Take a few days for an investor conference, they said. What could possibly happen while you’re not watching the markets, they said.

Okay, let’s slog through it all.

NAMASTE GETS SALES LICENSE, DEMONSTRATING HEALTH CANADA WILL LET ANYONE IN

Just days after Namaste Technologies (N.V) hit the headlines for having a literal bagholder party that featured sexy nurses signing up users for telemedicine weed prescription interviews, earning the ire of Quebec’s overlords and chasing Tilray (TLRY.Q) from a supply deal, Health Canada showed up at Namaste subsidiary Cannmart and gave them a sales license.

Namaste had been through a cheeky week, having news released this…

Cannmart Receives Confirmation from Health Canada That It Will Be Allowed to Purchase Pre-Packaged, Labelled and Tested Cannabis Products

…which was a note sent out to ALL license holders, not just Namaste, but which Namaste continues to press as being some sort of exclusive deal just for them and vindication that they’re for real.

It’s important to remember that, while Namaste now has a license to buy and sell weed online (for medical patients only), it’s also important to understand that they’re not the only ones with an online play.

The monster-sized retail giant Shoppers Drug Mart got a license of their own, and I can guarantee they’ll be making a huge push into the online space, with an existing audience that numbers millions, not thousands, and other LPs are neck deep into ecommerce platforms and plans that are aiming to keep all their margin, rather than surrender it to Namaste.

Vivo (VIVO.V), formerly AbCann, announced just this week they’re in the game, and I keep driving past huge billboards in BC advertising Emerald’s site for ‘information on cannabis’, and hearing Canopy’s podcast ads for the Tweet version of same.

Beacon Medical aims to provide a clear path to understanding medical cannabis,” stated Sung Kang, Vivo Chief Marketing Officer in the press release, “We have upgraded our website to make it easier to navigate and shop.”

The rebuilt website features expanded discount programs, a new classification system called Beacon Cannatypes and “simple categories that help consumers select from the hundreds of strains of cannabis available in Canada”.

Namaste is in the game, but this game is going to be crowded, and while Namaste’s profit margins will be limited to ecommerce, the other guys will be drawing from their growing, extracting, retail and more. If ecommerce becomes a tough place to make money, they’ll be fine… Namaste might not be.

Namaste does understand e-commerce, no question about it, as they’ve run multiple online vape sites for several years, but their success in that area has been largely through online marketing, which isn’t something that Health Canada allows under current rules. Hell, I can’t even get Facebook to accept ads for a story I wrote about e-sports that mentioned cannabis in the headline.

Namaste’s tendency to run at the wall in the assumption they’ll make it through has worked for them so far, with minimal handslaps from those who are tasked with keeping the markets – and the cannabis space – well regulated, so if you’re into keeping score, they’re leading at half time.

But building a company that monetizes the promises made to this point – to be the Amazon of weed – will take a lot more than weekly livestreams to the huddled masses and riding sector jumps.

If Namaste has had success in going all-in on every hand to this point, and it has, it would make a lot of sense for them to now pull back from the table a little, solidify their base, bring some adults into the room, and build a little slower, a little less riskily, and with a view to being one thing really well, rather than everything that’s hot for a minute.

Not that Sean Dollinger and his pinky-sized man-bun are likely to take my advice any time soon, but he’d be wise to. If you keep letting it ride on black all night, the odds you can keep your roll going will slim pretty fast.

TILRAY: THE DRYSHIPS OF CANNABIS

Last year, a little company called Dryships (DRYS.Q) got itself into trouble when it had to sell its cargo ships to cover debts that piled up as the company had bought cargo ships a short while earlier. It got itself out of trouble by issuing stock by the ton to a third party, which was quickly sold off by that party, driving the stock down 97% over a year through several rollbacks that amounted to an accumulative 1 for 7840 reverse split.

DRYS is a mess and will never recover from it’s shenanigans, but that’s not why I’m comparing it to Tilray (TLRY.Q). In actual fact, Tilray is a fine company run by grownups that looks like it’ll be a winner in the long run.

The reason I’m comparing it to DRYS is, nobody who has bought TLRY in the last week did so because they have great long term prospects. They bought it because it was the centre of a gigantic market run and nobody wanted to miss out on a daily 50% jump – even if an investment might come at the risk of a 50% loss the next day.

