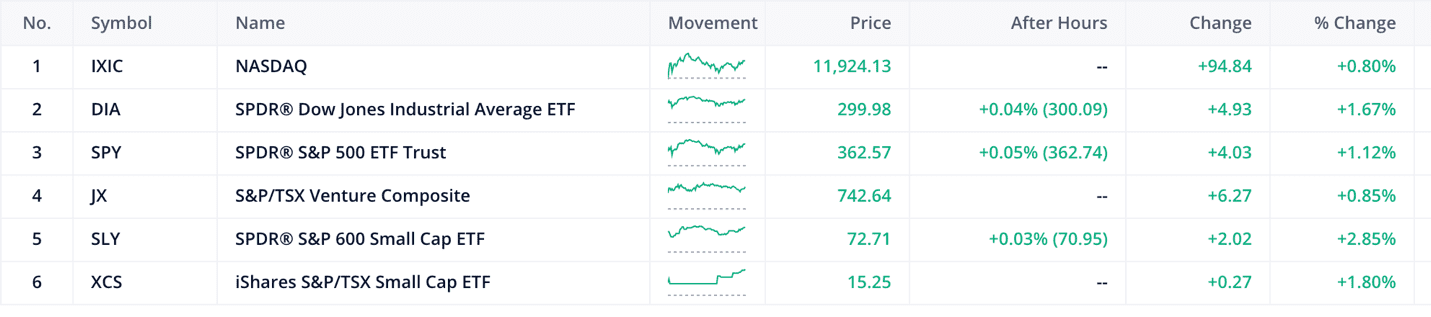

- The S&P 600 & TSX20 are up by 2.85% and 1.80% respectively

- Bonds see a rush of capital outflows as investors move into ‘riskier’ assets.

- The Canadian 10-year bond up by 0.01% and the US 10-year bond down by 0.01%

Today’s pick of the day is Crescita Therapeutics.

Crescita Therapeutics Inc (CTX) is a dermatology company, that provides non-prescription skincare products and prescription drug products for the treatment and care of skin conditions, diseases, and their symptoms in Canada, the United States, and internationally.

