With the ASX trading at ten-year highs, it’s time to wind back the clock and take a look at 2008 – a tumultuous year for financial markets across the globe with the collapse of Bear Stearns and Lehman Brothers heralding the arrival of the Global Financial Crisis.

It wasn’t doom and gloom for everyone, though.

One of the great stories of the time is that of Fortescue Metals Group (FMG.ASX), which back in May 2008 achieved a major milestone by shipping its first iron ore from the foundation Cloudbreak mine in the Pilbara region of Western Australia.

In doing so, Fortescue joined an elite club, that of iron ore exporters.

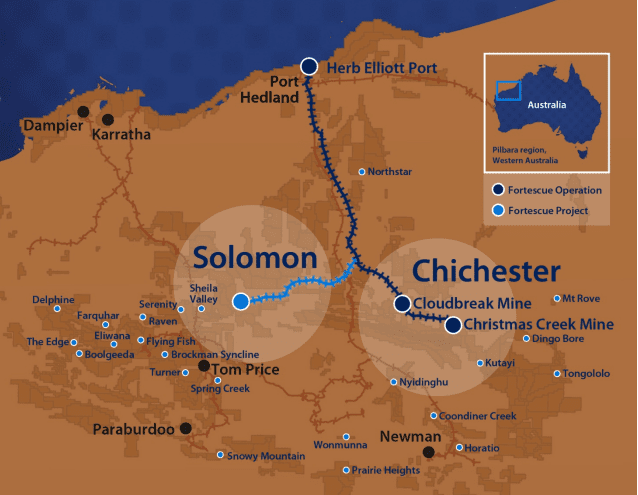

Location of FMG Pilbara mining tenements. Source: ASX Announcements 2

Iron ore is a key ingredient in steel-making and Australia tops the list of world exporters, shipping a staggering US $49.3 billion worth per annum, according to worldstopexports.com

Australia: US$49.3 billion (51.9% of total iron ore exports)

Brazil: $19.2 billion (20.2%)

South Africa: $4.8 billion (5%)

Canada: $3.5 billion (3.7%)

Let’s not forget that FMG was once a penny stock just like many of the mining stocks we talk about here at Equity Guru.

In April 2003 it traded10 at $0.10 and finished last week at $4.39 having undergone a 10-for-1 stock split in 2007.

In pre-split terms, we’re talking about a share price which has gone from 10 cents to over 43 bucks in the space of 15 years. A 400-bagger!

After the fanfare of the first shipment had subsided, the following years would be anything but smooth sailing for Fortescue. Astronomical debt levels and a falling iron ore price represented the ‘perfect storm’ and nearly sunk the dreams of Andrew Forrest for a 2nd time.

Fortescue survived, thanks to securing 4.5 billion in funding which allowed FMG to re-negotiate its debt agreements with the banksters.

The rest is history.

Last month Fortescue celebrated the 10-year anniversary of their first ore shipment with a ceremony taking place at the Cloudbreak mine where Australia’s Foreign Minister Julie Bishop said “Fortescue has changed the face of the Pilbara and the Australian mining industry.”

How they became a 3rd force in Australian iron ore is one of the great corporate stories of our time.

It’s a cracker of a yarn and one which has a personal connection – Besides having traded the stock on numerous occasions in the past, I’m two degrees of separation from someone who made a life-changing score with an investment in FMG. A ‘mate-of-a-mate’ who pinned back his ears and held on to his FMG shares for most of their wild ride, cashing out a good chunk when he spotted CEO Andrew Forrest celebrating his first ore shipment to China (tip: sell the news)

Fortescue and Forrest: One of the great Aussie success stories

To talk about Fortescue (FMG.ASX) is to talk about Andrew “Twiggy” Forrest, an entrepreneur and self-made billionaire who had the vision are wherewithal to bring FMG from concept to reality.

Brian Burke, former premier of Western Australia turned power-lobbyist, said1 of Forrest: “I don’t think anyone else but Twiggy Forrest could have gotten that company off the ground. I’ve met a lot of entrepreneurs, but Forrest was the best I ever saw.”

Forrest, who still holds nearly 30% of FMG’s issued capital, is now an active philanthropist whilst remaining chairman of Fortescue.

With an estimated net worth of more than 3 billion7, he is never far from the apex of Australia’s rich list.

His FMG dividends provide a staggering sum of money when they land in his bank account and according to the ABC, Forrest along with his wife Nicola donated AUD $400 million last year to be used for a number of causes, including cancer research and the eradication of slavery.

