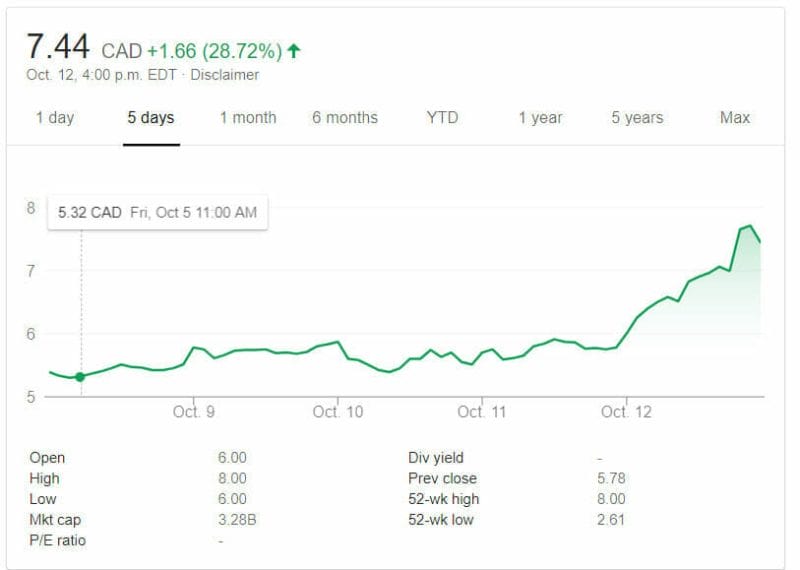

In news that pushed MedMen’s (MMEN.C) share price to new highs, the red shirt crew have announced they’re buying US based Pharmacann LLC for $682 million… or, rather, $682 million of MMEN stock, as of October 9.

Mind you, the news drove the company share price up significantly, meaning the actual price now being paid is $872 million in today’s stock value. Good for the company being acquired, I guess, and good for anyone cashing in today.

MedMen shareholders are beside themselves with the news, as one would be when your stock just jumped 28% in a day, but I’m not a MedMen believer in general terms, a stance taken through several months of watching their self-serving arrival on the market (where three execs got 99.3% of voting power and an absurd bonus/compensation/golden parachute structure), and their ridiculous attempts to shut us up through legal threats.

But the thing I’ve never really been able to get past on MedMen was their valuation, which we’re told by several sources has been a sticking point on several previous attempts to acquire competitors. If you’re going to take stock instead of cash, you need to have a serious belief that stock is worth what it’s being bought/sold for, and going to multiply in value going forward, and not just on the news announcing your deal.

This deal pushes that valuation pretty hard – but, it’s a big enough deal that it may just make MedMen worth something close to its market cap, in the same way Aurora Cannabis (ACB.T), Canopy Growth Corp, and Namaste (N.V) created value by buying things rather than necessarily doing things. Once you get big enough, valuations are tough to tie down and become easier to justify by virtue of your bigness.

MMEN has always been operated like its the biggest weed company in the US, which it hasn’t actually been to date. It wasn’t even the biggest dispensary company in the US, with 14 stores spread over a handful of states, until this deal.

But that hasn’t stopped the execs at red shirt central from pretending they’re giants, reportedly telling some suppliers that if they wouldn’t allow themselves to be acquired for stock, their products wouldn’t be stocked on shelves. An ongoing national marketing campaign, with ads running on Howard Stern’s satellite radio show, would appear to be a pretty dumb way to spend money when 90% of listeners can’t do business with you, but MMEN execs have seemingly always believed its own marketing hype that the company’s eventual gigantic stature was an inevitability.

In the PharmaCann deal, the company receives 10 more dispensaries, and three weed production facilities (one being 125k sq ft and the other two undescribed in promotional material), as well as licenses for future dispensaries.

Is all of that worth $682 million?

While it’s true that no dispensary is making enough money to justify a $50m valuation, which is about where I’d suggest this deal values the PharmaCann stores (I think a $182m valuation on the grow houses and licenses is fair, so $500m is what’s left), what MedMen are really buying here isn’t revenue, or profit, or even profit potential.

What they’re buying here is justification.

You can call yourself the biggest weed company in the US all you want, but until you have a truly national shape to you, you’re nothing. With this deal, yes, MedMen has that national shape. Now, national advertising makes sense. Now, they can actually legitimately threaten suppliers that if they want to bark about being paid on time, the consequences could be harsh.

And, now, the stock value point that kicks in a raft of executive bonuses… looks like actually kicking in.

But is it worth the $3.2 billion market cap currently showing on Google Finance? Is it worth $4 billion of worth it’ll hit once that new stock is added to the share count?

