Brand new companies often post eye-popping revenue increases.

Here’s how it works: if Pens Inc. sells a single $1 pen on December 31, then three pens on January 1 – and no more pens for the next 364 days – it’s a still a 300% yearly revenue increase. That doesn’t make Pens Inc. a great investment if the company’s burn rate is a $100,000/month and the pens are ugly.

So – at first glance – Quadron Cannatech’s (QCC.C) 972% yearly revenue increase should be taken with a grain of salt.

However, as we drilled into the audited report, we discovered that Quadron had a high initial revenue baseline (for an innovative company in a frontier industry), and the slope on the financial data suggests that something remarkable may be brewing.

However, as we drilled into the audited report, we discovered that Quadron had a high initial revenue baseline (for an innovative company in a frontier industry), and the slope on the financial data suggests that something remarkable may be brewing.

QCC has a market cap of only $9.8 million. If the current sales trend continues, it’s going to be a “growth stock”.

To review, Quadron is a Canadian micro-cap company focused on the “picks and shovels” end of the cannabis market. QCC doesn’t grow pot. Or sell pot. It provides extraction processing and delivery solutions including vape pens and capsules.

Unlike many of the cannabis start-ups, Quadron has real products and sales. On May 2, QCC received a $305,000 order for its custom branded vape pen units and cartridges.

Equity Guru principal Chris Parry is a big believer in Quadron’s CEO Rosy Mondin:

“Mondin co-founded the Cannabis Trade Alliance of Canada. She’s an advisory board member of the Canadian Association of Medical Dispensaries. She’s who Jodie Emery would be if Jodie Emery was A) not relentlessly self-obsessed, B) not married to a jackass. Mondin is the reason I invested in the company back when it was private. I signed the cheque and never questioned the decision.”

Let’s get back to the numbers.

On August 30, 2017, Quadron reported its annual financial and operating results for the year ended April 30, 2017.

Year-end Highlights (audited):

- Revenue for the year of $1,789,188, a 972% increase over 2016 revenue of $166,823;

- Gross margin for the year of $502,320 (28%);

- Loss and comprehensive loss from operations of $1,987,088 for the year, which includes a one-time charge of $1,344,713 related to the acquisition of Cybernetic;

- Working capital of $2,043,408 as of April 30, 2017; and

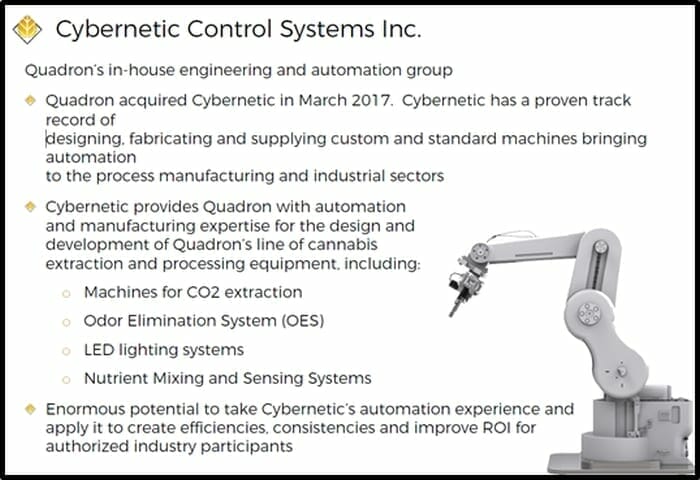

- Acquired automation design firm, Cybernetic Control Systems (“Cybernetic”). Qq

You dumb that down, you get surging revenues in an unprofitable company. But if you remove the one-time charge of $1.3 million for the acquisition of Cybernetic, the yearly operational loss shrinks to $642,000 – which is modest for a company less than a year old.

By way of comparison, Uber has raised $12 billion from investors in the last decade. Bloomberg values the ride-sharing company at $70 billion. But Uber still loses $6 million per day.

Cybernetics has developed high-tech automation and sensing expertise, which can be integrated into cannabis extraction and processing equipment.

But the technology has wider applications. A couple of weeks ago, Cybernetic secured two software automation and control panel contracts from a US entertainment theme park operator.

We believe Quadron’s most significant catalyst for medium-term future revenue growth is the signed letter of intent (L.O.I) with Lucid Labs – a Washington-based tech and licensing company that is developing and commercializing extraction and processing solutions.

We like this partnership with Lucid Labs for a few reasons: 1. Lucid Labs has an existing distribution network on the west coast. 2. Sales of equipment will be a revenue share between Lucid & Quadron. 3. QCC and Lucid will co-develop new processing/extraction equipment. 4. Lucid Labs is already a player in the cannabis space.

“Lucid Labs is an excellent strategic partner with a well-established footprint in the Western United States,” stated Mondin. “We are excited to expand our revenue base into the growing U.S. market.”

Here’s the skinny: Quadron is a newborn – still bathed in amniotic fluid. The company listed on the CSE in late February 2017, acquired Cybernetic in mid-March and signed the deal with Lucid Labs on August 1 – a full 31 days ago.

“We expect to see revenue growth through the course of this year,” stated Mondin. “Quadron is better positioned now than it has ever been to benefit from the significant growth opportunities across our entire business portfolio.”

While the US Cannabis Market is growing exponentially, the growth rate is not dispersed evenly over the entire sector.

In Washington State, for instance, the sales of cannabis concentrate have grown to over $140 million in just two and half years (compared to $3.4 M sold in the first year).

“Cannabis oil consumption is estimated to grow 100X times faster than dried marijuana consumption,” confirmed Mondin, “Many cannabis growers do not have the equipment or expertise to deliver a highly consistent, branded, end product to their customers leaving a critical void in the market which Quadron aims to capture.”

Should we be impressed with Quadron’s 972% yearly revenue increase?

Probably.

Should be concerned, that after 6 months as a public company, QCC is not yet turning a profit?

Probably not.

After all, the “World’s Biggest Store” – Amazon (AMZN.NASDAQ) just turned 20 years old. It’s only had about 9 profitable quarters. But it’s gone into cloud-computing, movie-making and running airlines. AMZN is now valued at almost half a trillion dollars.

Full Disclosure: Quadron Cannatech is an Equity Guru marketing client. We are also investors.