About eighteen months ago, National Access Cannabis (META.V) emerged as part II of the Chuck Rifici master plan of Canadian weed v2.0 domination.

His v1.0 domination plan was a company called Tweed, which later became Canopy Growth Corp (WEED.T). At a current $19.5 billion market cap, I guess you’d call that one a win, but it was very focused on growing weed as opposed to selling it and, towards the end of his time with the company, Rifici was finding himself increasingly at odds with management, and interested on what happens after you’ve grown the weed. So he stepped out to explore other options.

Weed 2.0 was going to require a bit more lateral thinking than simply sticking seeds in pots and turning on the lights. Oils were the focus of most folks looking for what’s next, but where those oils, and flower, and edibles and vapes and whatever else might emerge was going to be sold to consumers was the big opportunity.

The only problem: It was, and for the most part still is, illegal to sell these products in actual stores.

Creating a chain of dispensaries, a national distribution network the likes of which was already being seen in some US states, was going to take some finessing. How might one start a public company aimed at opening a dispensary chain, when dispensaries were forbidden?

You might do deals with First Nations groups, as a starter. You might open ‘education clinics’ as a placeholder. You might speak in code a little so as to not get in trouble as a public company with a plan to do something not legal yet..

While that might seem to be an ordeal, there would be more challenges to consider. Like, in the event you ever did open those dispensaries, how would you secure a good supply of product on the cheap?

Rifici’s plan on that front was a company he would call Cannabis Wheaton (now Auxly (XLY.V)), which would finance grow facilities in return for streaming supply deals that would one day bring in monthly truckloads of licensed Canadian weed, bought more or less for cheap stock.

The next step was to form National Access Cannabis, ostensibly as a medical education clinic chain, trojan horsing itself into the culture while the feds tried to figure out how dispensaries might work, one day, maybe.

I asked Rifici several times over that period if the two companies were part of one plan, and he always hedged his answers in words like, “who knows what the future will bring,” so I took that as a yes and he’s never corrected me yet.

And I could get behind that plan. We needed a healthy dispensary market to keep the healthy LP market fueled, and if you’re into balance sheets, generally speaking the money resulting from selling a consumer value-added product is going to be far more than the money made on the original farmed ingredients.

ENTER THE FEDS

But the Canadian government isn’t filled with smart people playing a long game, it’s rife with reactionary pearl clutchers who have seen Reefer Madness too many times and can’t understand why the kids keeping playing that infernal rock’n’roll music and worshiping Satan and eating Tide Pods.

So when the rules for Canadian cannabis distribution came out, it wasn’t the beginning of a new multi-national industry with Canada forever leading the world. Rather, it was a fucking mess. The feds essentially said, “Gah! Let the provinces figure it out” while the provinces were saying, “Gah! We don’t know what to do!”

Nature abhors a vacuum, so the unionized liquor distributors stepped in and volunteered themselves to run things because, lord knows, if you have trouble recommending a sassy Shiraz you’re going to have no trouble at all recommending a low THC strain that might help with anxiety and backpain, while being legally prevented from telling customers that there are any health benefits to anything you’re selling.

Canadian retail cannabis is still a fucking mess. The reputational damage of legal weed in the minds of the Canadian consumer right now is high, and the opportunity loss, as investor dollars have flowed into US MSO’s instead, is higher.

So, of course NAC’s stock is down. Hell, it’s down hard. It ought to be.

Hey, the US may still consider marijuana to be the devil on a federal level, but if you can even just do well in California as a weed operator, you’re dealing with a potential userbase that surpasses Canada’s population.

Marc Lustig got hip to that as the founder and head honcho at CannaRoyalty (now Origin House (OH.C)), pivoting that group away from a US multi-state expansion focus and turning the entire entity back toward the Golden State, before being acquired for a billion dollars by a US multi-state operator (Cresco Labs (CL.C)) specifically because they wanted a beachhead in California.

While he was getting to that exit, Lustig was also working with Rifici on NAC. He’s now Chairman of the Board. Rifici has moved on, due to conflicts of interest with other companies he’s involved with.

So now it’s Lustig’s deal and, just like he did with Origin House, he’s pivoted some.

And, just as happened early on with Origin House, the market hasn’t figured it out yet.

