load of risk from their deal. Green light.

— Chris Parry

FULL DISCLOSURE: Plus Products is an Equity.Guru marketing client.