Cannara Biotech (LOVE.C) is a pig.

I mean, okay. Pigs are actually kind of cool, they’re smart and bacon tastes good and they like a tummy rub, so Cannara is not actually a pig. But it is a trap for your money, and you should ideally not play with money traps because their sole purpose is, well, you know.

Why do I say this? Because we are in the worst of all Twilight Zone market dimensions, where straight up financial debauchery is rewarded with short term attention and profit-based absolution, and with each passing cycle the debauchery grows more brazen.

How can this be? How have we moved so far out of the acceptable mainstream where things like the Bridgemark scandal can continue to run, even as they’re being investigated by regulators? Where Aphria (APHA.T), one of the Big Three Canadian LPs, can be shown to be buying assets owned by self-dealing executives on their own team, at inflated prices, and it takes months for said executives to get moved sideways? Where Namaste (N.V) can fire their CEO for self-dealing, and then give him an advisory role the moment he coughs out the words “lawsuit?”

A while back I quoted an interview with financial author Michael Lewis, he of Moneyball, The Big Short, Liars Poker, and Flash Boys fame, where he said, of the global financial meltdown:

“As a rule, it is amazing how even the most corrupt people don’t think of themselves as corrupt. When I write about people who seem obviously villainous, and it’s obvious to a neutral reader that they’re villainous, they themselves don’t agree. It’s not like there’s a bunch of people in each sphere saying, I’m going to make a bunch of money being corrupt. What happens instead is people just follow incentives. There’s a pattern that leads people to either corrupt behaviours, or stupid behaviours. There’s some little carrot out there that they’re following, and they just don’t stop themselves. The run up to the financial crisis, whatever laws were broken – probably not enough laws were broken – it was really the case where a lot of stuff that happened that was awful, was perfectly legal.”

Cannara Biotech is awful. And perfectly legal.

And the people behind it would never consider themselves villains. But they’re engaging in what I’d consider to be a figurative villainy, the sort of loose concept villainy where one just adds an extra 10% to the routine they got away with last time, and another 10% when that doesn’t trip them up, until, eventually, you’re in front of the safe underneath the Bellagio, hanging from fishing wire, dodging laser beams and dobermans, thinking, “Who tripped the alarm?”

Let’s roll back a little to explain.

Back in the middle of 2018, we looked at MedMen’s (MMEN.C) go-public documents and lost our freakin’ minds at the greed afoot.

MedMen (MMEN.C) goes public Tuesday, but three executives will make most of the money on the deal

[…] The CEO and the Chairman will each receive US$1.5 million per year in salary for four years, plus US$10 million in ‘redeemable units’ based on share price, that have vested, plus another $30 million in long term incentive plan units that vest over 24 months, at the end of every month.

This means Bierman is coming into this deal – stock aside – with $1.5 million in salary, another $15 million annually in ‘incentives’, and $10 million ‘just cus’, or $26.5 million off the top.

President Andrew Modlin gets the same deal, so of the $100 million raised in new shares going public, $53 million of it goes straight into the pockets of the big two.

We also revealed how the founding three had dealt themselves Class A shares (which held almost all the voting rights at the company), and a massive golden parachute. This meant they could pretty much never be fired because they’d have to fire themselves to make it happen and, even if that happened, the exit package would pretty much bankrupt the company.

Investors didn’t like this policy, and after we revealed it and a half billion or so dollars of stock value left the room, they changed said policy (and threatened to sue us for the half billion dollar loss). The bonuses would still apply, but now they’d kick in based on share price performance targets instead of time passing, which is still greedy AF, but at least a little more aligned with shareholders.

You know, like how when daddy stops beating you with a shoe, he’s more aligned with you getting to sleep.

Around the same time MedMen was collecting dollars for the Founding Partners’ Hollywood Mansion Fund, FSD Pharma (HUGE.C) came to market from an altogether different crew, but with much the same ‘super voting’ share structure.

So, of course, we wrote about that as well.

It’s happening again: FSD Pharma (HUGE.C) is an insider loaded, overvalued, restrictive mess

FSD Pharma (HUGE.C) has over 1.3 billion Class B Subordinate shares out. I’m sure that seems like a lot of votes, until you understand there are 15,000 Class A voting shares held by insiders, each of which are worth a whopping 276,660 Class B votes, for a total of 4,149,900,000.