When Tilray IPOed in July and hit $20, a lot of people with smart outlooks on the cannabis market picked their $1.5 billion market cap as ridiculously high for a company that had was no more advanced than any six others among their competitors.

A few days later, it hit a $300 per share high, good for a $22.8 billion valuation, which it immediately retreated from. Over four days, TLRY lost 75% of its value.

Tilray, to be clear, has never actually looked anything like a $22 billion company. In fact, today’s $7 billion is a stretch if you’re basing it on actual sales, and the likelihood those sales will double or triple in the near future.

The real problem here is, Tilray’s value is irrelevant to North American cannabis investors, who have been playing a Greater Fool game that is beyond dangerous.

If you’re picking Tilray to do anything on a given day, you are playing three card monte, because the ups and downs of that stock are tied to things you don’t know about, and people with far bigger bank balances than you who don’t give a shit about revenue.

The big run, from $20 to $150, was based on a few things; Jim Cramer cupping Tilray’s balls on TV was a help, short seller outfit Citron Research pumping it while beating the tar out of Privateer stablemate Cronos (CRON.T) was another.

But even Citron eventually said TLRY’s value was excessive and said it was looking for a price drop – generally the code that they’re shorting.

From there, someone – and it may have been someone completely disconnected from the company, or it may have been insiders, went on a big short squeeze.

WHAT’S A SHORT SQUEEZE?

First, we need to explain short selling, which is when an investor sells a stock they don’t own yet. How is that possible? They borrow it from a broker, under an agreement that, at some point int he future, they’ll buy the stock back and either pocket the difference in price (if it goes down) or make up the difference in price (if it should instead go up).

So when a group of means decides to short a stock in a big way, they’re creating selling pressure, which drives the stock downward. Eventually, when they have to buy it back, they’re going to create buying pressure and drive it higher.

The bet is, it’ll fall enough in the meantime to make a big profit on the difference.

A short squeeze is when someone with similarly deep pockets decides, screw you guys, I’m buying a boatload of this stock and am going to drive the price higher, forcing the shorters to cover at a loss.

Tilray going from $150 to $300 was a gigantic short squeeze. That’s the good news for the company. The bad news is, this swirling mess was largely happening outside their control, and making their stock too volatile for most investors to play with

If you can read the tea leaves and know a short squeeze is happening, it presents an opportunity to profit from the inevitable sell-off when this carousel stops and the squeezers take their own profits. But because the market was nuts, folks all over Vancouver were talking about their ‘put’ options on Tilray, rather than their shorts.

WHAT’S A PUT OPTION?

If you think a stock will head down in price, a short sell means you’re going to profit from that loss all the way down, but if it goes up instead, especially if it goes up in multiples, you can end up owing a lot more money than you initially planned to wager.

A put is an agreement to sell the stock at a given price in the future, which means if it goes down in price you’re going to benefit from being able to sell it at the higher agreed upon ‘strike’ price, but if it goes up in value you’re going to take a loss.

The difference is, on a put you’re only going to lose, at most, your initial bet. On a short, you can lose multiples of that bet.

If you shorted TLRY at $150, which a lot of folks did, its run to $300 would have had your broker calling you up demanding you settle. Shorting TLRY at $300 would have been a good move, but nobody knew that when it was jumping 50% a day. At that volatility, a short was way risky. So the puts started blasting out, and as the stock plummeted, they made bank.

This is, admittedly, a very simplistic explanation of how this all works, so if you want more detail, here’s where you’ll find it.

Otherwise, back to Tilray.

The higher than expected price of TLRY right now presents an opportunity for early investors to sell out and make nice profit, but a lot of the float is tied up for a bit, which means the thing is trading on high volatility and limited availability. With a small available float, any price move on Tilray can be extraordinarily damaging depending on which direction you’re betting.

So, really, it’s for daytraders with a high risk/high reward profile – only. Until the backroom deals have ended and the casino players have settled their bets, I wouldn’t go near it with a barge pole.

Yes, it’s true that the company is a fine one and will be around for a long time doing real business – but if you’re buying a stock looking for a double, TLRY needs to hit $2 again, and it’s just as likely to end up shredding back to $0.75 the way things are rolling.

We all have FOMO (fear of missing out) sometimes. When TLRY hit $280 last week, I considered, for a hot second, that it might bean interesting gamble to just pile on what looked like a freight train.