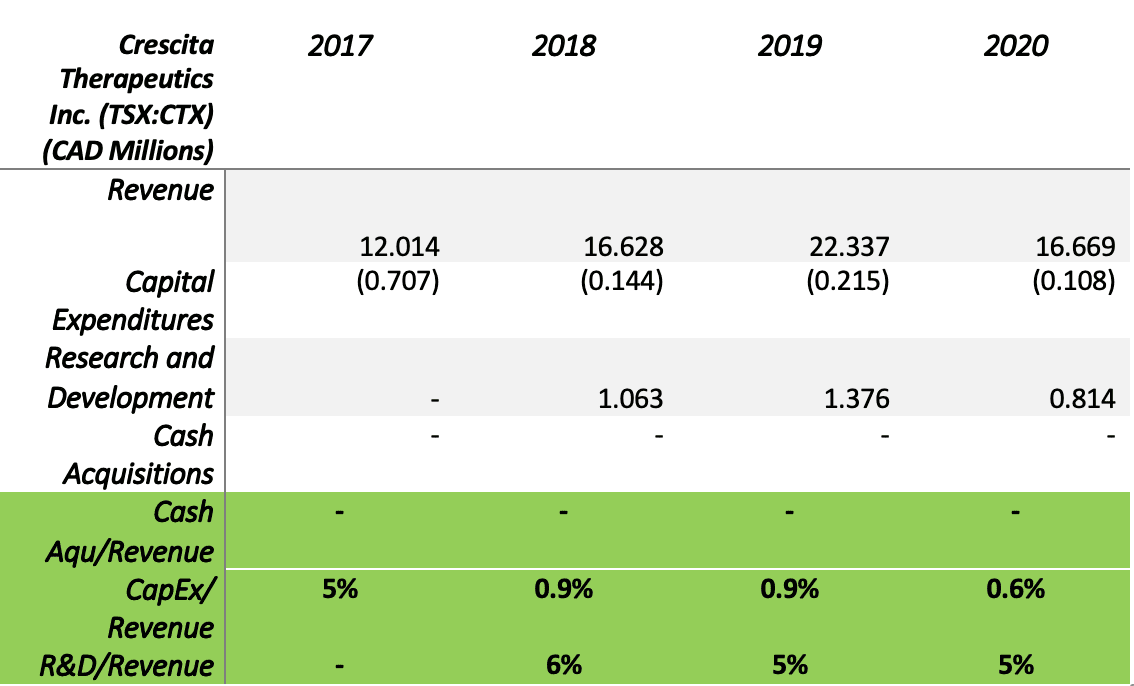

In 2019 Crescita produced a total of $23 million in revenue and it cost them $5 million to produces this business. This translates into a gross profit margin of 70%. Meaning for every dollar that they produced in revenue, they kept 70 cents. This might not seem that amazing but when you compare with the industry average of 46% you can now appreciate this excellent business performance.

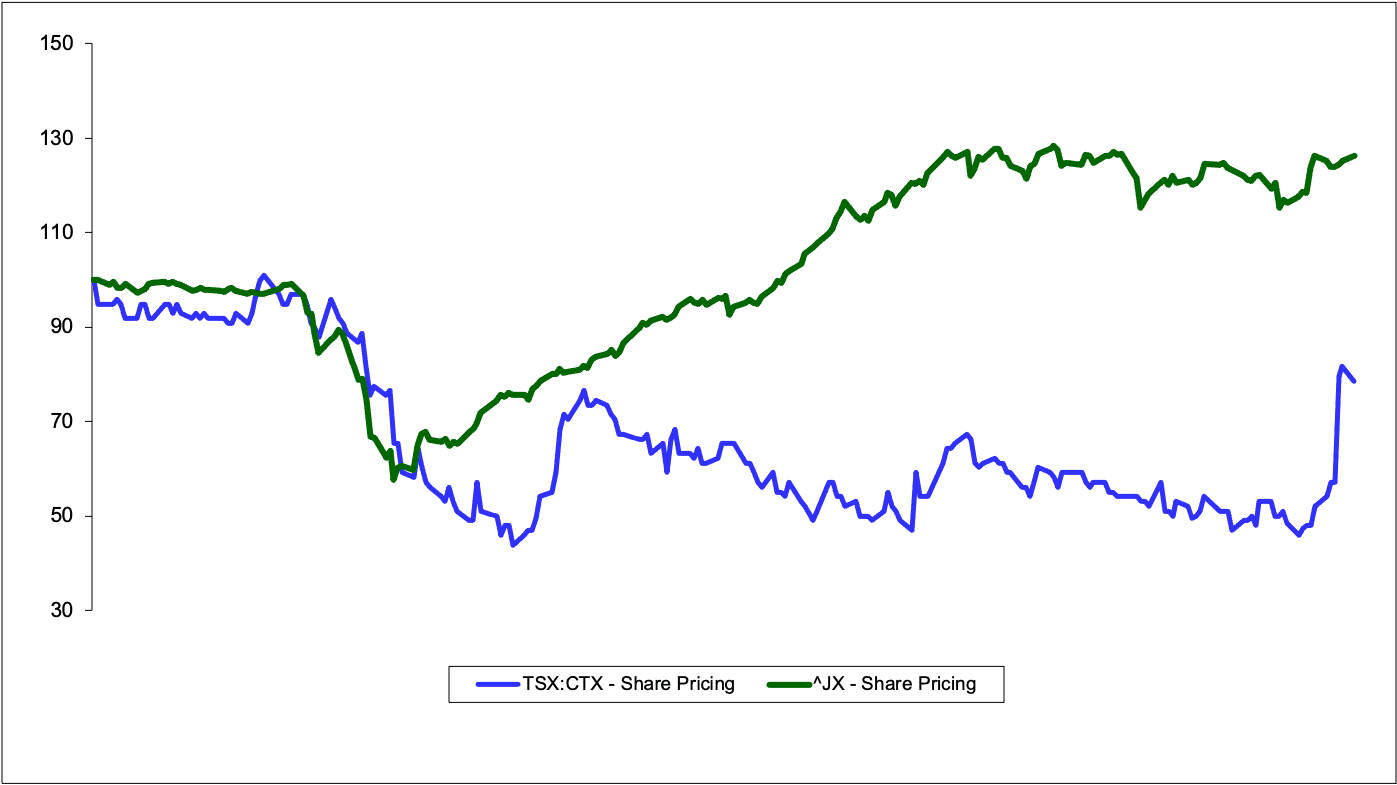

The big question on our minds should be, has this business efficiency translated into stockholder value? The simplest way to measure this is by comparing and contrasting the return of Crescita(CTX) versus the general market, specifically the S&P/TSX Venture Index.

