They’re crappy at blowing their own horn over at International Frontier Resources (IFR.V), so I’m going to do it for them.

Here’s what I wrote back on July 24, in a story that IFR CEO Steve Hanson told me quietly, “Hurt.”

A 50% drop in stock value is a tough day for any resource company executive, but when that executive owns more stock in that company than anyone else, it’s a particularly forceful boot to the nards.

Steve Hanson, President and CEO at International Frontier Resources (IFR.V), had been doing the work, drilling out a Mexican oil concession his company acquired when the Mexican government finally decided to open up its landscape to foreign companies, and [personally] acquiring the largest position of stock in the company. That’s what you want in a CEO – a true believer who puts his money next to yours.

But one of the holes IFR was going after, known as TEC-10, sadly, wasn’t what the company had hoped it would be. Or, at least, the way they came at it wasn’t the right way to come at it. The effect on the stock was dramatic, with 50% coming off the valuation of the company. In the days since, however, a climb back has commenced.

Hanson explained the snafu in great detail – his drill had come into the reservoir more or less right where part of the reservoir had previously caved in, leaving the drill to suck up muck that wasn’t oil, along with some oil, dampening the resulting numbers.

This resulted in TEC-10 encountering non-reservoir shales and mudstones at depths where Tonalli expected the El Abra reef to be structurally high and have good reservoir quality.

Folks sold hard on this news, as one would expect, but when the dust settled it appeared that maybe the sell-off was a little over eager, because IFR still had work to do.

The best possible solution for IFR will be to sling their drills in sideways. Horizontal wells have much more prolific rates then vertical wells, because they have the potential to intersect more porous rock. They’re also great for passing through a vertical rock drop and getting to the oil on either side.

And that’s exactly what IFR said they would do, and have now done.

Sound the fucking bells and let the angels chorus, 3000 barrels of oil have come out of TEC-10 and been trucked off to Mexico’s state oil company, Pemex.

Not a bad turnaround from what once was the cause of a massive sell-off:

On August 6, 2018, Tonalli completed an 18-day flow test of the primary zone interval producing 178 barrels of crude oil during the last 24 hours of the extended well test.

That test went well. Indeed, it went well enough to crank out product.

This is Greg Nolan’s check in on that news:

https://equity.guru/2018/08/08/international-frontier-ifr-v-wait-tick-tec-10-significant-flow/

The big takeaway:

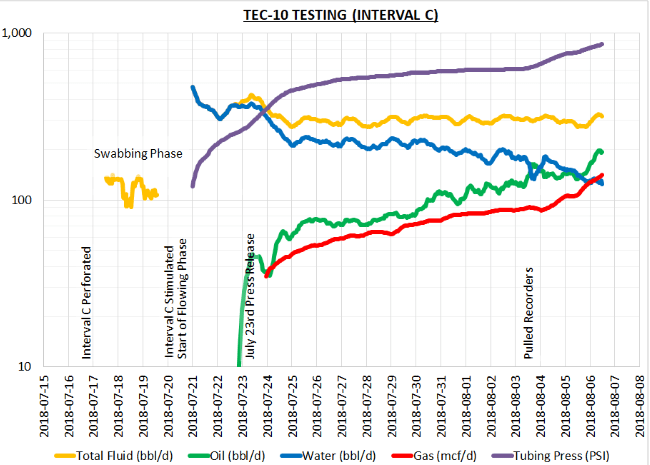

- Daily oil production of the TEC-10 well increased throughout the extended production test from the initial low flow rates observed on July 23, 2018 to more than 175 barrels of oil per day (“bopd”) at the end of the production test on August 6, 2018.

You can see the change in the graph above, showing oil and gas rates constantly climbing and water rates dropping. A nice side perk is the rapidly rising pressure (PSI) rates. That means there’s more inside dying for an exit.

“Achieving crude oil sales and first cash flow is a major milestone in the ongoing development at the Tecolutla field,” said Steve Hanson, President and CEO of IFR. “The efforts of our team and partners have validated IFR’s investment at Tecolutla, and now we look forward to maximizing the returns from Tecolutla and demonstrating our ability to operate successfully in Mexico.”

I called Hanson to see how he’s doing now that he’s off the ledge and looking at promising cashflow. He’s still underplaying it, but it’s okay to do that when the results on the ground are visible.

