Eskay Creek: 1932-Today

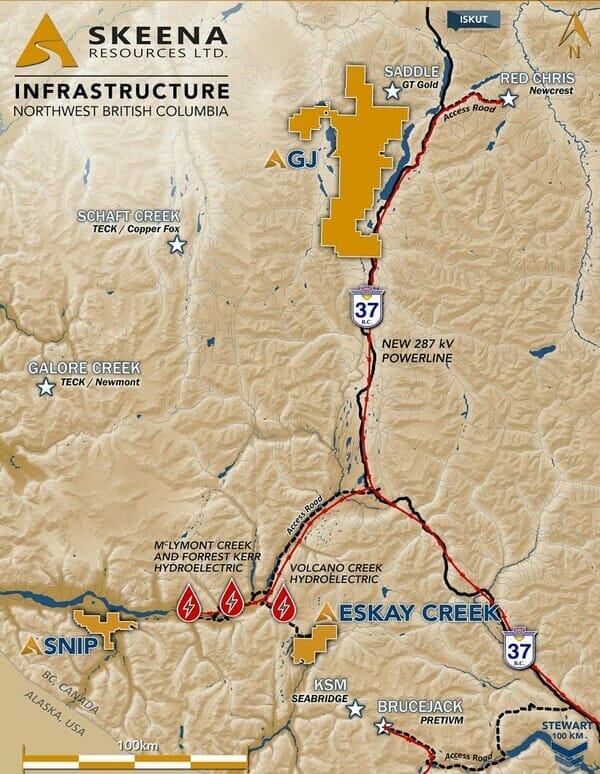

Tucked away in the Unuk and Iskut River region along the rugged north coastal mountains of big, beautiful British Columbia lies a legendary mine called Eskay Creek.

A prospector named Tom Mackay was the first to recognize the area’s unique geological setting after spotting an alluring rock outcrop from his single-engine bush plane. The year was 1932.

A boulder Mackay discovered shortly after staking the property assayed out at a spectacular five ounces of gold per tonne, prompting him to declare, “this will become one of the greatest mines in the province”.

Judging by the boulder’s angular features, Mackay knew it couldn’t have traveled far. But what he didn’t realize is that it had broken free from its source higher up on the mountain, rolling several dozen meters downslope.

Mackay worked the property for over 50 years, but his discovery proved too elusive.

Mackay’s wife, Marguerite, clung to her husband’s legacy, taking control of his company, Consolidated Stikine Resources.

In early 1988, geologists John Toffman and Ron Netolitzsky entered the fray—they liked what they saw at Eskay Creek.

Soon after, Murray Pezim—aka The Pez—was brought in to move the project forward.

It was in the Fall of 1989 when Consolidated Stikine and Pezim’s Calpine Resources hit what John Mackay had been looking for all those years. High-grade gold.

With winter looming, a decision was made to tear up their exploration budget and drill straight on through the Golden Triangle winter.

In the summer of 1990, after drilling 108 holes and with momentum building, they hit a fault. The deposit had disappeared somewhere under the mountain.

Chet Idziszek, Pezim’s onsite geologist, was stumped. After studying his maps and walking the terrain, Idziszek—a rock whisperer if there ever was one—dragged the drill rig to a spot 350 meters from the last hole drilled. That’s where he sunk hole 109.

Hole 109 goes down in history as one of the greats, a genuine monster: 27.2 grams per tonne gold and 30.2 grams per tonne silver over 208 meters.

In 1994, after the dust settled from an intense bidding war, Eskay Creek went into production. The mine produced for the better part of 14 years, finally winding down operations in 2008.

During its peak, Eskay Creek was THE highest-grade gold producer on the planet. It had no equal.

The mine produced 3.3 million ounces of gold at a breathtaking 45 g/t Au, not to mention 160 million ounces of silver at an equally astonishing 2224 g/t Ag.

Enter Skeena Resources (~C$125 million market cap)

One might think that after a run of 14 years, Eskay’s subsurface riches would be completely tapped out. Nope.

In fact, there’s currently more gold in Eskay’s subsurface layers than was ever mined back in the day.