Which means the untradeable Class A shares that were divvied up before the company went public will win every vote, for every thing. The CEO could decide he’s going to pivot into human trafficking, and there’s not a damn thing your votes can do about it.

For a while, the stock price on HUGE drifted downward, so the guys behind the company got busy making moves and did the best thing one can do when your deal has been loudly called out publicly.. they called me.

They didn’t hide, they didn’t threaten. They called and talked.

What followed was a long interview in which Anthony Durkacz defended the super voting move, saying it allowed the executive team and board to make fast moves without going to the shareholder base. He even suggested he’d be okay with putting in a sunset clause to hand the voting power back once the company had a chance to make their moves.

That interview was a good one. To his credit, Durkacz stood.

The fact that they’ve raised $53 million and have a grow license is nice, but the Cannabis Wheaton deal ties them in knots forever on cost to produce. Whatever your ‘cost per gram’ is, you’re going to have to double it to factor for what’s going to CBW. THIS IS A BIG DEAL.

So not only are you paying for stock that doesn’t come with votes attached to it, but you’ve also bought yourself, effectively, half an LP.

“You’re not wrong,” [Durkacz] said to me, “Though, also, you’re actually wrong.”

[..]

“If I was looking from the outside, in the past I would have thought the exact same way. Dual structures – that’s crazy, doesn’t make sense. So here’s what I wanted to clarify.

Number one, this dual share structure was inherited. Ultimately when going public those class A shares that contain the vote had to be turned into what they call super voting shares and those super voting shares carry no dollar value. So it’s not like even if you have one class A which turned into something like 230,000 votes. Those 230,000 votes isn’t reflective of a value of 230,000 class B’s. So, in fact, the total dollar value that could be assigned is something minute like fifteen thousand dollars or something like that in total, right.”

[..]

“It means that between myself, the founder and the executive vice president the three of us can make material decisions for the company literally within an hour and I think in this industry because there are going to be a lot of mergers and acquisitions and very material transactions that are going to have to happen just for people to be able to survive in this fast-paced industry. That allows us to move faster than any of them.”

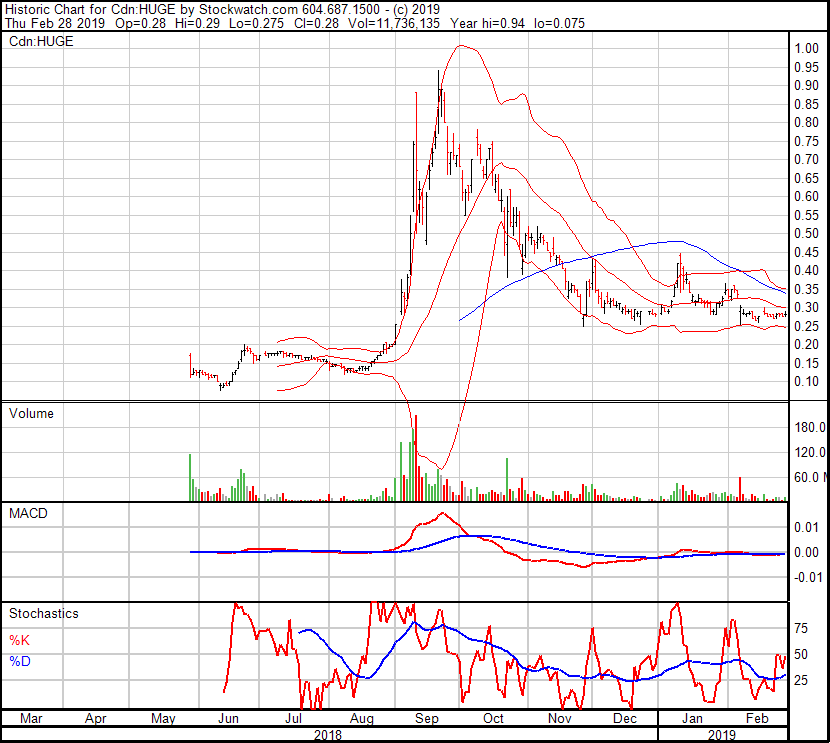

What followed was transformational for HUGE. Without the negative attention on their voting structure, and with confidence the executive and board team behind it had a plan they’d yell about from the rooftops, folks started to buy in.

And those folks spent a good month shooting me neener neeners because I’d dared to question their favourite as it moved up nearly a ten-bagger.

