As one Potash CEO told me in 2008, “As long as people are eating and having sex – potash prices will continue rising”.

That jaunty prediction turned out to be dramatically wrong: since 2008 potash prices have fallen from $800/tonne to $160/tonne. It’s been a long gentle decline. On a chart, the potash price looks like a right-sloping hill reserved for novice snowboarders.

For the uninitiated – “potash” is not something you find next to a burn-hole on your teenager’s pillow. It is a fertilizer mined from deposits left behind when ancient sea beds evaporated.

There is no commercial substitute for potash. An increase in global population combined with a decrease in arable (farmable) land are the two primary demand drivers.

As incomes in India and China grow, consumers shift to a more protein-rich diet, which means they eat more meat. This has an amplifying effect on the demand for fertilizer, because it requires about 5 kilograms of grain to produce 1 kilogram of pork or beef.

In order to satisfy demand for additional grain supplies, further improvements of yields are required from arable lands – driving the demand for fertilizers.

Quite simply, without potash, we will starve.

Before I discuss how to generate wealth from low potash prices – I have a confession: this article is an audition for “Equity Guru” (it is my 1st article).

Am I nervous? A little.

I’ll tell you why.

Over the last decade, I’ve written about 400 articles for 11 different publications. Each publication required “newsy” “authoritative” prose that mimicked the style of The New York Times. Writers were instructed to “foreground the rewards” and “background the risks”.

To be fair I was never asked – or permitted – to lie.

But the concept of journalistic bias was bent like a reed of bamboo to the point of snapping. Sometimes referred to as “stock-promotion-dressed-up-in-a-tuxedo-of-journalism” – this style necessitates a novelistic disclaimer which can be summarized as: “Since I am a prostitute, I reserve the right to fake my orgasms.”

So as I rode the bus to my interview with Chris Parry, CEO of “Equity Guru” – I was anticipating more of the same.

The outside of the Marine Building was the first hint that things might be different.

The building entrance at the foot of Burrard Street features polished brass and an Art Deco flock of Canada geese. Inside the lobby, the elevator panels are inlaid with 12 varieties of local hardwoods. As the elevator doors slid open I half-expected a young Faye Dunaway to hustle past me – sweaty with humiliation.

To my disappointment, Chris Parry was not wearing a fedora – nor did he offer me a single malt scotch.

But the “Equity Guru” business model is different.

Firstly, the client companies are curated. Parry won’t sign deals with companies or people he doesn’t believe in. Secondly – this was more of a jolt – Parry told me that I am welcome to make critical remarks about client companies. Thirdly, he told me that the staff writers at Equity Guru do not need to form a consensus: I am permitted to publically disagree with his opinions – or any of the staff writers.

The thinking is that if you pretend to admire things you don’t admire, your soul will rot. If you serve nothing but praise, that praise becomes devalued. If you can’t disagree with your peers, then a consensus of weak arguments will crowd out a solitary strong one.

So the rules of the game have changed. But do I need to change? Or am I just stripping off clothes that never fit?

Back to potash.

As I mentioned at the top of the article, it’s been a long slow price decline. In the last quarter of 2016, potash prices fell about 33% year-over-year.

If demand is growing, why are the prices declining?

The answer – unsurprisingly – has to do with supply. Potash is an unusual mining commodity in that – when the resource is there – it tends to be there in enormous quantities. It’s not like gold where you chase veins the thickness of dental floss down into the guts of a volcano.

Potash comes in layers 40 feet thick, 1 kilometer wide and 60 kilometers long. There is no shortage of it. The planet doesn’t need more discoveries; it needs more low cost, high value projects.

Potash prices fall because excess supply enables fertilizer buyers to re-negotiate contracts or consume existing inventories

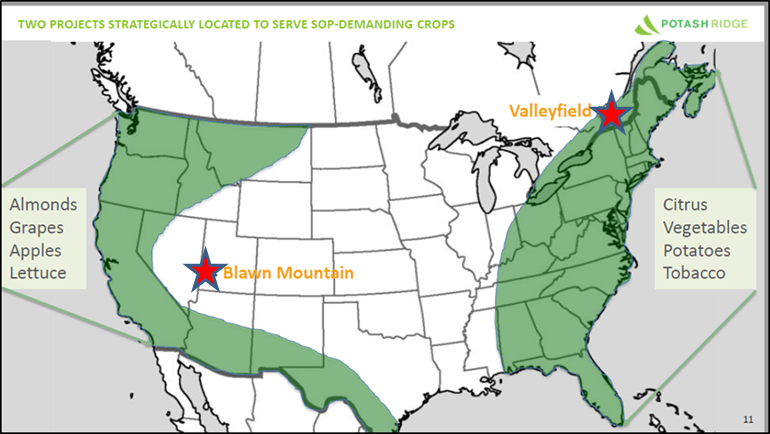

Potash Ridge (PRK.T) owns two “Sulphate of Potash” (SOP) projects, the Valleyfield project in Quebec and the Blawn Mountain in Utah.

Remember “SOP” because it’s an important part of this story, and why Potash Ridge shouldn’t be ignored.

All potash is not created equal. 90% of the global market is dominated by Muriate of Potash (MOP) – also known as Potassium Chloride (KCI). MOP has a global market size of 55 million tonnes/year.

