In mid-August, I posted an interview of Azarga Metals Corp’s President & CEO.

As a reminder…..

Dorian (“Dusty”) Nicol,

- 40-years international experience in exploration & mining. Dusty has worked in more than 60 countries

- Successful track record of managing exploration and development projects worldwide

- Member of the American Institute of Professional Geologists, a Fellow of the Society of Economic Geologists, a Fellow of the Australasian Institute of Mining & Metallurgy (AusIMM) and a Registered Member of the Society of Mining Engineers

- B.Sc. in geology from Massachusetts Institute of Technology (M.I.T) and a Master’s Degree in geology from Indiana University, fluent in six languages

Azarga Metals [TSX-V: AZR] owns a 60% interest (with an option to move to 100%, upon future negotiated terms) of the Unkur Silver-Copper Project (“Unkur”) in eastern Russia. Unkur is a high-grade deposit that was actively drilled and defined during the Soviet era. It had several mineral resource estimates done, but none were NI 43-101 compliant. The primary goal of Soviet era exploration was to find and delineate copper mineralization. However, once assays were completed, it was noticed that potentially meaningful silver values might also be present. The assayed samples were re-assayed in composites, but key information (about the silver) is incomplete. {See website}

Fast forward to mid-2016, Azarga is drilling close to Soviet era holes to test/confirm grade and thickness of the copper zones, and also to determine if attractive silver values can be identified. The next question, if high-grade silver mineralization is found/confirmed, does it correlate well to the location and grade profile of the copper? These questions are timely as the silver price is up 36% year-to-date!

Assays Report both Higher Grade & Thickness Than Historical Data

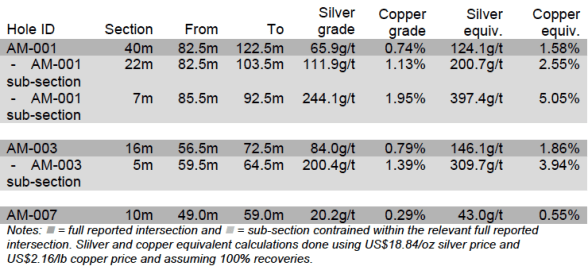

On September 1st, 2 assays were released to the market. One delivered strong results, the other hit lesser grade & thickness, but served to meaningfully expand the area of interest. Drill hole AM-003 returned 16 meters @ 84 grams per Metric tonne (“g/Mt”) Silver (“Ag“), plus 0.79% Copper (“Cu“), from 56.5 meters, including 5 meters at 200 g/Mt Ag, plus 1.39% Cu, from 59.5 meters.

That 16-meter intersection equates to strong equivalent grades of 144.5 g/Mt Ag, or 1.89% Cu. Hole AM-007 is important because it was drilled 750 meters along strike from AM-003, in a location previously not known to be mineralized from historical data. Therefore, AM-007 meaningfully increased the scale of the deposit, and both AM-001 & AM-003 demonstrated higher grades and thicknesses than corresponding Soviet era data. Today’s news validates some of what CEO Dusty Nicol indicated he was interested in finding out in preparation of a maiden NI 43-101 mineral resource estimate.

The chart below shows 3 assays reported since September 1st. AM-001 was reported today, presented with AM-003 & AM-007. Notice that AM-001 hit 40 meters, including 7 meters at 397.4 g/Mt Ag equivalent, vs. AM-003 at 16 meters, including 5 meters of 200.4 g/Mt Ag equivalent. This suggests that grade and thickness (might be) increasing in a northerly direction. Importantly, AM-001’s location extends the strike length a further 300 meters north-northwest of AM-003. Additional assays will be released over the next 3 months. {See Corporate Presentation}

Today, September 19th, the Company released an excellent drill hole assay. Hole AM-001 intersected very significant thickness of {40 meters @ 65.9 g/Mt Ag, plus 0.74% Cu}. On a silver equivalent basis (a metric that converts the $ value of the copper to additional silver grade), that’s 124.1 g/Mt Ag. Individually, the grade and thickness, respectively is good. Combined AM-001 is a great. Also notice the impressive 22 meter subsection in the chart above. {NOTE: grade equivalency for AM-001 based on US$18.84/oz silver & US$2.16 copper}

Putting AM-001 in perspective, if it was a gold assay, it would be about 1.8 g/Mt gold. The best subsection of the 40 meter span is 7 meters at {244 g/Mt Ag, plus 1.95% Cu}, equating to 397 g/Mt Ag equivalent grade. In gold terms, it would be like hitting 7 meters of 5.7 g/Mt Gold on an open-pitiable property. Dusty considers AM-001 one of the best in his 40 year career. {See map below}

It’s important to note that 7 meters is a fairly wide subsection compared to peers that frequently boast their higher-grade material in intervals closer to 0.5 to 2.0 meters. Unkur also has stellar 1-2 meter subsections, but the potential vast scale of the deposit is the key focus. Management believes that a maiden NI 43-101 mineral resource will be completed in 1q 2017.