“We’re going to bring it back on stream,” he told my Friday afternoon.

“From an ops standpoint, the well is back in production and cashflow, With 3000 barrels now being sold to Pemex, and with test flowing at 175 barrels a day, the pressure is really good, so we’re going to open the choke a bit to get more fluids up in the hope that it’ll produce even more, and then we’re going to go ahead of schedule to drill more horizontally.”

IFR perforated a mere 2.4 metre section on the first vertical to get that 175 barrels a day; the most likely plan now is to go with a further 40m section, though Hanson says they can potentially go up to 100 metres, if certain perforations are producing water and just don’t produce enough oil and gas to stick with.

“With the fluid delivery, our science, the workover information, we now know this formation pretty well, we just have to get the oil cut at a productive level, and will build water handling and separation facilities down the road,” says Hanson.

If some investors think 175 barrels a day isn’t interesting, on a drill that’s gone in about the depth of an average basement in a suburban family home, IFR is having none of that malarkey, and here’s why:

- IFR agreed to a significantly lower royalty rate than many of their competitors

- They’re getting a superior price for their oil from Pemex

- They budgeted their costs for this project on oil prices that are at about half the current market average

On royalties:

“Everyone agrees to a base royalty when they come into Mexico, which is a sliding scale everyone has to pay – say 7% or 8% on average,” says Hanson, “and many companies bid additional royalties of as much as 60% to 80%, depending on how badly they wanted to get a license. Landowner royalties, etc add more to that still. We actually lost the first bid on this block. The winner tagged a 68% royalty onto it, but couldn’t meet the necessary terms and conditions, so as the second place bid, it came to use… We got it at 31%.”

On prices they’re getting from Pemex:

“The price we are getting, it’s fluctuating every day, but we’re getting some of the best crude prices in North America for our product,” says Hanson. “It’s probably US$25 higher than what you’d get in Canada, with an asset better than you can find in North America right now. So with a great crude price, and a good royalty rate relative to competitors, that can all lead us to good cashflow,”

On costs:

“When we bid on this, oil was around $40 a barrel,” says Hanson. “We bid on our block to make money at that rate. With an additional royalty at 31%, we thought we could make money there at $40 oil. In this current environment, with oil prices much higher, the numbers start to look really interesting.”0

On the poor early results:

“We still felt we had 138m of reef to work over when we drilled that hole, with oil in multiple zones, so regardless of the market shift in our share price, we were still highly optimistic,” said Hanson. “We felt it should come in at 300-400 bbl/d, so when we stated we hard 3% oil and 97% water, had hit a sinkhole, that was obviously terrible to have to take to market. But we were in the formation and knew oil was in the system, and all logs suggested it was good, so – sure enough – the oil started to slowly increase, pressure went from 200 psi to 900 psi, we 60% oil cut, and 175 bbl/s day. That’s a good oil well, but didn’t meet what our estimates were and what we hoped for.

On Mexico’s new President and what that means for the oil business:

“There’s been a cloud over Mexico somewhat,” says Hanson, “It’s not completely clear as to how the new https://e4njohordzs.exactdn.com/wp-content/uploads/2021/10/tnw8sVO3j-2.pngistration will make changes to energy reform. That said, they can’t change our 35 year deal, and we’re about to earn into that in the next few months. We will meet the minimum requirements doing the work we’re doing right now, but from a macro standpoint, we still have a lot of investors on the sidelines, taking a wait and see attitude.”

“We’re registered in the February auction round, with 37 massive blocks becoming available, though there are questions as to whether that’ll continue, or what form it might take if it does. What we know is, we’ve created 125 jobs, we have strong local content, and Pemex is a partner. “

“Previously, if Pemex wanted to work with a company, they had to get permission from the government and the process was arduous. Now, we work closely with them, and we think there’s some phenomenal joint ventures opportunities with them. In fact, there’s a Pemex JV round coming up in February as well. We’ve studied those fields, we know they’re exceptional assets, and we would love to partner with them. If the government changes make that process easier, we’re all ears.”

IFR’s stock is still at around half of its ‘pre poor drill results’ levels, though it has shown increasing upward movement recently, and one may suspect that, as potential investors become aware of what’s happening on (and in) the ground, this sweet spot may be available for only a short time.

— Chris Parry

FULL DISCLOSURE: IFR is an Equity.Guru marketing client, and the author owns stock in the company.