NATIONAL ACCESS CANNABIS IS LEGIT, YO

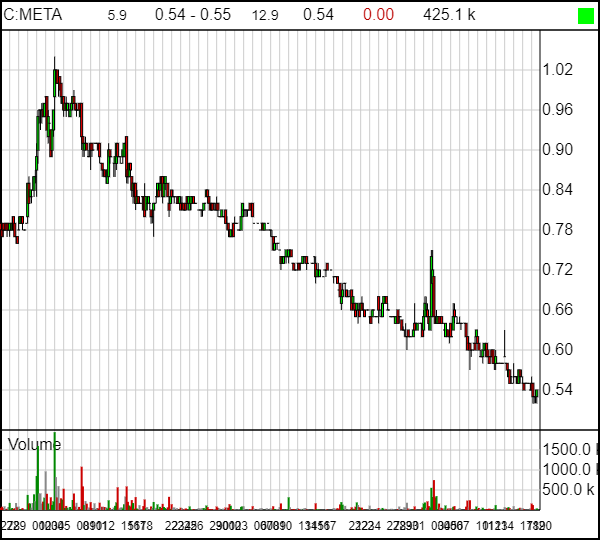

That chart is a horror show, but it matches a ton of Canadian weedco charts over the last few months. As the monster LPs continue to stack mega-losses on growing revenues that can’t possibly justify their market caps, and as Health Canada drags itself along like a redheaded stepchild after a ‘daddy lost his job and has been into the gin’ beating, any smart investor is sitting on an uncomfortable amount of cash.

At times like these, the play is value. Companies like Pure Global (PURE.V) at **$19m** in cap, GTEC Holdings (GTEC.C) at $59m, Biome Grow (BIO.C) at $53m, and C21 Investments (CXXI.C) at $65m are crazy in comparison to their peers, with charts that have seemingly already weathered most of the storm.

META.V, at a $100m cap, isn’t far from those value levels.

BUT WHAT DO THEY HAVE?

Well, this is the surprising thing… they have licensed Canadian retail dispensaries.

Not ‘leases’, not ‘city permits’ without provincial approval, but actual functioning dispensaries.

And not 2 or 4 of them.

They have 29 of them.

To put this in perspective, Trulieve (TRUL.C), as of early April, had 26 dispensaries, mostly in Florida. It has a healthy $460m valuation.

NAC’s ‘META’ subsidiary has 10 locations across Manitoba, Saskatchewan, and the Cree Nation.

Their NewLeaf chain has 13 locations open across Calgary, Lethbridge and Edmonton.

And the parent company has six ‘education centre’ locations, which aren’t dispensaries but do bring in revenue, across five provinces.

How much revenue?

$15.8m last quarter through the retail stores, with another $300k from the education clinics. The previous quarter, revenue was $3.8m from those same stores.

The company ran a loss, but that loss was almost entirely made up of corporate costs which, for a company with over 300 employees, is fair. The retail stores by themselves ran a negligible $8k loss last quarter.

Yes, $8k. Those are new stores doing marketing and taking out leases and being furnished and equipped and hiring, and not only is their rev flying but they’re essentially break even already.

The corporation behind them is not, but the loss on that front is defensible considering the clear growth they’re undertaking.

What makes me very happy with those numbers is the numbers are rising fast, in a market where most have struggled to get a foothold, and you’ve got MARC LUSTIG at the wheel, which has never been a bad thing. That guy knows how to find a good asset, how to pick up said asset for a good deal, with a good structure, and without blowing the bank.

I’m not suggesting you rush out and buy META today. That’s up to you, and your financial advisor, and your god. But the company did just announce a $200 million base shelf prospectus which, if they can fill it, tells me there’s a lot more interest in this company than is currently seen on the daily trading volume.

A base shelf prospectus means they can go raise cash at any time, through loans, financings, warrants, preferred shares… you name it – for however long the prospectus is active.

Why?

“Growing our industry leading footprint from a portfolio of 28 stores to 110 stores by the end of calendar 2020 will require growth capital,” said Mark Goliger, chief executive officer of National Access Cannabis. “The base shelf will provide our company with maximum flexibility to access capital in the future in order to execute on our strategic growth initiatives.”

This means, there will be dilution going forward, which will put pressure on the share price. That, however, is a trade off for the money that will come in, which the company will use to grow as hard as they can.

It’s not a debenture, it’s a warning that you may see one coming, for $2m, $20m, or $200m, as the company sees fit. This is a novel approach, because usually a company will just go grab whatever money they can get a hold of, then spend it, then try for more.

But NAC stock is cheap, so going out for all that finance now would be REALLY dilutionary. Taking what’s needed, as needed, and being able to do so quickly, is smart business. It’s Lustig 101.

Finally: META is not a client. Lustig has always been on good terms with Equity.Guru, but he’s never spent a cent with us. This is just a good company at a good time that, for mine, you’re getting very cheap right now. The last time we said that about one of his deals was CannaRoyalty, at a $200m cap, a year before the $1.1b buyout.

Consider those US comparables on the MSO front, and how inexpensive Canada’s biggest MPO is, and I think that’s something worth exploring.

— Chris Parry

FULL DISCLOSURE: Not a client, don’t own stock but am poised to buy in…