Skeena Resources (SKE.V), with its sights set on creating shareholder value via optioning geologically prospective advanced-stage or past-producing assets, acquired Eskay Creek from Barrick Gold in December of 2017.

The company, run by a young, dynamic, mining savvy crew, immediately went to work on the project, first, poring over 700,000 meters of assay data inherited from Barrick.

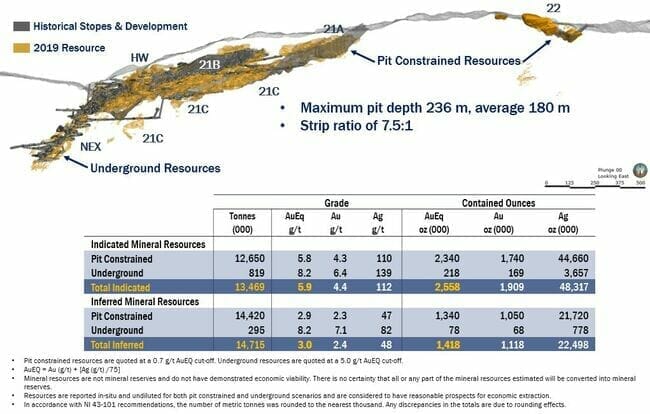

For the first eight months, the company ‘mined’ this assay data. Then, in September 2018 the company tabled their first Eskay Creek underground resource—some 2M ounces at 10 g/t AuEq—based solely on this data inheritance, without drilling a single hole.

Back in the day, due to the remoteness of the project and the low gold price environment (gold traded between $250 and $400), the cutoff grades at Eskay Creek were kept high—15 g/t for the mill feed. Translation: sub-economic ore leftover from the historic operation is hugely economic today—substantially higher precious metals prices and significant advances in infrastructure have made it so.

In February of 2019, after 7k meters of infill drilling and changing their mine plan from an underground to an open-pit scenario, they upgraded the resource.

“Good grades make for good Miner’s”.

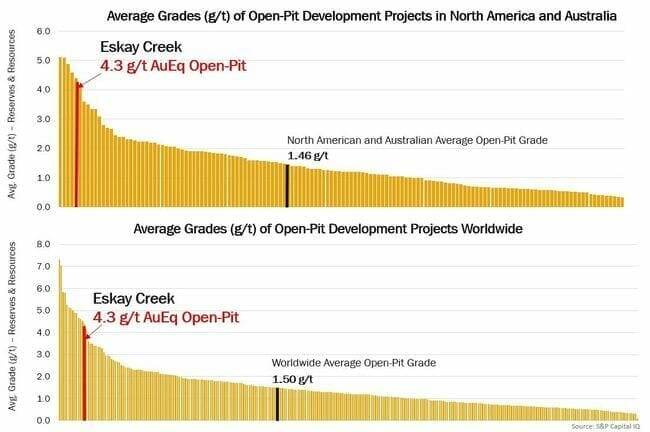

At 4M ounces grading 4.4 g/t AuEq, Eskay Creek now ranks as one of the highest grade open pit deposits on the planet. The maximum pit depth is 236 meters—the average pit depth is 180 meters.

Open-pit mines are typically low-grade scenarios, often less than one gram per tonne (g/t). There are open-pit mines in production today—profitable open-pit mines—producing from sub 0.5 g/t material.

Eskay’s 4.4 g/t AuEq is rich rock.

To say Skeena has been pushing their flagship asset aggressively along the development curve would be an understatement.

The PEA

On November 7, 2019, the company dropped a PEA that turned more than a few heads.

These are robust numbers alright. It’s not often you see an after-tax IRR north of 50%.