That was a short month. After touching a billion dollars in market cap briefly, it fell hard and has been heavy lifting ever since.

FSD has had some issues recently, not the least of which is the falling out with their one time streaming partner/financier, Auxly (XLY.V).

The joint venture was formed with the intention of developing a portion of FSD Pharma’s cannabis cultivation facility located in Cobourg, Ont., in mutually agreed staged phases. Pursuant to the agreement, the company was to receive a 49.9-per-cent stream of all cannabis produced at the JV facility; the first phase of the JV facility development was to be the construction of an approximately 220,000-square-foot self-contained cultivation facility. To date, the company has invested $7.5-million in the development and construction of the JV facility.

[..] In the course of the company’s efforts to advance the JV facility development, it identified contractual breaches relating to FSD Pharma’s management and staffing obligations of the JV facility, as well as significant concerns regarding certain aspects of the buildings’ infrastructure.

On Jan. 17, 2019, the company provided notice to FSD Pharma of such breaches in the hopes that FSD Pharma would work with the company toward a resolution. To the company’s disappointment, FSD Pharma failed to remedy its breaches and instead purported to terminate the agreement effective Feb. 6, 2019. The company subsequently terminated the agreement effective Feb. 7, 2019.

UPDATE: LOVE execs have contacted me and stated it was they that terminated the agreement with Auxly, not the other way around. That’s factually correct, according to both parties but, as I mentioned above, it’s worth noting that LOVE disengagement happened after Auxly, to repeat, ‘failed to remedy its breaches and instead purported to terminate the agreement.”

Frankly, an inability to get this situation sorted over the last six months without having to go nuclear is NOT a positive for either party, and to suggest an “I’m not fired, I quit!” is some sort of win is utter silliness.

FSD’s facility is a magical swirling vortex where accurate numbers go to die.

Previously, HUGE boasted they were ‘operating out of a 620k sq ft facility.’

Recently, the FSD crew have been reportedly talking about having a ‘combined capacity of 1.2m sq ft’ with Cannara Biotech (LOVE.C), which they’ve just taken public as a side hustle (We’ll get to that one shortly).

Reality bites hard, however. The reason Auxly bailed on their deal was because FSD has only got 25k sq ft currently permitted for growing anything, so they took back their cash and walked – the only deal I’m aware of that Auxly has ever backed out of.

Suitably chastened, FSD news releases now use the following – more accurate – wording to describe their situation:

The Company has 25,000 square feet available for production at its Ontario facility with an additional 220,000 square feet currently in development

What was once touted as destined to be the largest facility in Canada is functionally the size of Anthony Jackson’s West Vancouver ‘Bridgemark proceeds’ shoreline hideaway.

But Cannara isn’t so much an expansion of FSD’s plans as it is a monetization of them… and a repeat of last year’s stock structure bamboozler, with a nasty twist.

The Deep Dive does a really nice job covering this shitshow.

Cannara has a dual class share structure. This consists of both Class A and Class B shares, similar to that of its partner FSD Pharma. However, one key difference, is that Cannara’s Class B shares hold ZERO voting rights.

Currently, there are 15,000 Class A shares in existance, while there are 476,652,330 Class B shares in addition to 207,640,374 subscription receipts for these shares for a total Class B share count of 684,292,704 shares – plus ~31.5 million potential shares in the form of options and warrants.

Care to guess which shares will be publicly traded?

You guys can buy all the Cannara shares you want, and you’ll never be bothered for an AGM proxy because YOU CAN’T VOTE.

Not even a little bit. Not even 10%, so you get the warm feeling that your investment makes you an actual owner, albeit an ignored one.

No, with Cannara, you get to be completely fucking ignored entirely.

UPDATE/CORRECTION: LOVE did indeed alter this two tier share structure upon going public, doing away with it subsequent to the listing.

That’s good. But of the things that piss me off about this deal, it’s ‘early game Jenga’ tuff. What pisses me off royally is what comes below:

Worse: Of the 700m class B shares potentially out there, 300m of them were bought by insiders six months before the company went public at the total cost of…

$300.00

That’s $0.000001 per share.

At today’s share price of $0.215 per share, the founders are sitting on $64m in stock that they purchased for $300 nine months ago.

They’re sitting on a 215,000-bagger.

And the 15k Class A shares that actually have voting rights? They cost the inside guys $15 in total.

Fifteen bucks for complete voting control of the company.