I’ve done this before, even on companies I don’t particularly like. Sometimes you just have to let the tide drag you along for a bit and hope you can find some shoreline before you find a waterfall.

But that valuation – I just couldn’t do it. I still can’t. It’s too nutty.

And there are MANY better options in the short term.

ASCENT INDUSTRIES: THE OPTION MOST LIKELY

I ran an event at the Extraordinary Future Cambridge House conference last week called The Gauntlet, and it was one of the most exhilarating things I’ve done in this line of work.

The format was different from the usual ’20 minutes to walk through 36 Powerpoint slides’ that most CEOs get at such events. I wanted it to be brutal, a baptism of fire in which a good CEO with a good company would be left standing at the end while the others writhed in pain.

I asked two rough questions of each CEO, putting them on the spot with no prior notice of what they’d be asked. Then I asked the CEOs to pose tough questions of each other.

To my surprise, they went hard, and it was magnificent.

Patriot One Technologies (PAT.V) was the winner in the end, as several CEOs said, if they had to buy one stock that wasn’t their own, that was what they’d go with. But every other company – Bee Vectoring (BEE.V), SmartShare Solutions (private), DMG Blockchain (DMGI.V), Ascent Industries (ASNT.C) and even Province Brands (private), which I’d previously called a ‘clown car of bullshit claims’ stepped up and defended themselves well.

But Phillip Campbell of Ascent Industries, for mine, was a force to be reckoned with. While non-cannabis company CEOs were put off from picking ASNT as their hot pick because the sector has high valuations that are tough to defend, Campbell’s pitch was a cold blooded assassin in the darkened room. His business plan snuck up on you and just slipped right in between your floating ribs before you knew what hit you.

Ascent has some big plans that will require it to punch above the weight many people associate with it, given the modest size of its existing grow facility, but dig a little deeper and you find a lot going on.

Such as the giant edibles production facility currently being completed in BC, or the massive 600k sq. ft. pepper greenhouse that they’re transitioning to weed a stone’s throw from their existing facility.

Or the lines of CBD products, or the gender identity product for growers, or their dealer’s license, or the forays into other countries, or their deals in Nevada and Washington and Oregon and Denmark..

Here’s their corporate video:

And if you have virtual reality glasses, or even want to just hold your cellphone up to your eyes and scan the room, or (worst case) want to just watch it in full screen, here’s the Equity.Guru VR IR demo we shot for them with our new 360 degree, 3D video camera crew, displayed in glorious 6K video.

Be sure to move it around a little to get the full 360 degree effect.

The real ‘wow’ factor with Ascent broke out while they were at the conference, with news they’ve cracked the water soluble CBD market.

Through Ascent Industries Corp.’s wholly owned subsidiary, Agrima Botanicals Corp., the company has developed a proprietary methodology for producing a variety of discrete, water-soluble cannabinoids, both in powder and liquid form. Cannabinoids in their natural state are oil-based and non-water soluble, making it challenging for beverage makers and edibles manufacturers to evenly suspend and standardize their product mixtures. Water-soluble cannabinoids emulsify evenly, allowing both beverage and edibles makers to completely standardize their product mixtures, giving end consumers a consistent, high-quality product experience. Additionally, water-soluble cannabinoids have a faster activation time of approximately 10 to 15 minutes in the human body, compared with 30 to 45 minutes generally for oil-based delivery methods. These effects generally wear off within two hours compared with four to six hours with traditional oil-based products.

https://equity.guru/2018/09/20/ascent-asnt-c-just-unlock-money-vault/

Worth noting, while others like Sproutly (SPR.C) have bought technology that gets them into this space, and are hence worth a big look, ASNT developed their own tech, and plans to use it to create the water soluble product in their own nearly complete processing facility, for sale to other companies and for their own needs.

When the company’s large-scale production facility, Agrima Labs, is fully licensed and operational, the company expects it will be able to provide large quantities of water-soluble formulate to beverage and edibles manufacturers as an input ingredient. The company expects to provide a variety of discrete cannabinoids, including tetrahydrocannabinol (THC), cannabidiol (CBD), cannabinol (CBN) and cannabigerol (CBG) distillates, isolates and water-soluble formulates, to medical and adult-use product manufacturers globally.

That’s a lot of cannabinoids. If this technology 1) Can be patented and 2) works, ASNT is an absolute steal at its current $202 million market cap. Right now, they’re at the top of my interest list.

