With the Bank of Canada’s announcement interest rates would hold steady at 1.25%, the housing-rich masses in Toronto and Vancouver breathed a sigh of relief I could hear across the straight in Victoria.

Real Estate and Real Money

If you live in the 604 or 416 area codes you know the housing situation defies logic. I thank my lucky stars I live in only the 3rd or 4th most expensive market in the country. One of the major drivers of this price expansion has been the historically cheap money fuelled by low interest rates.

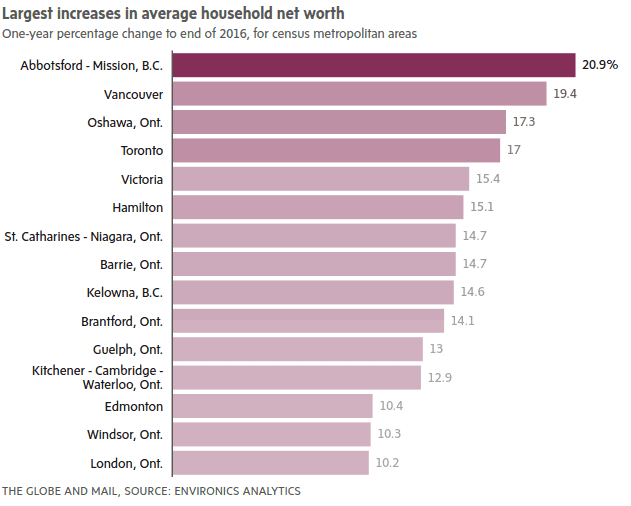

In November, the people over at the Globe and Mail Economy pages had the bump in the average Canadian’s net worth at 12%, with much larger pops in urban markets.

There are a million blogs and column inches devoted to the housing bubble in Canada – so I won’t bother going into the whyfors and predicting the future – but a growing market needs investment capital. The housing market has plenty of that and, to a degree that nobody can really quantify, it bleeds into small cap.

According to the annual WealthScapes report from Environics Analytics, national household net worth rose 12 per cent over last year to $770,635, while household debt grew 4.4 per cent. Canadians also increased their savings by 5.6 per cent and their investments by 13.2 per cent last year.

Individual investors are present at every stage of the growth (and collapse) of small cap stocks and, without them, institutional investors aren’t interested. The small and micro cap stock ecosystem is essential habitat for the cannabis, energy metals and tech / software / crypto sectors as we know them. It needs stock pickers, message board posters and degenerate action junkies for more than just their capital. This system runs on interest and it runs best when that interest is spread widely, without getting too thin.

The degree of market participation is a function of availability of capital, and the average retail investor’s available capital has a lot to do with the shape of his or her home equity investment. So it’s important for a savvy investor to keep an eye on the housing markets, and the BoC’s prime interest rate, because here’s what happens when the rate does start going up…

You want interest? OK I’M INTERESTED

When the prime rate goes up, the bank mortgage rates go up, and everyone who needs to renew their mortgage will have to do it at the new rates. Homeowners with variable rate mortgages feel it sooner, fixed a bit later, but everyone feels it.

Many homeowners are likely to quit allocating their non-housing savings (and certainly any capital they’ve leveraged out of home equity loans) from their online portfolios in a higher rate environment.

Yesterday’s hold announcement pushes a rate hike off, and low unemployment, inflation at target and an “at capacity” economy (does anyone know how they track that?), makes it seem like there might not be another hike for a while here.

Right now Canada is house-rich and cash-poor and if a spike in interest rates seriously impacts the housing markets, it’ll hit the whole economy, but it’ll be most quickly apparent in the most liquid of markets – public equity markets.