I spend a good amount of time scouring the Junior ExplorerCo landscape looking for undervalued, undiscovered gems.

They’re never easy to find.

But occasionally you luck out and stumble upon something that makes the whole rummage worthwhile.

When I find a company I like, I try not to get too excited. I try to think like a Brent Cook.

I try to find that fatal flaw, the one that has the potential to derail a project, or kill it outright.

A couple of examples:

- A mineral deposit may look great on the surface, on paper, but in the subsurface layers the mineralization may lack continuity, it might have an extremely high stripping ratio, the ore may be refractory, the deposit may be too deep. Any one of the above conditions can doom a deposit.

- A mineral deposit may appear to have everything in alignment – geometry, good grades, a low stripping ratio, shallow (near surface) mineralization, decent recovery rates – but it resides in a region where armed insurgents or twitchy politicos can to pull the rug out from under it at any time.

There is no shortage of horror stories. Centerra’s ordeal in Kazakhstan and Barrick’s travails in Tanzania come to mind, as do the tragic events surrounding Continental’s Berlin project in Colombia.

If I can’t find that fatal flaw, I begin searching for elements which reinforce my positive take: A management team with skin in the game can be a good one. One or more strategic investors – smart money types – is another. The latter, if the names are noteworthy, can add heaps of validity to one’s hunch.

A new one:

There’s a company we happened upon recently which meets the ‘management-strategic investor’ criteria neatly. It’s an exploration and development company – a new company – with its sights set on Mexican silver.

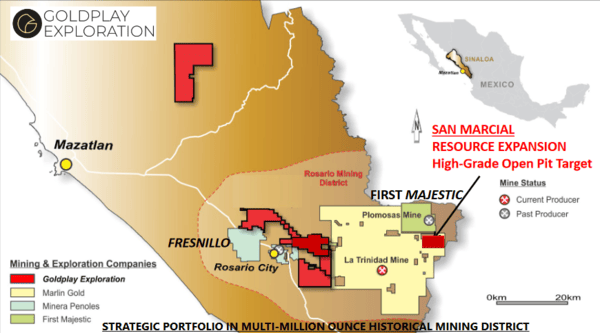

Goldplay Exploration (GPLY.V) holds a strategic portfolio of projects encompassing some 250 square kilometers of concessions in the prolific Rosario Mining District of Sinaloa, Mexico.

This district has a history. Home to a number of world-class precious metals mines and projects, Rosario’s crowning glory is the historic multi-million-ounce Rosario gold-silver mine, an operation which remained in production for over 250 years.

Goldplay’s flagship Rosario asset is San Marcial, a near-surface, high-grade silver-zinc-lead, advanced-stage development project it optioned from SSR Mining (SSRM.TO) last April.

The mineralization at San Marcial is typical of the low sulphidation, epithermal systems hosted near the contact of the Tertiary, Upper and Lower Volcanic units in the Sierra Madre Occidental Geological Province. This Province hosts many important precious metal mines and prospects along its 1,500 km long, 250 km wide extent.

Goldplay’s neighbors include Penoles, Mako (MKO.V), and First Majestic (FR.TO).

San Marcial already boasts 30 million ounces of silver equivalent (AgEq), a resource the company classifies as historical (NI 43-101 – 2008).

Interesting detail: San Marcial’s 30 million oz AgEq resource was based on fifty-two drill holes. It turns out that 22 of these holes were not fully sampled.

The company wasted no time sending the unsampled sections of core off to the lab. Incredibly, some of the core came back with AgEq grades exceeding one kilo per tonne.

Some of the more impressive highlights from this recently sampled historical core include:

- 1.5 meters grading 1,285 g/t AgEq.

- 1.5 meters grading 1,079 g/t AgEq.

- 4.0 meters grading 589 g/t AgEq.

- 1.5 meters grading 1,285 g/t AgEq.

- 6.0 meters grading 1,012 g/t AgEq.

- 12.5 meters (true width 11.2 meters) grading 379 g/t AgEq.

- 14.3 meters (true width 12.9 meters) grading 278 g/t Ag Eq.

- Damn!

It’s not often a company can tack significant high-quality ounces onto an existing resource without mobilizing a drill rig.

This unsampled drill core was a gift.

Without a doubt, Goldplay’s 30 million oz resource is about to grow – the company is due to release an updated, expanded resource estimate. This highly anticipated piece of news could drop any day now.

Another interesting detail: San Marcial’s high-grade AgEq resource is largely open pittable.

The majority of silver mines in Mexico are underground operations. A high-grade open-pit scenario should demonstrate robust economics and a modest Capex. Translation: San Marcial could be a highly profitable mine, and a cheap one to build.

The region’s ample infrastructure should further minimize the capital intensity of the project.

Above and beyond – the resource, the exploration upside:

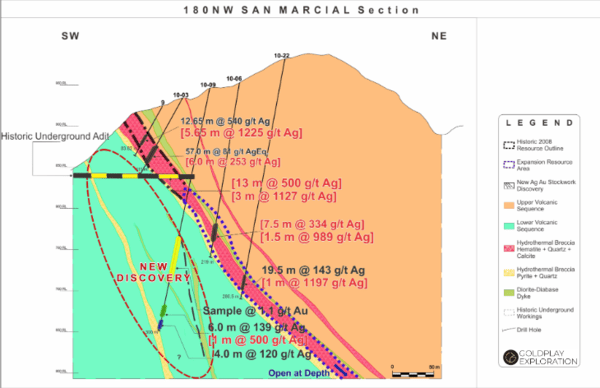

In a Nov. 1, 2018 press release, the company reported it had re-opened an underground tunnel at San Marcial, one that cut the SM Main Fault and associated silver-bearing breccia approximately 80 meters below the surface near the center of the resource area.