From the chart below it is pretty evident that the stock of Crescita has been destroying value instead of creating value over the last year. But this makes no sense compared to the business performance, but a deeper dive into the firm sheds light on the fact that the market ‘might’ be wrong.

Before we dive deep into the fun stuff and look at the financial statements I thought it would be relevant to take a look at some of the key assets that Crescita owns. Doing this shows us how the management team at Crescita plans to keep competitive in its industry. With a gross margin of 70%, it is highly likely this sort of profitability will attract competition.

It owns various proprietary drug delivery platforms, including :

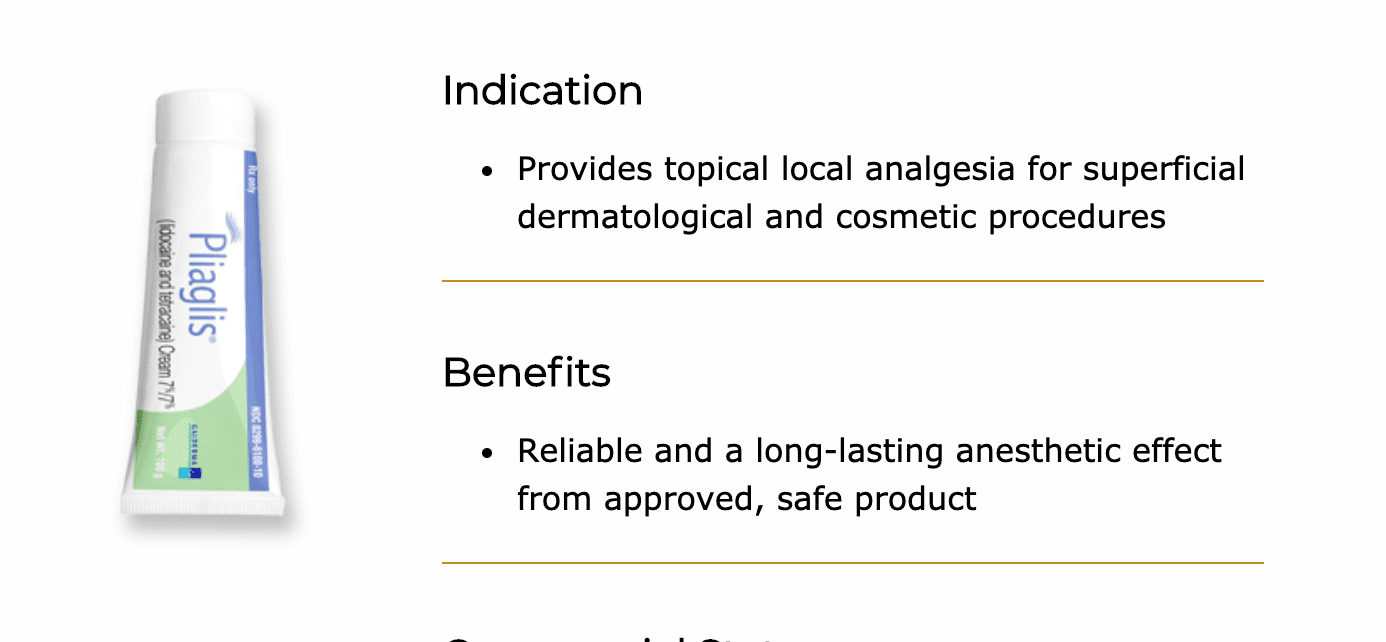

Pliaglis

Their flagship asset is Pliaglis cream which is the first and only approved FDA topical anesthetic that combines the highest concentration of two powerful ingredients Lidocaine and tetracaine {7%/7%}.

Its unique formula is applied as a cream that allows for a simpler and smarter transfer from anesthesia to the procedure. It is designed to improve dermatology procedures. Dermatology is the branch of medicine dealing with the skin. It is a specialty with both medical and surgical aspects.