Australian Prime Minister, Malcolm Turnbull, described it as “the biggest single philanthropic gift” in Australian history, and the largest donation by a living Australian.

Blue sky mining – The rise of Cloudbreak

In July 2003, Forrest took control of mining-minnow, Allied Mining and Processing, whose name was subsequently changed to Fortescue Metals Group after shareholder approval3.

He then set about drumming-up investor support for his dream of establishing a new iron ore mine in the Pilbara, which would require the construction of a new railway for which at the time he had neither the approval nor funds.

Burning ambition alone would propel Forrest to conquer all ahead of him in his quest to bring his vision to life.

It’s one thing to do it at all (build a mine, that is) – but the speed at which Twiggy put the naysayers in their place is truly mind-boggling.

As Andrew Burrell wrote in the award-winning unauthorized biography Twiggy: The High-Stakes Life of Andrew Forrest: ” In 2003, Fortescue was little more than a thought bubble in Forrest’s hyperactive brain. Within five years, it was the world’s 4th biggest iron ore exporter.”

[Note: Burrell’s account of Forrest and Fortescue is an absolute page-turner, and I highly recommend you get a hold of it. The Kindle version can be had for 3 bucks and I doubt you’ll get much sleep after you delve into the early chapters. (We have no financial arrangements with Burrell or the book)]

The fourth-largest and the three ahead of FMG are heavyweights Vale (VALE.NYSE), Rio Tinto (RIO.ASX) and BHP Billiton (BHP.ASX).

Stop and think about that for a moment. It’s a hell of an achievement.

Why?

Because getting an operational mine up and running is no easy feat and takes money. A lot of it.

The capital expenditure (capex) is enormous.

There are two types of expenses miners face:

1. Capex is ‘capital expenditures’ and refers to the cost of building a project. The lower the capex the better.

2. Opex is ‘operational expenses’ or ‘operational expenditure’.

Think of Opex as ‘everything else you pay for once a mine is built’. Again, you want your Opex to be as low as possible and preferably declining YoY (Year on Year). While not always possible (think fuel costs and currency fluctuations), your Opex directly affects your profitability.

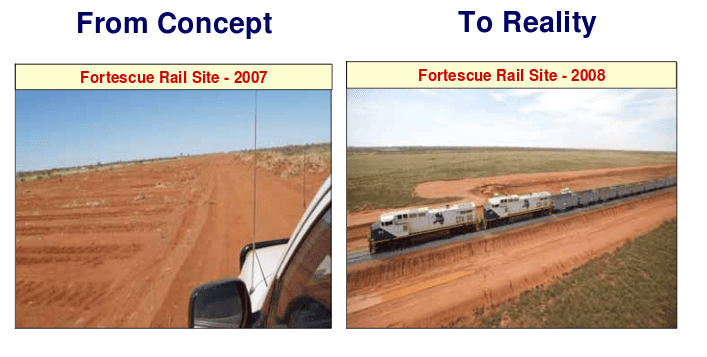

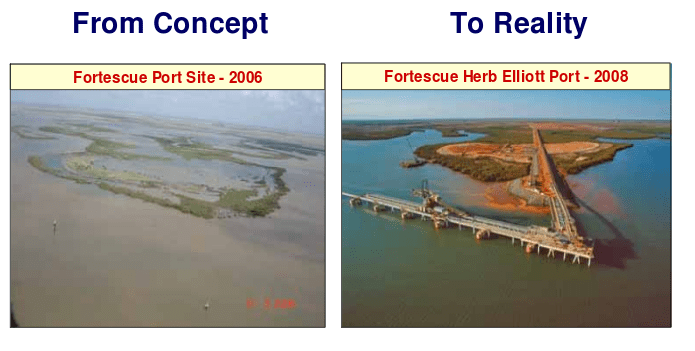

From concept to reality

Take a look at the following pictures and note the time frame.

1. The mine ..

First, you need a mine which is a whole lot more than just a hole in the ground.

You’ll need to order some trucks, crushers, screeners and concentrators.

Source: ASX Announcements 2

You’ll also need a water supply and electricity.

Don’t forget workshops, fuel storage, warehouses, laboratories, https://e4njohordzs.exactdn.com/wp-content/uploads/2021/10/tnw8sVO3j-2.pngistration buildings, access roads and permanent accommodation for your FIFO workers.

Oh, and an airport.

After being one of the first outsiders to undertake a site visit to Cloudbreak, legendary market pundit and broker to the stars, Charlie Aitken, penned a research report4 in 2007 titled “Fortescue: Blue Sky Miner” which made a lot of investors sit up and take notice.