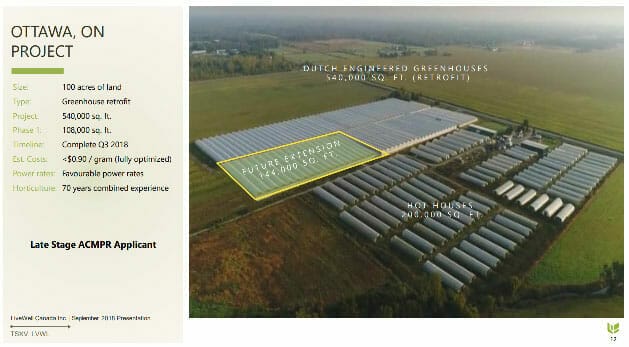

LIVEWELL CANADA: ‘LITTLE CANOPY’ GETS BIGGER

Also interesting, though they’ve been quiet for a bit, is Livewell Canada (LVWL.C), which has existing interest from stakeholder sisters Canopy Growth Corp (WEED.T) and the newly listed venture arm of same, Canopy Rivers (RIV.V).

https://equity.guru/2018/09/05/canopy-growth-corp-weed-t-5-billion-buy-something-whats-list/

Livewell has more than 1.5 million square feet of greenhouses under construction in Ontario and Quebec, and 740k sq. ft. of that in existing greenhouses and hothouses.

That’s a fair whack of land.

The downside on LVWL? They don’t have a license yet.

The upside? Canopy is helping them get that license and, when that happens, the current $155 million market cap will be long gone.

Also, they’re not necessarily tied down to cannabis proper; they’re looking to develop health products based on extracting cannabidiols from industrial hemp, of which they can grow AN ABSURD AMOUNT in those massive greenhouses with necessarily having to spend a king’s ransom on buildout.

You need CBD? Hemp CBD works, but costs a lot less to obtain.

Canopy, for what it’s worth, appears to be looking at LVWL as its hemp products arm, and the deal they made to purchase product, assist with the licensing, and carry all the costs associated with getting that license, puts the company in a really nice position – especially if you think, like you should, that Canopy Rivers isn’t around to toss a few percentage points at upstarts, but rather to get an early bead on takeover targets.

This is not a small deal. Fill that facility with weed and you’ll have a competitive space. Fill it with hemp, and you’ll be providing Canopy all the CBD feedstock they could ever want.

Of course, any LP can grow and squeeze hemp. Why LVWL is more interesting is their partnership with Loyalist college:

Of course, any LP can grow and squeeze hemp. Why LVWL is more interesting is their partnership with Loyalist college:

- Only College in Canada licensed under Health Canada to perform

R&D with cannabis- This partnership enables the isolation of individual cannabinoids

for use in highly precise dosed formulations for medicinal,

nutraceutical, pharmaceutical and future edible products.

That is, they can use trim and waste product of their hemp (and cannabis) to create high value extracts.

- Ability to produce over 100 kg/month of 99%+ pure THC and CBD (>1,000,000 individual 100 mg dosages/m) per production line

- LiveWell has exclusive rights to use the technology in Canada through its licensing partnership with Relief Effects

Not good enough for you? Dig it:

LVWL bought 1000 acres worth of industrial hemp biomass to get the ball rolling, and have an option to grab another 1000 acres more.

That 1000 acres produces around 25k kilograms of CBD isolate, at a cynical price of $6500 per kilo on the market. The math on that is $162 million worth of product, which has to be wrong, and even if it’s not i’m going to discount it because, come on now.

If they get half that, or $81 million, by just processing ornery old, ‘grows on the side of railway tracks, can’t be killed with anything outside of fire and deliberate neglect’ hemp, then anything they can garner from cannabis upon licensing is just cherry.

But this is the one I really like:

Mm-hmm.

This one is also hitting me right in the feels.

Yep. That’s what I like.

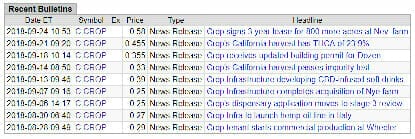

CROP INFRASTRUCTURE: SO MUCH NEWS, WE HAVE SOMEONE ON THEM FULL TIME

‘Dapper’ Dan Terrett, Nick ‘the Hammer’ Horsley, and Hani John ‘Howe Street Napoleon’ al Rayess, from Howe and Bay, are killing me right now.