Channel sampling within the historical tunnel include an uber high-grade section of 13 meters grading 1,048 g/t AgEq, including 3.0 meters grading 1,934 g/t AgEq.

This could open things up considerably.

These results bolster the continuity of the mineralization and present enticing targets for an upcoming drill campaign.

Once again, San Marcial is destined to grow.

Goldplay CEO, Marcio Fonseca:

“We recently re-opened a historical underground tunnel that cuts through the foot wall sequence of the San Marcial deposit and through the silver-lead-zinc-gold bearing hydrothermal breccia. The high-grade results that we received over substantial widths, including 3 meters at over 1.9 kg/t AgEq, support the high-grade nature of the mineralization. Our understanding of the geological controls on the high-grade mineralization will assist in the planning of our upcoming drill program. The tunnel results support continuity of the polymetallic mineralization from surface and provide positive correlation with our current 3D modeling, which will lead into a new NI 43-101 resource estimate, expected in January 2019.”

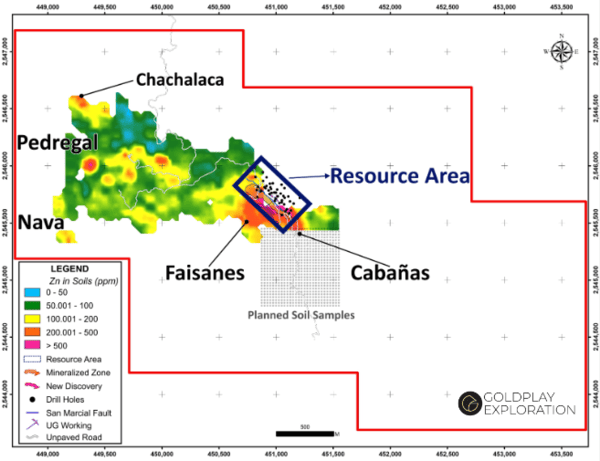

The current resource at San Marcial occupies a mere 500 meters along a 3.5 km mineralized trend.

A total of 14 exploration targets were generated along the property by previous explorers.

The company recently developed five targets that are in close proximity to the resource area.

Good science – mapping, soil and rock sampling, ground geophysics – is being applied to generate these high-quality, high-priority exploration targets.

Fonseca again:

“The San Marcial Project is one of Goldplay’s top prospects in the Rosario Mining District and we continue to be very encouraged by the upside potential for expansion of the deposit. The exploration results on the 3.5 km mineralized trend, in the vicinity of the historic resource, show high quality targets delineated by the soil and rock sampling program. The 250 years of historical silver and gold production in the region, with several multi-million ounce historic silver mines nearby, support the exploration potential for new discoveries on the under-explored San Marcial concession.”

With drill permits in hand, the company is currently interpreting recent exploration results in order to prioritize targets for the upcoming drilling campaign.

The company has also been active on its 100% owned El Habal project where they are exploring an oxidized gold zone along a six-kilometer-long corridor. Recent trenching and drilling at El Habal have produced positive results, but more on El Habal another day.

Final thoughts:

Listening to Fonseca speak, it’s apparent he would entertain a buyout from a resource hungry producer after he bulks up San Marcial, demonstrates the economics and augments its value.

There’s nothing more satisfying than waking up in the morning and discovering your stock halted due to a takeover offer, solicited or not.

Pay particular attention to the 4:00 mark where we get a tour of the man’s resume. Color me impressed.

Note that CEO Fonseca was the VP of corp development for Silver Crest Mines, a company taken over by First Majestic, one of Goldplay’s close neighbors. That transaction was valued at $150M.

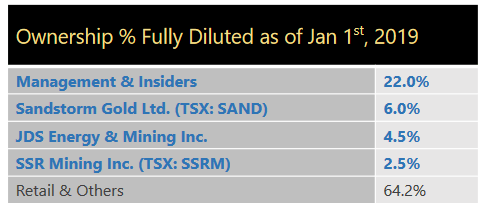

Along with Sandstrom Gold (SSL.TO), SSR Mining (SSRM.TO), and JDS Energy and Mining Inc, Fonseca is one of Goldplay’s largest shareholders. As mentioned above, significant inside ownership and strategic shareholders lend heaps of validity to this play.

With 41.01 million shares outstanding, the company has an oh-so-modest market cap of $9.23M, based on its most recent close at $0.22.

Fonseca’s target for San Marcial’s updated and expanded resource – a number which could drop at any moment – is between 45 and 60 million ounces of silver equivalent.

Considering the high-grade nature of the San Marcial deposit, its open-pit potential and close proximity to infrastructure, it wouldn’t be a leap to expect favorable economics when the company finishes crunching its first set of numbers (a preliminary economic assessment is scheduled for completion in mid-2019).

I like this stock.

END

~ ~ Dirk Diggler

Full disclosure: Equity.Guru does not have a marketing relationship with Goldplay Exploration at this time.