Aitken was convinced the stock was misunderstood by the investment community and severely undervalued.

As he put it “Iron ore is basically a logistics business. It’s all about moving as much high iron content volume as possible, doing it 24/7, and doing it for the lowest possible cash cost. The nature and structure of the ore body make continuous mining necessary. The market has huge doubts about continuous mining of iron ore, yet the technology is widely used around the world in the coal industry. Fortescue has ordered 16 continuous miners from Germany’s Wirtgen, and has people on site at the manufacturing plant making sure the technical specifications are met.”

Surface mining at Cloudbreak. Source: ASX Announcements 2

The above graphic shows surface mining, also known as ‘strip mining’. This is only possible when the ore is at or near surface.

There were doubters as to Fortescue’s use of surface miners even being able to extract the ore, yet Forrest has always been one to challenge the status quo, and more often than not, prove the doubters wrong.

Aitken went on to explain how the topography at Cloudbreak, being somewhat flat, helped to curb FMG’s operating expenses:

The topography at Cloud Break, the key iron ore site for Fortescue, is much flatter than the other existing iron ore mines we saw. This is an interesting point because the topography and positioning of the ore body close to the surface should reduce mining costs and increase sustainable margins.

Some of the other existing iron ore mines we saw are so deep it takes the trucks 40 minutes to reach the top, and one can only guess how many hundreds of litres of diesel fuel that takes. Fortescue’s trucks should only take five minutes across flat country to reach the crushing and screening plants. That is a big sustainable advantage in fuel costs, as is the continuous mining strategy that Fortescue is employing. (Emphasis ours)

Then he threw together a few ‘back on the envelope’ calculations.

Yet, when you do “what if” scenarios you can see the leverage in this stock is potentially enormous. There is no way of buying such pure, large scale, leverage to the sustainability of iron ore contract prices. If I am right about my stated view on the sustainability of iron ore prices, and if I am right about Fortescue’s production growth and selling price assumptions, then in medium-term (three to five years), it could easily be a $100 stock and have a significant weighting in the ASX 200 index. (Emphasis ours)

Within a year Aitken would be proven correct in his assessment of the stocks’ potential, with the price peaking at a pre-split $131.509

2. The railway ..

Then you need a railway line to transport the ore.

Fortescue had no real interest in building one in the first place. The Pilbara incumbents (BHP and RIO), however, had no intention of sharing their rail infrastructure with Fortescue and told FMG politely to fuck off when it tried to negotiate access to the lines.

Source: ASX Announcements 2

The rail line from CloudBreak to the Herb Elliott Port is roughly 290-km long and has 8 major bridges

and 360 culvert installations. The journey to get the ore from mine to port takes 5 hours.

3. The port ..

Lastly, you need a port which can accommodate a Capesize bulk carrier to load your ore into.

What is Capesize you ask?

They’re the ones which are too big to fit through the Panama and Suez canals.

And to get the ore into the ship you’ll need a train unloader, wharf structures and a shiploader.

Capex and more capex.

Source: ASX Announcements 2

When all the above is in place you can finally start shipping the ore and asking the Chinese to make payment.

Source: ASX Announcements 2

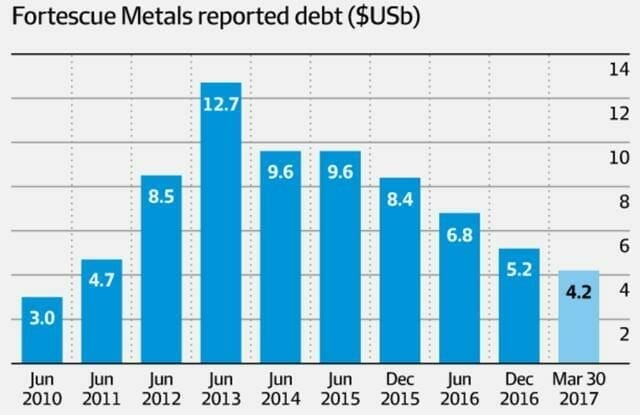

By 2012, FMG was caught in ‘The perfect storm’

Fortescue was playing a dangerous game of ‘cat and mouse’, relying on ore revenues to service its ever-growing debt pile which grew from USD 3 billion to over USD 12 billion in the space of just three years (June 2010 to June 2013).

While the iron ore price remained in the stratosphere, everything was peachy. Then it started to fall, taking the FMG share price along for the ride.