These fellas, who are steering the marketing efforts at Crop Infrastructure (CROP.C), are giving me the shits to no end. Not because they’re not doing well with CROP (they are), or because they’re not banging out news (lord knows they are), but because they JUST. DON’T. STOP. putting out news.

I mean, Jesus, give it a damn rest you guys. Take a breather. Go to the cabin with your lady. Open a sassy chablis.

The CROP scoreline for the last month is, three PRs in the last week, two the week before, two more the week before that, and two beyond that. Nine pieces of news in a single month, and none of them fluffy.

Look at this:

Nobody who knows this crew would ever accuse them of being late for work. They’re an aggressive marketing group that is looking at CROP as their legacy, and putting all their shoulder into everything it does.

And this is what that looks like:

Big volume, big, consistent moves, manageable selling, nearly a triple in one month.

And so much information going out to the market that it warrants its own news roundup:

https://equity.guru/2018/09/20/crop-crop-c-news-roundup-cannabis-skin-care-harvest-updates-dozen/

That’s right, we’re employing a guy who is pretty much only writing about Crop Infrastructure. He finishes one piece, and before he can post it, there’s more to add. Crop has become a journalism ‘beat’.

That’s insane. But when you start looking through the news in question, it’s legit. There’s a lot to unpack. Go look.

YOU WANT BRANDING? RUBICON ORGANICS (PUBLIC SOON) JUST BROKE THE MOLD

Every LP has its own marketing team, or has paid a marketing agency, to create brands that it hopes will attract your eye at a Canadian liquor store.

Most of them are terrible.

Rubicon Organics is going to, if you’ll excuse the parlance, fuck shit up.

Check it out: The 1964 Artist Series

FOWLER OUT AS SUPREME CEO, BUT NO EXIT ON THE HORIZON

Usually when you hear a CEO has been nudged out, it’s a cause for concern, but at Supreme Cannabis (FIRE.V), there was no way they were going to let esteemed, respected, and occasionally feared executive John ‘T-1000’ Fowler out of the building.

T-1000 has shifted along to the role of President, with a new focus on adult use opportunities, now that the medical/wholesale grow facility he pioneered is nearing completion.

Under Mr. Fowler’s leadership, construction of 7Acres’ world-class facility is scheduled for completion by year-end and annual production capacity is expected to reach 50,000 kilograms in mid-2019. Mr. Fowler’s leadership was also instrumental in Supreme Cannabis securing supply agreements with provincial recreational partners in Ontario, British Columbia, Alberta, Manitoba, Nova Scotia and Prince Edward Island.

The new CEO, Navdeep Dhaliwal, locks in the company’s new focus on driving shareholder returns and talking to the market.

Mr. Dhaliwal, in his role as chief executive officer, will continue to focus on executing on the company’s broader global growth strategy, including merger and acquisition opportunities, strategic investments, and developing the company’s international and medical businesses. Mr. Dhaliwal will also continue to lead the company’s investor and capital markets relations activities. To date, Mr. Dhaliwal has led the company’s capital-raising efforts, strategy, international investments and initiatives.

It’s been abundantly clear, since Supreme begrudgingly decided to start marketing itself to investors this past few months, that investors have appreciated the change. When we announced Supreme had engaged us to help, the stock went on a run immediately.

Now they’ve grown from a $300m valuation to a $582m valuation, that investment in time and focus has clearly paid off. The new leadership team will continue to tell its story, while Fowler (who is great on tape but not one to toot his own horn) keeps the top quality weed rolling out.

I’ve never lost money on Supreme, because ultimately, no matter where the share price rolls, the quality product and people will always win out. From 7c back in the early days, to the $2.19 today, if you trusted Fowler and held tight, you’ve made incredible returns – even as he shied away from publicity.

Now Supreme is prepared to show what it’s capable of, and has declared a stated aim to acquire, grow, and become a truly national brand.

The T-1000 never stays down. It just keeps coming.

— Chris Parry

FULL DISCLOSURE: Supreme, Sproutly, Ascent, Patriot One, Vivo, SmartShare, CROP, and Livewell are Equity.Guru marketing clients, and we may own stock in any of them.

I’m more interested in the pat presentation… what were the tough questions you asked?