Without going into too much of the science we can see that this is a ground-breaking discovery for the firm and allows dermatologists the ability to improve the efficiency of their operations. Being the only FDA-approved topical anesthetic it gives Crescita a competitive head start.

Their second asset would be their Alyria line of products.

Alyria is a respected cosmeceutical brand of elegant and effective skincare products that target major skincare concerns. It is believed to help patients achieve healthier, younger-looking skin with visible results.

Alyria is a respected cosmeceutical brand of elegant and effective skincare products that target major skincare concerns. It is believed to help patients achieve healthier, younger-looking skin with visible results.

Alyria products are available exclusively to physicians. Alyria’s portfolio is complementary to the Company’s existing Pro-Derm line. Pro-Derm line specially formulated for rejuvenation, anti-aging, and improvement of the most common skin conditions. It contains high-quality active ingredients that are often used in combination with or pre & post medical procedures.

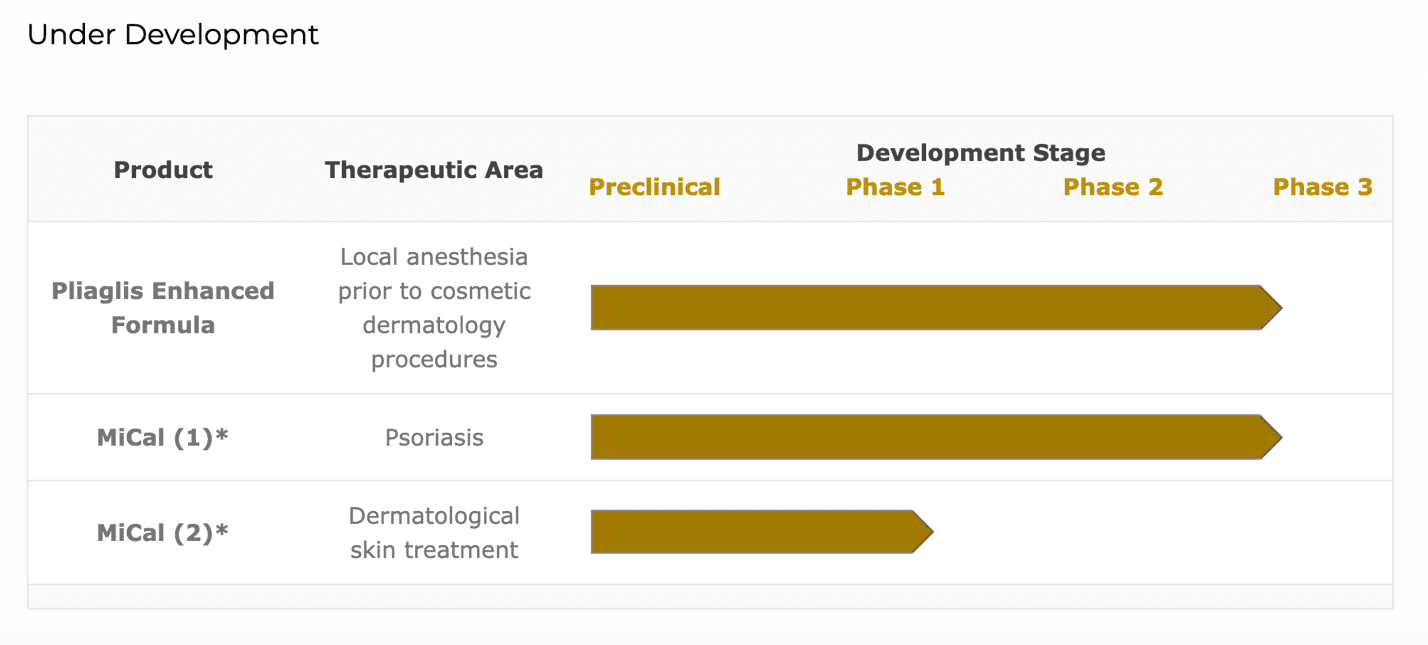

Crescita also has a strong pipeline of products in Phase 1 and Phase 3 of product development.