Eskay Creek 2019 PEA Highlights:

- High-grade open-pit averaging 3.23 g/t Au, 78 g/t Ag (4.17 g/t AuEq) (diluted);

- After-tax NPV5% of C$638M (US$491M) and 51% IRR at US$1,325/oz Au and US$16/oz Ag;

- After-tax payback period of 1.2 years;

- Pre-production capital expenditures (CAPEX) of C$303M (US$233M);

- After-tax NPV: CAPEX Ratio of 2.1:1;

- Life of Mine (“LOM”) average annual production of 236,000 oz Au, 5,812,000 oz Ag (306,000 oz AuEq);

- LOM all-in sustaining costs (AISC) of C$983/oz (US$757/oz) AuEq recovered;

- LOM cash costs of C$949/oz (US$731/oz) AuEq recovered;

- 6,850 tonne per day (TPD) mill and flotation plant producing saleable concentrate.

When Eskay Creek was in production back in the 1990s, road access was limited and there were no power lines to draw energy from. Power was a major cost driver—50% of the Opex was diesel and propane consumption.

Today, with year-round road access and the Volcano Creek Power Station within hiking distance of the minesite (< 10 kms by road), power consumption will eat only 10 – 15% ($0.064 per kilowatt-hour).

Eskay is shaping up to be a substantial producer—more than 300k ounces per year over a nine-year mine life.

CapEx rings in at a very modest C $303M. This low CapEx is due in part to the company’s decision to produce a concentrate rather than building out all the circuits to create doré on site. This raises the Opex somewhat, but it’s a good trade-off.

The after-tax IRR of 51% means that Eskay will generate after-tax cash flow in the range of $147M per annum. Nice!

The price assumptions applied here were conservative—$1325 gold. If we use a $1500 gold price, which might be more realistic (gold is currently trading at $1570 as I type), the IRR jumps to 63% and the after-tax payback period is measured in months, not years.

Eskay Creek has good leverage to higher metal prices.

These are robust numbers alright.

Infill drilling

It’s possible that infill drilling alone will pull in another 1 million ounces.

How?

The drill holes representing the inferred ounces were spaced 50 to 70 meters apart versus the 10 to 15 meters spacings between the indicated ounces—the further the distance between holes, the lower the grade due to the uncertainty. Tightening up these spacings on the inferred ground (infilling) could bring the grade (currently at 3.0 g/t for the inferred material) more in line with the indicated grades of 5.9 g/t Au.

Being a VMS setting characterized by good continuity, there’s every reason to believe infill drilling will connect the dots and usher in another million ounces.

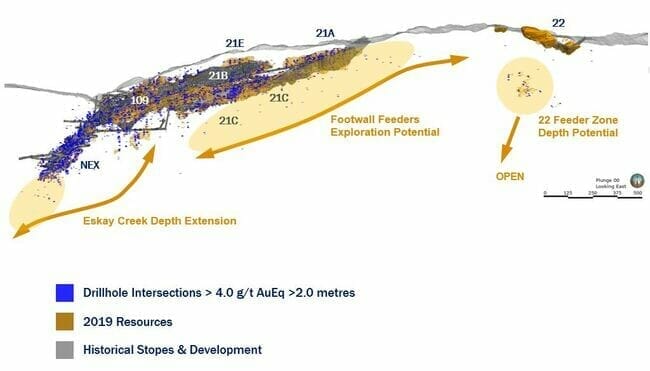

Exploration upside at depth

VMS deposits hold the possibility of high-grade feeder zones (vents on the ancient ocean floor that acted as conduits for hot mineralizing fluids). Tapping a feeder zone and following it to depth opens up significant exploration upside. Note the projected feeder zones on the above map.

Adding validity to the subsurface feeder zone potential at Eskay Creek, the following headline dropped on January 14:

Skeena Intersects 14.73 g/t AuEq over 36.85 m at Eskay Creek

I don’t usually get excited about infill assays, but these are pretty damn good.

Highlights from this phase one program include:

- 10.14 g/t Au, 345 g/t Ag (14.73 g/t AuEq) over 36.85 meters 21A (SK-19-170);

- 2.90 g/t Au, 278 g/t Ag (6.60 g/t AuEq) over 57.90 meters 21A (SK-19-153);

- 4.14 g/t Au, 151 g/t Ag (6.15 g/t AuEq) over 61.50 meters 21A (SK-19-151);

- 7.01 g/t Au, 114 g/t Ag (8.53 g/t AuEq) over 37.89 meters 21A (SK-19-160);

- 4.09 g/t Au, 52 g/t Ag (4.78 g/t AuEq) over 59.00 meters 21A (SK-19-148);

- 6.34 g/t Au, 42 g/t Ag (6.91 g/t AuEq) over 34.00 meters 21A (SK-19-167);

- 8.33 g/t Au, 51 g/t Ag (9.02 g/t AuEq) over 18.45 meters 21A (SK-19-164).