Aphria (APH.T) is a bona fide large weed player in the Canadian space, and it’s market cap is $4.8 billion right now. CannTrust (TRST.T) is another legit player and sits at $1.3 billion. In MedMen worth three TRST’s? The valuations for those companies are hotly debated, despite being a digit away from where the top of the tree sit.

iAnthus (IAN.C), which is directly competing with MedMen in the US dispensary space (and is, in full disclosure, an Equity.Guru client) sits on a $368m market cap for its collection of licenses, weed grow facilities, and dispensaries across the US that, until today’s deal, matched pretty closely in number and reach.

iAnthus just closed a $34.5 million bought deal, which presumably is going to be used toward competing with MMEN on a buying spree. MedMen, at the same time, just closed an $86m financing, and then added a $99.5m loan facility on top of it.

So that’s $185.5 million in debt and share dilution, before you even get to the $682 million in share dilution (or $872 million in today’s value) that the PharmaCann deal brings.

All told, considering the value of the stock right now, that’s over a billion in new money, some of it for stock, some with interest payments due, that MedMen has added to the kitty. It’s also a hell of a lot of stock dilution (PharmaCann shareholders will hold 25% of MMEN stock post-deal)

And for that, ten new stores and three weed grows?

Look, you know what I think of MedMen management – it’s been no secret – but that seems like a risky bet. It’s seems like a double down. It seems like taking out a second mortgage to pay the first.

When comparing MedMen to iAnthus, you’ve got a study in contrasts. One is brash and aggressive, one is softer and steadier. One has come out of the gates with a massive valuation, the other a moderate valuation. One has been up and down since it went public and, for the most part (until today) was a push in terms of value created. The other has been a consistent climber, even in dead markets.

For mine, though, here’s what it comes down to:

MMEN:

IAN:

iAnthus is smaller, but boy has it added value for long holders and made itself an attractive takeover target. Even through sector slumps, it has marched upward consistently and honestly, with good business done in a sector area investors like. But it’s resisted the urge to go borrow half a billion dollars and buy its way to respectability.

https://equity.guru/2018/09/05/canopy-growth-corp-weed-t-5-billion-buy-something-whats-list/

In the words of the CEO a few months back, “You can just go buy whatever you want for whatever money you can raise, but if you can go get a license yourself and open a store for $10m instead of buying one for $100m, that’s the way to go.”

MedMen has been snapping up individual dispensaries whenever it can, of late, with all of those deals being cloaked in secrecy. Frankly, we don’t know if they’re paying $10m per store or $100m, because – and this is fact – the company doesn’t consider its purchase price to be material information.

Here’s the news regarding their Arizona dispensary acquisition:

As consideration for the acquisition, the company will pay approximately 80 per cent in stock and 20 per cent in cash. The stock consideration will be satisfied by way of issuance of shares of Medmen Enterprises.

Here’s the news regarding their San Francisco dispensary acquisition:

As consideration for the acquisition, the company will pay a combination of cash at closing and shares of Medmen Enterprises in an undisclosed amount.

Here’s the news regarding their Chicago dispensary acquisition:

As consideration for the acquisition, the company will pay a combination of cash at closing, deferred cash and shares of Medmen Enterprises, an amount not deemed material.

Excuse me? How is it non-material to tell how much you’re paying for a business that is material enough to announce in a news release? If it’s material to have purchased the business, the price paid is most certainly material.

And this is what I worry about most with MMEN. They set up their ‘supervoter’ share structure, which gives almost all of the voting power to the three biggest execs, presumably for the purpose of being able to act quickly in approving acquisitions. Other companies, such as FSD Pharma (HUGE.C), that have come out with a similar share structure, have given this as their reasoning.

But the problem with that is, you’re trusting that management will behave like adults when it comes to being financially prudent. that they won’t spend an exorbitant amount to increase market cap artificially to trigger bonuses, or that they won’t blow through cash and decide shareholders have no business knowing what they’re spending, or that they won’t jack the share structure to crazily diluted levels, knowing they’ll still control the votes.

MedMen, today, is bigger than it was yesterday, and is certainly more of a player when this deal goes through.

But at what real future cost?

— Chris Parry

FULL DISCLOSURE: The author has beef with MedMen, but no position in the company, positive or negative.

Remember this is the CSE and IRFS accounting and other pronouncements we usually see here in the US are kinda out the door. I am still flummoxed by the allowance of counting plant materials in process (WIP so to speak) as a part of the revenue stream, something GAAP and PCAOB accounting methods and oversight would certainly not allow, I think.