These products have the potential to boost the companies top line at the same time improving the diversity of revenue streams.

Having briefly touched on the various product lines available and those in the pipeline, it is easy to see how Crescita has been able to generate close to $20 million in revenue and is able to continue to generate this amount of business in the future. As of 2020, it has been able to garner $16 million in revenue amidst the COVID 19 global pandemic. This can only be possible if they have a strong competitive advantage.

Intellectual technology and property

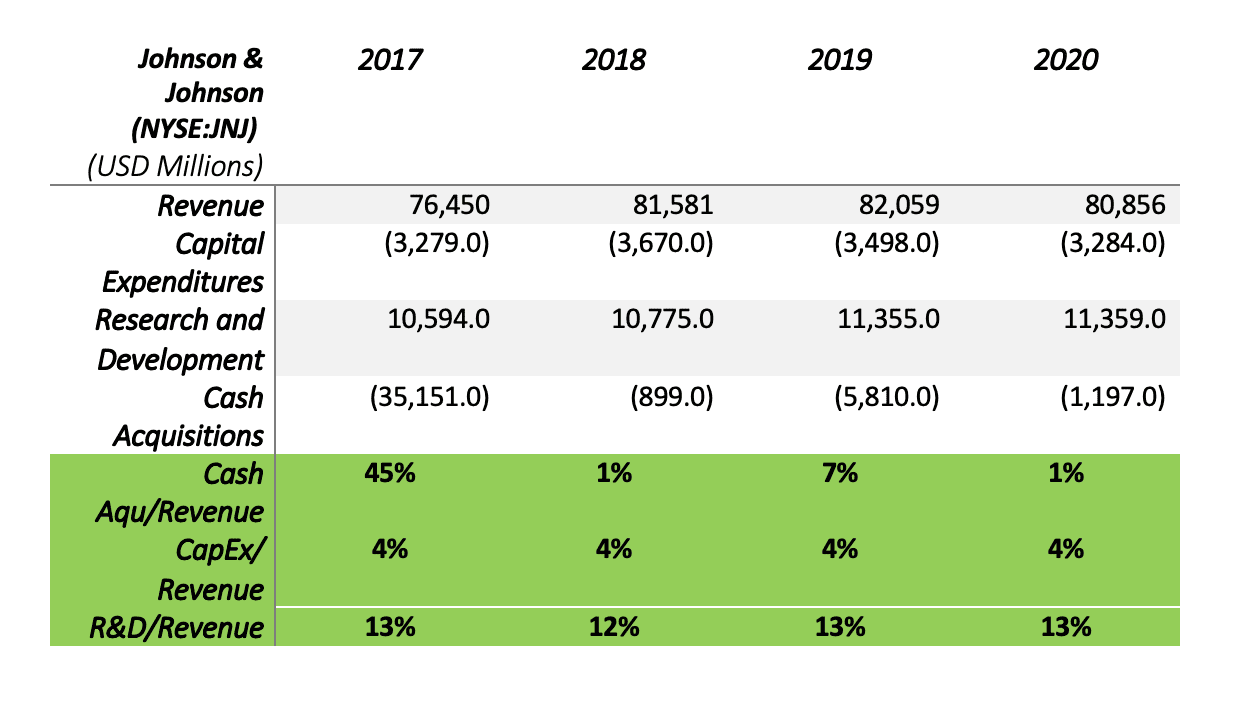

The Pharmaceuticals industry is one of the most competitive industries. Some of the industry leaders like Johnson & Johnson (NYSE: JNJ) have been able to sustain a competitive advantage because of the sheer amount of capital they have to invest in research and development. These days JNJ does not put that much money into R&D, as of 12 month period ending in September 2020, they have spent a total of $11 Billion in research but have been very active in business acquisitions spending a total of $35 Billion in 2017.

For the eager investor, we have added two tables that compare and contrast two firms in different sectors but the same industry.

To start the analysis, we have Crescita which is in the business of commercializing the drugs. Crescita will invest heavily in products that are already in Phase 1 or Phase 2 of the product development stage. This avoids the need to spend millions of dollars in research and development and they only need to deploy capital to sustain the business infrastructure.

