Revive Therapeutics (“RVV.C”) is a life sciences company that focuses on the research and development of therapeutics for rare disorders and infectious diseases. and it is prioritizing drug development efforts to take advantage of several regulatory incentives awarded by the U.S. Food and Drug Administration (“FDA”) such as Orphan Drug, Fast Track, Breakthrough Therapy and Rare Pediatric Disease designations.

We’ve talked about these guys a great deal over at Equity.guru and I thought I’d give them the same treatment I gave Aequus Pharmaceuticals (“AQS.V”) yesterday on ‘The Equity.guru Investors round table’. We talked about the 6 filters that help me filter through the many publicly traded companies and pick the ones I want to entrust with my life savings. Today RVV will receive the same service!

The 6 Filters

5-year Revenue Growth (“CAGR”): NA

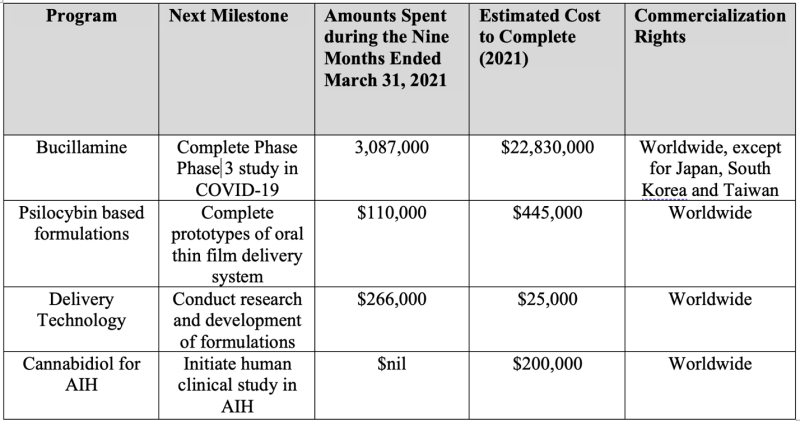

There was no track record for me to do the compounded annual growth rate for these sales over the last five years because the business has not generated any revenues. Majority of their pipeline is still going through the phases to commercialization and once these objectives have been met the company will begin to make sales on this product using a dedicated Salesforce and marketing techniques.

As for now a key driver for their sales revenue would not be price or volume adjustments but (i)monitoring the cost associated with each stage of development and (i) the current level or stage of development of each product line.

5-year Operating Loss Reduction (“CAGR”): 7%

From 2016 two 2020 the operating loss increased by 7%. Majority of the increase in expenses came from stock-based compensation, which went from 4% to a high of 28% of the total expenses, that increased 54 percent over the last five years from $120,000 in 2016 to just above $1,000,000. Selling and general administrative expenses increased by 16%, recent development expenses decreased by negative 22% and depreciation increased by 25%. selling and general administrative expenses went from 37% to a high of 90% during this period and then dropped to 58% in 2020. Research and development expenses went from 58% of the total expenses to 12% in 2020.

At first glance the excessive use of stock-based compensation is alarming especially due to the trend only worsening at the beginning of 2021. For the nine months ended March 31, 2021, the company’s been a total $4 million on stock-based compensation which equaled the research and development costs of $4 million. The company states in their notes to be a financial statement that:

“ The Company has granted options for the purchase of common shares to its directors, officers, employees and certain consultants. The purpose of the plan is to attract, retain and motivate these parties by providing them with the opportunity, through share options, to acquire a proprietary interest in the Company and to benefit from its growth. These options are valid for a maximum of 10 years from the date of issue. Vesting terms and conditions are determined by the Board of Directors at the time of the grant. The maximum number of options to be issued under the plan shall not exceed 10% of the total number of common shares issued and outstanding.”

$2,570,357 of those stock-based rewards went to directors and key management personnel including Chief Executive Officer and Chief Financial Officer of the Company.

Quick Assets over Liabilities (“Current Ratio, Quick Ratio, Total Liabilities /Assets”)

The company does not need a lot of assets and only needs a head office or a distribution centre, a sales force in marketing team including the corporate executives and cash to utilize in the research and development of its products. As such they have a relatively “boring” balance sheet. In their latest reporting period ended March 31st, 2021, they had $19 million in cash and close to $100,000 of property plant and equipment on their balance sheet. Since they are in the business of commercializing pharmaceutical product, they do have a balance of $12 million of intangible assets also including goodwill from acquisitions.

5-year Cash flow from (used) in Operations Growth (“CAGR”): (5%)

Since the firm is still in its development stage it is not generating a positive operating cashflow position just yet. At its current production levels, it is using more money than it is generating and must utilize equity financing another debt obligations to fund its day-to-day. over the last five years that cash flow used in operations has grown by 5% from 2 million in 2016 to 2.52 million in 2020 and as of the last 12 months it’s gone up by 6 million.

5-year Share Dilution (+) or Accretion (-): +36%

Like I mentioned in filter 4 the company is not generating any cash of its own, so it must dig deep into investors pockets to fund its day-to-day operations another strategic investments and research projects. Over the last five years the shares have been diluted and increased by 36% from 2016 to 2020 as of the latest filing they had a total of 230 million shares outstanding compared to 24 million shares outstanding at the beginning of 2016.

5-year Return on Invested Capital (“ROIC”): -196%

The return invested capital is also relatively low because the company is still ploughing money into future sales streams by investing heavily in research and development and the commercialization phases for its flagship products. over the last five years the return invested capital has been negative 196% but the trend is on the positive side as of the last 12 months they return on invested capital is -48%.

The company did fail on five of the filters and passed the balance sheet filter. this doesn’t mean the company won’t succeed in the future, but it means there are way more permutations on the possibility of what the present business will be like as it tries to commercialize it operations. These various uncertainties are what makes valuing early-stage business is very difficult and sort of an art and less of a science. Although they don’t pass on all filters and trust me not all companies pass all six filters, them having quite a conservative balance sheet means that the company just needs to utilize its current pool of cash of $19 million to invest incremental cash productively and return a high incremental rate of return on invested capital. the key here being the incremental cash being invested.

From this my conclusion is that I would skip further research on the company but put it on a watchlist and wait for more business developments to happen probably the commercialization of its first pharmaceutical products.