In June of 2012, when FMG was carrying USD 6 billion of debt, the alarm was sounded by Bronte Capital, with John Hempton stating:

Exploration, evaluation and development assets of USD5 billion (give or take a little) and debt of USD6 billion.

And it can all be paid if the iron ore price remains high.

But if the commodity cycle goes back to the dark days when BHP’s margin was around 10 percent this one is pushing up daisies. They have 20 percentage points less margin than BHP and with a commodity crunch their margin will go negative and the debt will not be able to be serviced. (Emphasis ours)

While Forrest had summoned Nostradamus-like powers to successfully predict the Chinese awakening and subsequent mining boom resulting from their near insatiable need for iron ore beginning in early 2003, it’s doubtful he could foresee the alarming drop in the commodities’ price which began in late 2011/early 2012.

Yet others could, notably hedge-fund honcho Jim Chanos, who started to smell blood in the water.

More from Burrell (note: we have added the graphics to provide some context)

By 2012, economic growth in China was beginning to slow down and iron ore prices were retreating from their unsustainable peaks of the previous year. A well-known American hedge fund manager and short-seller, Jim Chanos, began telling his clients that he was “shorting” Fortescue shares, or betting that the price of the stock would fall, because the miner was too highly geared, too exposed to China and was being led by a “promotional management team”. Although Forrest had handed over management to Power by then, the barb about self-promotion was aimed directly at him.

Chanos also predicted that Fortescue would have trouble servicing its huge debt pile if iron ore prices fell below $US100 a tonne. At the time, such a prospect appeared unlikely because iron ore was trading steadily at around $US150 a tonne, allowing Fortescue to meet its interest payments and still deliver a healthy return for shareholders. Moreover, Fortescue’s share price had risen 30 per cent between January and April, despite concerns about the strength of China’s economy. Both Forrest and Power went in hard against Chanos, suggesting Fortescue would always be protected by a natural “floor” in the iron ore price of $US120 a tonne.

Within a few months, however, almost everything Chanos had warned about Fortescue appeared to be coming true. China’s economic growth rate began to slow further and the iron ore price spiralled below the so-called floor of $US120 a tonne. For Fortescue, it was the worst possible timing: the miner’s revenues collapsed at the same time as its debt load peaked.

Unlike its peers BHP and RIO, FMG was highly leveraged and could not weather sustained lower prices to the same extent as the others, especially given its higher production costs.

By September 2012, there was a feeling in the market that Forrest may have pushed his luck too far and FMG would soon be in default of certain banking covenants.

A palpable stench had engulfed Fortescue. Buying FMG shares suddenly seemed akin to a binary options bet where the only likely outcomes were to double your money in short order or lose the lot.

Fortescue, it seemed, might go under.

Then, on September 18, 2012, the company announced it had obtained a USD 4.5 billion secured credit facility underwritten by Credit Suisse and JP Morgan which would give it the much-needed breathing space to restructure its debt.

Forrest had once again cheated corporate death to the chagrin of his detractors.

An 8-year legal battle to clear his name completes an annus horribilus for Forrest

Twiggy’s journey to the top is one of perseverance and personal cost.

With his chequered history in Anaconda Nickel, which nearly collapsed during his tenure, the financial regulators had him truly in their sights from the beginning at Fortescue.

In 2004, Fortescue came under the corporate watchdog’s spotlight when FMG made a number of market announcements with respect to contracts covering the construction of the infrastructure required for the new mine.

It all came down to the interpretation of the words “binding contracts”.

Burrell recounts the story as such:

The trouble had begun in August 2004, when Fortescue had told the market it had entered into a “binding contract” with the state-owned China Railway Engineering Corporation (CREC) to finance and build its railway line in the Pilbara. At a press conference, a journalist had asked Forrest: “You talk about a $1.85 billion project, how much of that is the railway line?” Forrest had replied: “The price of the railway line and the rolling stock is confidential but we are pleased to say it’s competitive.”

Ten weeks later, Forrest had even more good news to trumpet: Fortescue had signed “binding contracts” with two other Chinese state-owned entities, China Harbour Engineering Company (CHEC) and China Metallurgical Construction Corporation (MCC), to finance and build its port and mine.

In the Weekend Australian, resources writer Robin Bromby had summed up the mood among observers by declaring: “Andrew Forrest has pulled off what must be one of the most breathtaking deals in our mining history – he has talked the Chinese government into almost fully financing his $1.85 billion Pilbara iron ore dream. And he has done it without giving away a single share in his Fortescue Metals Group.” (Emphasis ours)

What started in 2004 as a series of “please explain” inquiries by the ASX culminated in ASIC8 announcing they were suing Forrest and Fortescue in the Federal Court two years later, alleging Forrest had breached his duties as a director by referring to the construction deals with Chinese companies as “binding contracts”.