If you look hard enough for a deal, a pink Jack Rabbit waterproof multi-speed vibrator will cost you the voting rights of four Cannara Biotechs.

At least this way, when they screw you, you might get a happy ending out of it.

But hey, great news for those FSD guys. Turning $315 into $64 million is a top result. I’m sure they’ve done a ton of work creating a fantastic business for that sort of profit, right?

Right?

At first glance, it looks amazing!

But when you dig, you find reality to be a harsh mistress.

- Yes, they’ve raised $55m. Congrats on that.

- But they don’t have a 625k sq ft facility, at all, no matter what metrics you use and how you word it. And if they did, it wouldn’t be the largest indoor facility in Canada – at all. What’s up, Aurora.

- And their “>100,000 KG capacity” brag is laughable, especially with no license.

- they may well have 19 provisional patents around CBDs. Maybe. But who cares?

- And the “7 brands, 1 company” is so much hokum. Not one of those brands has sold a product.

Here, give me a minute, I’m about to come up with eight brands on the fly.

- Moose Turds Edibles

- Lucky Darts Pre-Rolls

- RobotCock Vape Pens

- Hamster Panties Hygenic Hair Products

- ThiccBuds Flower Products

- Granny Stoner Seniors Care Products

- SlurredMeow Pet Weed

- KidsBTrippin Gummies

That took me four minutes. Next I’ll head to Fiverr.com and spend $40 getting crappy logos created. Where’s my $50m valuation?

What you’re REALLY buying, when you buy Cannara stock, is this:

The Deep Dive, again:

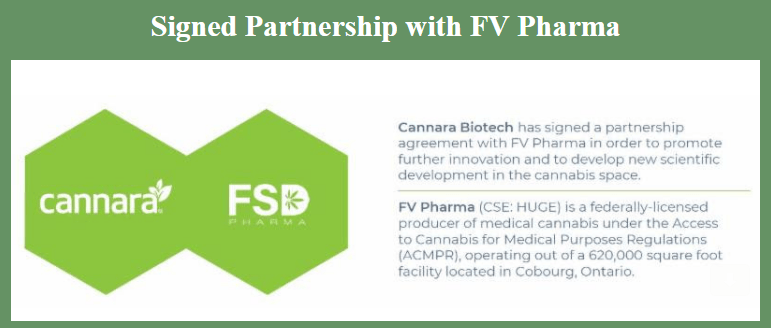

Although the facility is frequently advertised as being 625,000 square feet in size, the context of this is a bit misleading. Although the building may total this square footage, Cannara Biotech’s access to all of that space is restricted – they currently lease out 70% of the building. To be fair a portion of this, 105,523 square feet, is leased to FV Pharma Quebec, a subsidiary of FSD Pharma, and the firms second site. The remaining leased out space is to two non-related entities which use the space for warehousing and distribution. Collectively, leases from the two non-related parties is expected to generate $2mm in revenues for Cannara in 2019.

But hey, at least you’re getting a weed license, right?

Well..

What investors should take note of is that Cannara itself will not be applying for, or at least doesn’t intend to apply for at this point in time, a license to produce cannabis. Instead, FV Pharma Quebec, the FSD Pharma subsidiary, has applied for a second site license to cultivate cannabis. This application was filed on August 18, 2018, and still remains in stage one of six to acquire such a license.

As per the terms of their lease, FV Pharma will be conducting all cannabis cultivation, production, and sales activities at the facility. Meanwhile, Cannara, who has no license to deal with cannabis, will be providing “industry expertise” to FSD Pharma Quebec.

So what does Cannara actually own? Or do?

In their literature, they say an investment is an “opportunity to invest in what is planned to become the largest cannabis indoor grow operation in Quebec.” *

*..that someone else will own the license for.

Cannara wants to create products with the weed grown (by someone else) under a license (owned by someone else) for brands (owned by someone else) they intend to host on site as tenants. Yes folks, you’re buying a piece of a warehouse. THAT’S IT.

Cannara can’t sell weed products, they can’t grow weed, they can’t put their hands on weed, they can’t turn it into lovely juices, they can’t even transport it. They’re simply renting space to people who can and offering ‘strategy.’

In a way, the Cannara plan is absolute genius. If FSD Pharma had simply said, “We’re buying a new building and hoping to put a license in it,” FSD stock wouldn’t budge on the news.