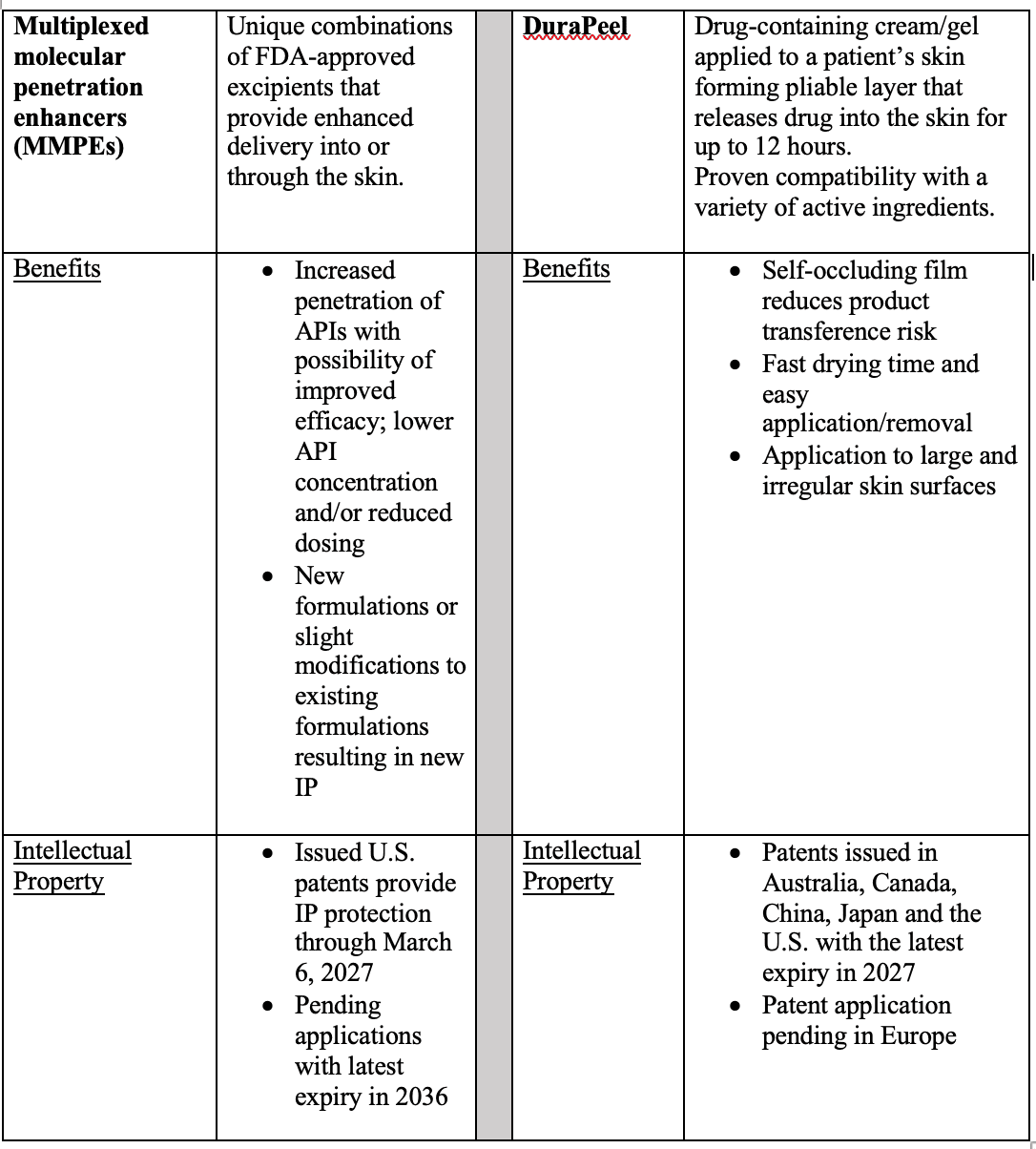

The majority of the capital deployed by Crescita goes into their MMPE and DuraPeel application technology.

On the other hand, Johnson and Johnson are obviously in the business of acquiring smaller pharmaceutical companies instead of commercializing drugs. They seem to have pivoted their business model because it costs more to commercialize drugs and do the research and development whilst waiting for FDA approvals.