95% Core Recoveries vs. 40% Historically….

Most important is how new drilling is relating to historical data. Unkur was drilled in the 1960s and 1970s. Since core recoveries were only about 40%, management believes that historical grade and thickness results could be systematically underestimated. There seems to be solid evidence supporting that thesis from these 3 assays. If true, Unkur has the potential (still early days) to be a globally significant silver-copper deposit/resource.

As it stands, 4 additional drill-holes have been completed at Azarga Metals’ Unkur Silver-Copper Project since September 1st, for a total of 8 completed. Assays on 3 can be seen seen on this map.

The Soviet era data included a, “prognostic” resource estimate that, if borne out by new drilling, could point to an area containing hundreds of millions of Silver equivalent ounces. The first step towards this conceptual view will of course be a maiden NI 43-101 compliant mineral resource estimate. Here’s a quote from Dusty Nicol,

“AM-001 exceeded expectations in terms of both thickness and grades. In particular, we are seeing the silver potential being confirmed compared to the historical data that had less information available for silver vis-à-vis copper.”

More specifically, from the press release, (not a direct quote from management),

The results from AM-001 are extremely encouraging. It was drilled to confirm the results of historic hole C-118 which reported an intersection of 23 meters at 0.73% copper with no silver assay recorded. The historic hole had only 40% core recovery and the results from hole AM-001 (which had 95% core recovery) support the contention that historic drilling may have understated thickness and grade of the Unkur mineralization.

To reiterate, 3 reported assays since September 1st show zones of mineralization spread over 1 km of an anticipated 5 to 6 kms of strike length, on the western side of the deposit. With modern drilling and core analysis techniques, the results from Azarga’s 95% core recovered assays lead management to believe that prior explorers responded to the poor core recovery of the day with what appear to be conservative estimates.

Conclusion

Azarga Metals owns a 60% interest in a high-grade, near-surface silver-copper deposit, that contains historic Soviet era drilling data pointing to a substantial ore body as indicated by grade, thickness and strike length. Until a maiden NI 43-101 mineral resource estimate is delivered, expected in 1q 2017, one can only speculate about the deposit’s overall scale and global significance. However, historical data demonstrated a possibility of hundreds of millions of Silver equivalent ounces. Again, this is only a conceptual view, not a forecast or estimate.

++++

At this stage, management’s conceptual goal is to delineate a maiden NI 43-101 compliant mineral resource estimate at a grade and thickness matching or exceeding historical data. In August/September, Azarga has reported solid evidence (not proof) that historical assays may have systematically underestimated both grades and thicknesses. Azarga Metals [TSX-V: AZR] is funded well into 2h 2017, plenty of time to advance the Unkur project towards a Preliminary Economic Assessment (“PEA“) by the end of next year. With a market cap of C$ 13 million = US$ 10 million, the Company’s valuation could have considerable upside if drill results continue to exceed expectations, leading to a favorable maiden mineral resource estimate.

{See Corporate Presentation}

{Today’s Press Release}

{August 15th CEO Interview}

Disclosures: The content of this article is for informational purposes only. Readers fully understand and agree that nothing contained herein, written by Peter Epstein, about Azarga Metals Corp, including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc. is to be considered, in any way whatsoever, implicit or explicit investment advice. Further, nothing contained herein is a recommendation or solicitation to buy, hold or sell any security. The content contained herein is not directed at any individual or group. Peter Epstein and Epstein Research [ER] are not responsible, under any circumstances whatsoever, for investment actions taken by the reader. Peter Epstein and [ER] have never been, and are not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, trader, money manager, compliance or legal officer, and they do not perform market making activities. Peter Epstein and [ER] are not directly employed by any company, group, organization, party or person. The shares of Azarga Metals are highly speculative, not suitable for all investors. Readers understand and agree that investments in small cap stocks can result in a 100% loss of invested funds. It is assumed and agreed upon by readers that they will consult with their own licensed or registered financial advisors before making any investment decisions.

At the time this article was posted, Peter Epstein owned shares and stock options of Azarga Metals and the Company was a sponsor of Epstein Research. Readers understand and agree that they must conduct their own due diligence above and beyond reading this article. While the author believes he’s diligent in screening out companies that, for any reasons whatsoever, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. Mr. Epstein & [ER] are not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts & financial calculations, or for the completeness of this article or future content. Mr. Epstein & [ER] are not expected or required to subsequently follow or cover events & news, or write about any particular company or topic. Mr. Epstein and [ER] are not experts in any company, industry sector or investment topic.