But setting up another company entirely to hold that new building, and taking that company public at a time when weedcos are moving up irrationally, that gets them the $100m bullshit premium that is applied as a base to any cannabis company with a ticker, whether or not there’s a company there.

And by ensuring that 300m shares of the company stock were held by the FSD crew for pennies, before anyone else got a chance to take part, they’ve all instantly got ridiculously rich.

But here’s the kicker:

NONE OF THIS IS ILLEGAL.

All of this jiggeryfuckery, all the weirdness, all the straight up emptiness – they announced it all in their company documents, that you guys never bothered to read.

And you didn’t read them, partly because you’re lazy, but partly because they’re kept on Sedar.com, which is an Alberta Securities Commission-run public document website that appears to have never been updated since the late 90’s, and is so fucking hard to use that it would appear the intention is to PREVENT you from going over public documents, rather than offer a transparent and useful way of checking the validity of your investments before you sink money into them.

And you didn’t read them, partly because you’re lazy, but partly because they’re kept on Sedar.com, which is an Alberta Securities Commission-run public document website that appears to have never been updated since the late 90’s, and is so fucking hard to use that it would appear the intention is to PREVENT you from going over public documents, rather than offer a transparent and useful way of checking the validity of your investments before you sink money into them.

SEDAR is a collection of PDFs, which makes them non-searchable, non-cross referenceable and, since they’re all listed as ‘news release’ rather than with their actual headline, you’ve got to open a dozen documents to find the one you need. WELL DONE, REGULATORS.

I’d love to be sending the RCMP out to knock these guys down for running what is, for all intents and purposes, a shakedown of investors, and I’d love to send the OSC or ASC or BCSC out to shut them down, or even toss a class action lawyer their way to tie them up for a few years… but, and here’s the important thing – nothing they did was criminal.

It’s terrible and gross and obvious, but they will continue to get away with that because you fucking idiots out there, yes you guys reading this, you keep accepting this kind of deal as a rational way of doing business on the public markets.

Aphria scammed shareholders. It blew shareholder funds out buying things the executive team had a personal interest in, for a massive markup over what said executives bought said assets for, and when they couldn’t argue their way out of that story, they simply moved the CEO and carried on.

AND THAT WAS OKAY WITH YOU GUYS!

Nobody storming the AGM. Nobody yelling to the media. No regulator investigation. Hell, half the market was buying the stock in the middle of their scandal because you know nothing will ever really happen to shady players.

So why shouldn’t Anthony Durkacz send out an email to his buddies offering them a means of earning a 215,000-bagger by taking public a thing that could just as easily have been left under the FSD umbrella? Why shouldn’t he put a ticker symbol on a trashbag and toss it out the window at high speed, if you knuckleheads are going to catch it and give all your money to him in thanks?

Cannara is trash. But it’s legal trash.and if you choose to buy into it because you believe that it’s going to benefit from a big pump soon, and you figure you can get out of that situation alive and make some dollars doing so, then FSD isn’t the problem and Cannara isn’t the problem, and the regulators aren’t the problem, and the media isn’t the problem, and the brokers earning their cut out of it all aren’t the problem, and the crappy exchange okaying all three of the poor deals mentioned in this piece isn’t the problem..

YOU ARE, LADS.

Demand more, motherfuckers. This isn’t sports. People’s futures are on the line. It’s called ‘investing’, not roulette.

Hell, at least with roulette you know how much the house will take. Deals like Cannara are less like roulette and more like three card monte.

— Chris Parry

FULL DISCLOSURE: Not short, not long, not interested in any way, shape or form in any company mentioned in this piece.

Excellent, as always Chris.

Some of your finest work. I lost a good chunk of cash on these cunts, recklessly hoping for a repeat of HUGE. Wished on a star and got my butt hurt. I was also too lazy and stupid to even bother researching or using SEDAR. #1 chump.

Thanks, that was ficken awesome.

Keep telling the truth, when enough A holes loss big, maybe something will happen but likely not as long money talks and they are making it by the bag fulls.

I threw a bit of money at HUGE when it was at $0.19/share. I did not think much of the company, but thought that with their grandiose dream of building a 3 million sq ft facility, it would get enough FOMOs’ investing in them. When those investors did materialize and HUGE went over $0.80/share, I bailed immediately and pocketed the nice profit!! I mean, come on, FSD was approaching the same share price as XLY and basically still had (/has) nothing. What a great timed sell for me, as their share price has been in a freefall ever since.