While he won that case, with the decision handed down in late 2009, he would lose on appeal when the case came before the full bench of the Federal Court the following year.

Forrest appealed the decision to the High Court of Australia.

This was another instance of Forrest having the wind at his back at the right time. By the time the case reached court, Forrest had pockets deep enough to hire the best legal minds in the country to defend him.

Additionally, by that stage, FMG had a mine in production. It was hard to argue the contracts to build the infrastructure had not clearly been binding.

Winners are grinners How FMG lost some battles but won the war

Pilbara, present day.

Fortescue is a very different company from that of 2008.

FMG has worked hard to develop a diverse work culture – according to recent reports5 females constitute 17.3% of their workforce while Indigenous Australians account for 15%.

They have also implemented a number of programs which underpin their corporate responsibility. One example is their Billion Opportunities program commenced in 2011 as an initiative to generate business opportunities for Aboriginal people.

But the real story is in the numbers.

FMG now have four operating mines: Firetail and Kings Valley in the Solomon hub and Cloudbreak and Christmas Creek in the Chichester hub.

Their cash costs have been declining YoY since 2012 and now sit at USD 12.82 per wet metric ton (wmt).

Additionally, their ore output (measured in million tonnes per annum or mtpa) has risen considerably over the years. Here’s a chart we’ve thrown together which illustrates these two important trends:

Production is usually quoted in terms of wet metric tonnes (wmt), and the iron ore price is based on dry metric tonnes (dmt)

To adjust from wet to dry tonnes, an 8% reduction is applied to the wet tonnes to adjust for moisture content

Source: FIIG Research

The ability of FMG to become a 155 mtpa producer while shaving production costs YoY has seen them weather the storm of sustained lower ore prices and cement their position as a force in iron ore.

The dark days of 2012 are now a distant memory.

In the most recent half-yearly financial results, Fortescue reported NPAT of USD 681 million and net debt of USD 3.3 billion (including USD 8.92 million in cash), representing a net gearing level of 25%.

Additionally, since paying a maiden dividend in 2011, FMG has now returned in excess of AUD $1.20 to shareholders.

FULL DISCLOSURE: FMG are not an Equity Guru marketing client. We have no affiliate links with Amazon. The author holds no position in FMG at the time of writing but has traded the stock on numerous occasions over the past decade.

Footnotes:

1. Burrell, Andrew. “Twiggy: The High-Stakes Life of Andrew Forrest”. Black Incorporated, 2013 – Ch 8 Burke’s Backyard

2. Source: Company presentation: 8th China International Steel and Raw Materials Conference Quingdao October 2008

3. Chessell, James. Sydney July 18 2003 “Forrest has grand $1.2bn plan for tiny Perth mining company” (NB: Possible paywall)

4. The Blue Sky Miner research note was published when Aitken was working for Southern Cross Equities back in 2007. His follow up note titled Fortescue: all systems go published a little over a year later can be found here.

5. Source: Company Presentation: Diggers and Dealers 2017

6. Sourcing accurate historical share price data for FMG over the past 15 years has proven difficult. I personally recall the shares trading below AUD $2.00 at their nadir. Reuters agrees. Some data providers seem not to have adjusted their data accurately to account for the stock split in 2007. The MarketWatch chart provided gives a good sense of the trend since 2003, which is what we want to convey.

7. According to Forbes, “his net worth peaked at $12.7 billion in June 2008 when Fortescue shares hit an all-time high.”. As of 2 July 2018 Forbes reports his net-worth to be 3.7 billion. The 2018 AFR Rich List has Forrest ranked 8th with 6.1 billion. Who do you believe?

8. ASIC – Australian Securities and Investment Commission. The Australian corporate regulator who oversee corporations as per the Corporations Act 2001.

9. As per (6) pinpointing the exact ATH (all-time high) of FMG securities is now haphazard at best. An smh article states “over $12” while Reuters reports a June 1, 2008 high of AUD $13.15 which equates to a pre-split price of $131.50 for the purposes of Aitken’s prediction.

10. Under the ASX stock ticker AMS. The ticker was changed to FMG effective 5 August 2003.

11. NB: Iron ore pricing data: Statista.com. Chart data displays the average commodity price for iron ore from 2003 to 2017.