A couple of weeks ago we published an article about Potash Ridge (PRK.V) called, “Nobody’s talking, nobody’s selling – that’s a good sign”.

In the article, Chris Parry wrote:

“In October 2016, PRK was a long way less developed, had a lot more risk, and was worth about 140% more. Today, as it continues to do its business and roll closer to a production scenario, it’s sitting here at a $19 million market cap, with off-take deals signed and resource estimates posted.”

Parry’s instinct was right – it was the calm before the storm.

People are talking now.

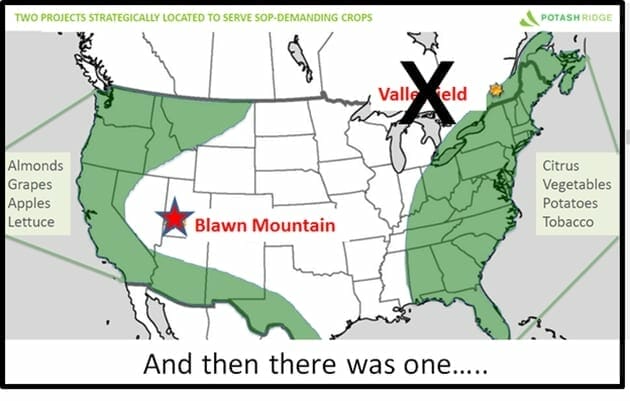

On September 20, 2017 Potash Ridge announced that it is “in the best interest of its shareholders that the Valleyfield Fertilizer Corporation be spun out from PRK into a separate publicly traded vehicle.”

In the wake of the news, 11.5 million shares traded hands (10 x the normal volume).

The buyers and sellers were like two armies of drunks shouting at each other from opposite sides of a lake.

When the mist finally cleared, no conclusion had been reached.

As of this writing, the PRK stock price is .13 – a penny lower than its pre-spin-off announcement level.

As though anticipating the conflicted response, Potash Ridge released an unusually detailed, nuanced statement, explaining the rationale behind the spin-off.

After reminding us PRK has two de-risked advanced development stage SOP projects, it added that the projects are “fundamentally different in size and scope”:

“The Blawn Mountain project is a large scale mining operation and the Valleyfield project is a smaller scale manufacturing plant. The variance between the projects makes them appeal to different investor groups on a regional, national, and international level. [emphasis ours].”

We aren’t 100% in agreement with the “different investor groups” argument.

When you boil it right down, there is only one investor group: financial risk-takers who want to grow their capital.

Weed, lithium, block-chain, gold, fertilizers – micro-cap investors are typically sluts – they’ll hop energetically from bed to bed, chasing a cheap thrill.

However in the September 20 press release, PRK makes a deeper point which we agree with 100%:

“The value of PRK does not reflect the combined value of its two assets, therefore it is in the best interest of its shareholders that the Valleyfield Fertilizer Corporation be spun out from PRK into a separate publically traded vehicle, a change which management feels would better reflect the value of the Company’s assets moving forward.”

There are about 5,000 micro-cap companies all vying for our attention. With mobile devices, Netflix, Virtual Reality, 24-hour news-cycles – investor band width is now microscopically thin.

We know Apple (AAPL.NASDAQ) makes I-phones, Google (GOOG.NASDAQ) operates a search engine and Exxon (XOM.NYSE) pumps oil – but the little companies (under $250 million market cap) have to remind us who there are and what they do.

The statement “We do X” is always a more powerful message than “We do X and Y”.

The irony (and possibly the cause of the market’s self-cancelling opinion) is that both the Quebec and Utah assets are set up to create premium SOP fertilizer – which is used to boost production of crops including tomatoes, spinach, strawberries and avocados.

SOP is about 300% more expensive than its more plentiful cousin, MOP.

SOP potash demand is surging. According to the World Bank, farmers will need to produce 50% more food by 2050 to avoid a global famine. In Q2, 2017 North American SOP prices exceeded CAD$800/tonne.

Sooner, rather than later, the Valleyfield asset will be gone from the PRK portfolio. But like a stressed out girlfriend announcing her boyfriend’s eviction – PRK hasn’t committed to a date or a method.

“The format and mechanics of spinning the Valleyfield project out as a separately traded vehicle may take many forms and the Company is reviewing several options including an equity spin out in favor of the shareholders of PRK, a sale for cash and equity, or a joint venture. The Company is currently in discussions regarding each of these options.”

There is no question: Blawn Mountain is a world-class SOP project, with high production capacity, long life-of-mine and competitive operating costs. The engineering is complete and PRK is now doing metallurgical testing to commercially exploit the alumina content in the tailings.

An April 2017, NI 43-101 compliant pre-feasibility report (PFR) included the following highlights:

- PFR predicts Blawn Mountain lowest cost producer of SOP in North America.

- Average net cash operating costs after by-product credits of $177/ton of SOP.

- Projected after-tax net present value of $482 million.

- Established “Proven & Probable” mineral reserves of 153 million tons.

- Geochemical modeling predicts 19 million tons of M&I alumina resources – worth a couple of billion dollars at current spot prices.

- An average of 255,000 tons of SOP per annum during first 10 years of operation – generating about $150 million a year in sales.

The market seems in a bit of a muddle about this proposed spin-off.

We aren’t.

A simpler message is a good thing.

FULL DISCLOSURE: Potash Ridge is an Equity Guru client. We own stock, we’re buying more.

Hello when can we expect any updates on both projects?

Now trading at 10 cents a share, seems like a rock bottom price

Chad, your are right, Potash Ridge looks cheap. The supply story is real. This company is real. Potash is not a sexy commodity now. I believe it will come back. Potash Ridge is no longer an Equity Guru (EG) client, which does not mean that we don’t like the stock. We often write about good companies like Potash Ridge, that aren’t clients, or that are former-clients. An official EG update is not forthcoming simply because we are swamped with new clients, blockchain, technology, weed, oil…