And after conducting DD, I never once had any inkling to invest in MMEN or LOVE. But I do follow them, just to see how long it will take before they implode and leave all their investors broke.

Are you kidding me this is hit piece with lies and inaccuracies. First of Cannara no longer has a 2 tier share structure as they dissolved it before being listed. So you are lying.

FSD terminated it’s contract with Auxly and not vice versa. Auxly had agreed to complete the 220,000 sq ft by Dec, 2018. Then they changed it for 1st quarter of 2019 till finally they extended it to 2nd quarter 2019. Auxly breached their contract because they didn’t execute within the agreed upon timeline. So you are lying.

You have had it in for FSD since inception and write whatever comes to mind without doing your proper due diligence.

You are just as bad as Quintessential Capital Management’s founder Gabriel Grego who spewed half trusts and lies in order to profit from a short selling attack. People like you should be arrested for causing misfortune to all investors. Thank God the SEC and OSC are looking into people like you. Get a life and earn your money honestly not off the backs of hard working investors.

Thanks for the love, and thanks for reading! 🙂

So why don’t you rebuttal my statements? Is it because it will show you for who you are; a person who is looking to bash anything related to FSD?

Why did you copy and paste Auxly’s NR about them terminating their JV with FSD? Why didn’t you use FSD’s NR about them being the one’s that terminated the deal because Auxly was dragging their feet and were 6 months late in the construction of the FSD 220,000 sq ft facility? Is it because if you would have used FSD’s narrative it would be detrimental to the premise of your hit piece?

Why don’t you come out and say that your due diligence is shady at best since you failed to discover that Cannara’s 2 tier share structure was dissolved prior to listing on the CSE? You were to lazy to check so you used the information from Deep Dive’s article which happens to be another shady site used by short sellers to discredit companies to their financial benefit.

The only people who deserve to be stopped are people like you and authors from sites like Seeking Aphria and Deep Dive to mention only a few shoert seller type authors.

If you are going to write article then at least answer the questions!

You raise a fine point about the dissolving of the 2 tier shares. We’ve made a correction to show that.

But you also suggested I spew half truths and lies, which is incorrect and something you should correct.

When you meet me in the middle, we can talk.

I do notice an update/correction section but you do keep the bolder more visible original text which to me defeats the purpose as people are also reading the incorrect information. If someone is just browsing your article then they might only read the incorrect information.

In your second correction you state, “LOVE execs have contacted me and stated it was they that terminated the agreement…” . It should be ‘HUGE’ not ‘LOVE’. I feel the whole paragraph is hard to read so might want to take a second look at it.

You have had to make 2 corrections and therefore your article is full of inconsistencies. So what have I said wrong?

We’re at a point now where your complaints amount to offering us advice on font bolding.

If you don’t like the site, you can go now.

Chris you state and I quote, “UPDATE: LOVE execs have contacted me and stated it was they that terminated the agreement with Auxly…”. LOL it is not the LOVE execs that had an agreement with Auxly it was HUGE. Repeat after me LOVE is Cannara’s stock symbol, HUGE is FSD’s stock symbol.

Have someone proof read your crap before publishing it. If you don’t like the heat than you should stay out of the kitchen.

Cool talk.

This is all bullshit. Get ur facts straight u fuck head .

Julian, your measured and sophisticated analysis is greatly appreciated. All news-desk activities have been halted at Equity Guru – while we collectively extract the intellectual nutrients you have so generously provided. ps. it may feel silly, but it is entirely okay to hug yourself.

Lucas, as the editor don’t you find it disingenuous to write an article with so many mistakes? If Equity Guru wants to be taken seriously then it should strive to do proper due diligence before publishing an article. Did Chris try to reach out to Cannara and FSD to allow them to confirm or deny the contents of the article? Off course not!

Chris did the same thing when he wrote his first article on FSD. He also made mistakes in that article and had not reached out to get their version.

Finally, what is the purpose of updating errors in an article but leaving the original erroneous content intact? Obviously it is clear to see that the article is biased and still intends to be biased.

Hi Ray,

Just off the phone with Durkacz, who has no issues with the stories as they stand, and is discussing working with us to ensure his next deal is better received.

Have a nice day.

Chris, if so, and I will confirm this with FSD, I guess he might have accepted after the 2 corrections you had to make to your incorrect original story. BTW, you should be thanking me for doing your due diligence and helping you fix the erroneous parts of your story.