The high chloride content in MOP can damage fruit and vegetables crops, including tomatoes, spinach, carrots, leeks, pineapple, cucumber, tobacco, raspberries, strawberries, avocados etc.

These high-value crops require Potash Ridge’s product: SOP.

Granted, SOP is a smaller market, but it’s also much more lucrative.

If you walked into a butcher shop, MOP would be hamburger meat, SOP would be lamb chops. There’s less of it and it’s much more expensive. You only serve it to people you like.

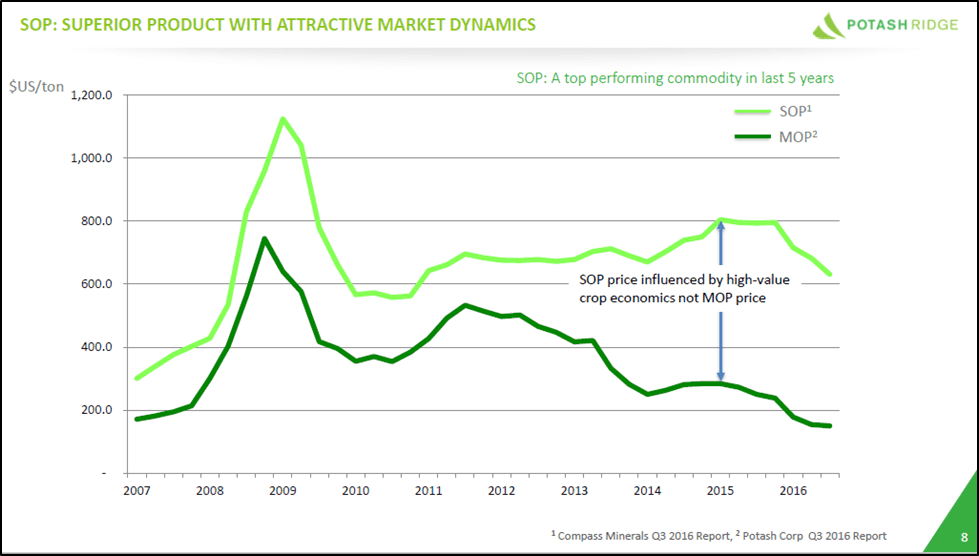

As the following graph shows, there is a significant disconnect between SOP and MOP prices. The price of SOP is anchored to crop value not the MOP price.

“Investor sentiment” is a tricky concept to nail down. But as I see it, Potash Ridge – with a stock price of .23, market cap $29 million – is sitting in a sector shadow (oversupply of MOP) that does not affect its ability to operate a profitable mine.

“Investor sentiment” is a tricky concept to nail down. But as I see it, Potash Ridge – with a stock price of .23, market cap $29 million – is sitting in a sector shadow (oversupply of MOP) that does not affect its ability to operate a profitable mine.

That creates an investment opportunity.

China is the world’s largest producer of tobacco, fruits and vegetables. Not surprisingly, it is also the largest consumer of SOP, accounting for more than 45% of global demand.

Over the past 20 years, the demand for SOP in China has grown about 400%.

In fact, Potash Ridge may not need to export their product to China because the locations of its two projects are strategically located to serve North American markets.

The Valleyfield project will produce SOP through the Mannheim Process; and the Blawn Mountain will employ an alunite material. I could explain the chemistry to you but I don’t like it when people yawn in my face – so I’m not going to.

The President and CEO of PRK is Guy Bentinck who, earlier in his career, oversaw a portfolio of early-stage nickel and cobalt projects ranging between $200 million and $4 billion.

PRK recently signed a 5-year agreement with a major North American supplier for 100% its sulphuric acid requirements for its 40,000 tonne per year Valleyfield Project.

“The next steps to constructing Valleyfield will be permitting, finalizing the $50 million financing requirement, and securing SOP off-take agreements, all of which are expected in 2017,” stated Bentinck.

PRK’s 43-101 Technical Report for the Blawn Mountain Project outlined plans for a surface mine with conventional crushing, roasting and leaching.

The proven and probable mineral reserves of 153 million tons support a 46-year project life. It is expected to be the lowest cost producer of potassium sulphate in North America: average net cash operating costs of $172/ton.

Blawn Mountain is expected to deliver an after tax internal rate of return of 20.1%, based on assumed price of $675/ton for potassium sulphate and $115/ton for sulphuric acid in 2020 and 2% inflation;

After tax cash flow is projected to be $107 million per annum during first 10 years of operation after ramp-up; life of mine average of $128 million per annum.

The downside: potash is not a hot sector.

Investors who purchased shares of the Potash Corporation (POT-NYSE) in 2008 lost 70% of their share value. But in 2016 POT still generated a $1 billion in cash, with a gross margin of about $430 million.

So it’s not like buying shares in a company that makes VHS recorders.

Global potash demand is rising about 2.5% a year. To generate a profit, farmers must have high crop yields. A broke farmer can delay buying potash for a year, but not five years. His land will become fallow.

Investing in a beaten down sector with strong macro-fundamentals is worth considering. To illustrate how strong these fundamentals are, let me give you a personal example: today I woke up and decided, “I am going to eat and have sex”.

Now I seldom achieve all my daily goals. But I always succeed in doing at least one of the things on my list.

I’m just heading out to lunch.

— Lukas Kane

FULL DISCLOSURE: Potash ridge is an Equity.guru marketing client