This news release went on to state:

“It is also important to note that this high-grade mineralization occurs not only in the mudstone but also stratigraphically below the mudstone within intensely sheared, brecciated and hydrothermally altered rhyolites. This potentially indicates the uppermost expression of a previously unidentified synvolcanic feeder structure, which could lead to additional exploration targets.”

It’s now time to mobilize a drill rig outside the main resource blocks to test ground that may hold the key to additional ounces AND a longer mine life. Phase I (ground-based) infill and exploration drilling is expected to commence in February.

That’s right! They’re drilling straight on through the Golden Triangle winter.

Do you see what I mean about an aggressive push along the development curve?

Clearly, management has tremendous confidence in this asset.

SNIP

The Snip Gold Project, another legendary past-producing high-grade Golden Triangle mine, was also optioned from Barrick. It was acquired for basically nothing—Skeena agreed to take over the project’s environmental liabilities which equate to roughly $3M.

On September 19, 2018, Skeena granted Hochschild Mining, one of the better underground Miner’s out there, an option to earn a 60% stake in Snip. The option terms are as follows:

- incur expenditures on Snip that are no less than twice the amount of such expenditures incurred by Skeena from March 23, 2016 up until the time of exercise of the Option by Hochschild. (as of June 30 2018, Skeena had incurred C$16.9 million of expenditures at Snip);

- incur no less than C$7.5 million in exploration or development expenditures on Snip in each 12-month period of the Option Period;

- provide 60% of the financial assurance required by governmental authorities for the Snip mining properties.

If Hochschild was interested in Snip early on, they’re likely even more interested now, after Skeena dropped the following assays on January 9:

Skeena Intersects 16.64 g/t Au over 5.10 m in 200 Footwall at Snip

Highlights from this phase 1 round of drilling include:

- 16.64 g/t Au over 5.10 meters including 96.20 g/t Au over 0.50 meters;

- and 39.80 g/t Au over 0.85 meters (S19-035);

- 57.90 g/t Au over 0.65 meters (S19-041);

- 57.00 g/t Au over 0.50 meters (S19-041);

- 12.00 g/t Au over 1.35 meters (S19-043).

The company plans to mobilize a drill rig to Snip next summer to follow up on these results.

BC is open for business

Some critics say it’s nearly impossible to permit and build a mine in the Golden Triangle of B.C.

Not true.

If that were the case, why would the B.C. gov’t pour $2B into infrastructure, into a region with very few human inhabitants?

The $2B was to encourage resource development, particularly mining.

There’s no doubt that mining has an image problem in B.C.

To remedy those concerns and assuage that negative perception, the BC gov’t, First Nations, and industry formed the British Columbia Regional Mining Alliance (BCRMA).

Skeena is a founding member of BCRMA.

Mines do get built.

The Golden Triangle is open for business if you’re willing to work with the Nisga’a and Tahltan, as partners, in a spirit of fairness and cooperation.

More mines will get built. The Majors’ are stepping in. Newmont-Goldcorp recently took a position in GT Gold. Newcrest Mining recently took down a majority stake in Imperial Metals’ Red Chris Mine (a transaction valued at > $800M).

Final thought

There is a very good chance that the brutal bear market in junior mining stocks over the past nine years is at or very near an end. When the trend changes, the turn is often dramatic.

Skeena, with its high-grade open-pit resource of 4M ounces (and growing), could one of the better vehicles to ride this next wave.

We stand to watch.

END

The above article was first published on Tommy Humphreys ceo.ca on Feb. 2, 2020

by Greg Nolan, HighballerStocks.com

Full disclosure: Equity Guru does not have a marketing relationship with Skeena Resources.