For JNJ it seems more profitable to spend a lot of the money they make on acquisitions and they do this once in a while. For example, in 2017 and 2019 from the table above.

This has allowed them to diversify their revenues at the same time spending less and less on research and development. This unique business model has allowed Johnson and Johnson to reduce their research and development or better said keep their research expenses steady as revenues have grown over time.

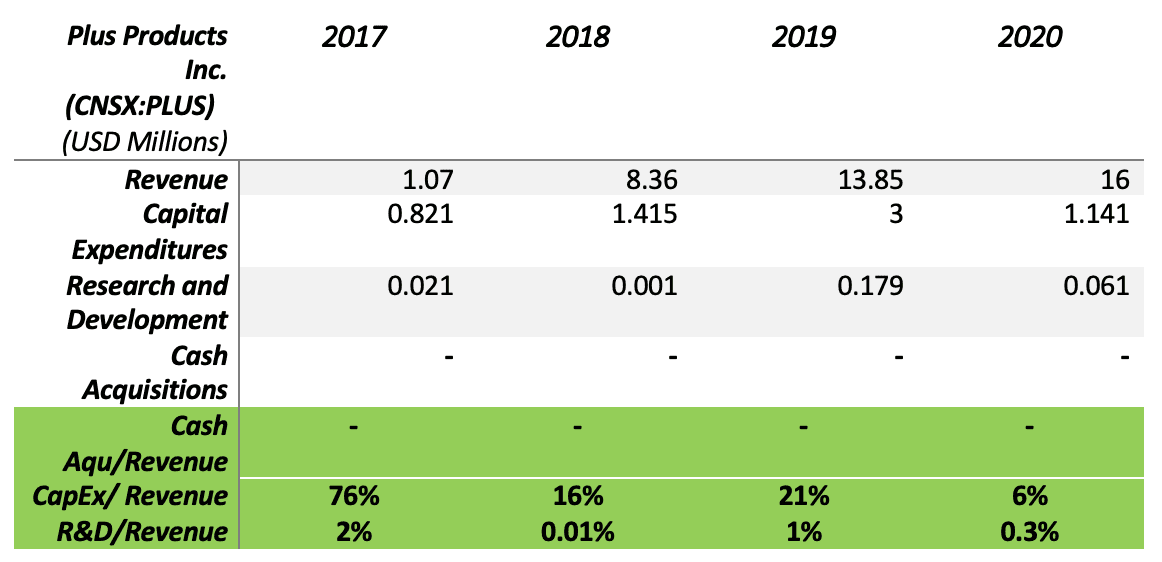

Obviously, the above comparison is used as an example and should not be taken as hard science. The investor would need to contrast two similar businesses, we would suggest a company somewhat similar in size for example Plus Products Inc(PLUS). We have provided the table below for comparison.

The analysis above is brief but can be used as a starting point for the research on the Pharmaceutical industry. But brief as it maybe it has the ability to show how the different business models in the industry are being applied and if they are profitable.

With a unique business model and an ability to keep costs low at the same time retaining a large portion of the revenue to reinvest in more productive assets like the ones in the product line. This has given Crescita the ability to stay the course and they hope to be a going concern in the future whilst creating shareholder value.

The dispersion between the fundamentals of the business and the stock price could be caused by two main factors. The first being how difficult it is to understand the industry because of all the jargon involved. The second factor would be a misunderstanding of the economic structure of the industry and how it affects profitability due to the different business models used by all the firms.

But again, this is merely a guess. The reality of the beauty contest that is the stock market is that if every stock is somebody’s favorite, then every price should be viewed with skepticism even those that may seem like risk-free investments.

HAPPY HUNTING!

Legal Disclaimer The information on this article/website and resources available or download through this website is not intended as and shall not be understood or constructed as financial advice. I am not an attorney, accountant, or financial advisor, nor am I holding myself out to be, and the information contained on the website or in the articles is not a substitute for financial advice from a professional who is aware of the facts and circumstances of your individual situation. We have done our best to ensure that the information provided in the articles/website and the resources available for download are accurate and provide valuable information for education purposes. Regardless of anything to the contrary, nothing available on or through this website/article should be understood as a recommendation that you should consult with a financial professional to address our information. The Company expressly recommends that you seek advice from a professional.