Every work day, I’m pitched multiple companies as being the next big thing. And along with those pitches come all sorts of investor materials and props and charts and even sometimes pretty ladies. Dealmakers will pull every trick in the book to get a guy to pay attention, including drinks, but only one company has ever had a true reason to get the pitchee liquored up.

Eastside Distilling’s (ESDID) pitch meeting was my favourite pitch meeting ever. Even more than the one that was held at Brandi’s with the Mary Elizabeth Parker lookalike and the lapdance tab.

Eastside Distilling’s (ESDID) pitch meeting was my favourite pitch meeting ever. Even more than the one that was held at Brandi’s with the Mary Elizabeth Parker lookalike and the lapdance tab.

Even more than the one in Nassau.

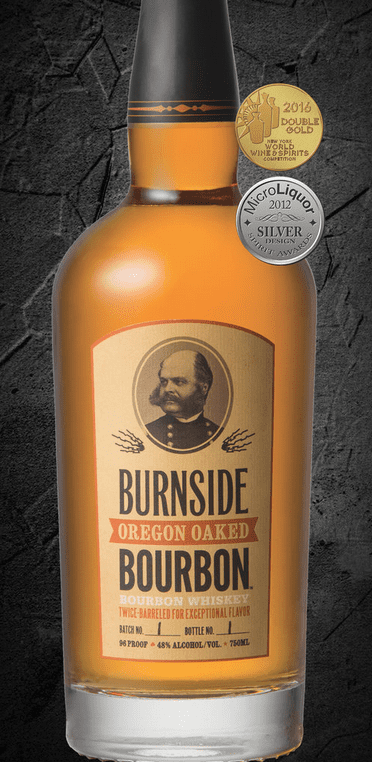

Reason was, Eastside has an amazing line of products that are genuinely superior to those I’ve tried elsewhere. Coffee-laced rum. Marionberry Whiskey. Potato Vodka. Cherry Whiskey. Ginger Rum. And for Christmas: Eggnog Liqueur, Holiday Spiced Liqueur, and Peppermint Bark Liqueur.

These are all artisanally produced at their distillery in hipster heaven, Portland Oregon, and from there, Eastside has quickly become a national brand synonymous with the west coast booze scene.

But that pitch meeting nearly didn’t happen, as our trusty border officials decided to confiscate the first load of bottles brought up for investors, and then hit the second (sent through the night in a panic) with import tariffs three times as expensive as the actual list price of the product. Basically, Eastside had to spend $1000 in duties to bring up $300 worth of product for sampling. O Canada…

So I tried them, we talked to their spirit expert about how they make them and we oohed and aahed at their amazing branding.

Amazing branding like this:

Nope. Wrong photo. Wait a second, I have it here somewhere.

Nope. That’s not it… Branding.

There we go.

These are small batch, hand-crafted spirits and liqueurs created by America’s only female master distiller west of the Mississip’, Mel Heim, and she does not cut corners.

When I tell you this stuff tastes amazing, it’s not just because it got me lit at 10am on a Tuesday once a year ago, it’s because I’ve told friends about it when they’ve gone traveling to Oregon, and they always – ALWAYS – come back with a trunk load once they visit the company.

That success is tracking in terms of sales too, with the company quickly spreading its distribution list across the USA. It just opened Florida, which is a huge market, and is starting to truly become a national brand, which isn’t easy for a bunch of Portlandites who started out with a vat in the back room.

But Eastside lost its way over the last year or so. Not on the sales side, where it continues to run hot, but on the market side. The company had planned to built a big tasting room to help it grow locally, to serve as a showroom for its products and a meeting place for locals, but costs for such a build turned out to be prohibitive – especially as growing a national brand has an upfront cost.

And Eastside struggled to rein in those costs. That’s not a big deal if your stock is running hot – you just go raise more – but the stock struggled initially, because frankly it went public too early, so raising growth money became painful. Debts began to pile up, then those started turning toxic, and a restructuring became necessary. Maybe more than one.

THE COMEBACK

Through all the internal squabbles, and there have been many, the product continued to shine and grab a foothold in multiple states. 21 states, according to their website, including the big guns – New York, Texas, California, and now Florida.

The tasting room strategy wasn’t abandoned, but it was altered – the company built a small room in a mall location that allows it to handle new product testing, additional revs ($95k in sales in a month), and special events.

The tasting room strategy wasn’t abandoned, but it was altered – the company built a small room in a mall location that allows it to handle new product testing, additional revs ($95k in sales in a month), and special events.

In terms of building a proper alcohol brand that can take advantage of the massive acquisition valuations sometimes seen in that space, Eastside has done everything right; its marketing is on point, its products on trend, and its coffee rum on my wishlist. Most craft distillers have three SKUs, tops. Eastside has 14, and that number is evolving as sales numbers give them more and more insight into what consumers are looking for.

In 2012, sales topped $300k. In 2015, they hit $2.3 million. 2016 will be up, but not significantly so, as the company needed to tap the brakes during its backend market and debt retooling. Growth spending all but stopped to give debt retirement a chance to kick in, which is the right play.

In terms of cases sold, 2012 saw 19,200 bottles go out. 2015 saw that rise to 124,000 bottles out the door, which is a significant jump, and a large enough slice of the market that large distributors are taking notice and taking on the product.

But with all that front end success, the back end really needed a big fat clean up. They need to retire that toxic debt, they needed new blood in the boardroom, and they needed new investors willing to finance the last steps of their multi-year growth plan.

This they now have. The company, from what I can tell, has retooled and set itself back on the right course. And as part of that plan, they rolled back the stock.

Boy howdy, did they roll back that stock, with a 20 to 1 split that leaves the deal with just 4,766,659 shares of common stock issued and outstanding.

Take a second now to let that sink in – ESDI (it’ll be ESDID for the next few weeks) is an OTC company with just 4.7 million shares out. That’d be like a TSX Venture company sitting on 1300 shares outstanding. It’s nuts.

And, of course, after an initial burst of activity, the stock took a hiding on the back of that rollback, because investors are rubes.

THE OPPORTUNITY:

I could give you all sorts of stats from the corporate presentation about the size of the industry and how quickly flavoured whiskeys are growing and how craft distilling is catching on and… but who gives a shit.

The opportunity here is not in the sector or the sub-sectors or growth trends or potential. The opportunity here is in the fact that this stock has been oversold and overbeaten and underestimated, and that it is ready to make its move.

I bought Eastside stock this morning at $1.79 because it’s dropped from $2.45 to $1.79 in the last three trading days on absolutely minimal volume, leaving it at an absurdly low $8m market cap. With 42% of stock held by insiders (who will be wanting much more value than this before they start cashing in), you’re looking at about 3 million shares available on the public markets right now.

In my eyes, any sort of low volume buying will catapult it back up, and I think we’ll see numbers by year end that warrant such a move.

On the acquisition side, Cabo Wabo had sold 56,000 cases when it was bought by Campari for $91 million. Zacapa was selling 100,000 cases when it was bought by Daigeo for $200 million. Those two sales put Eastside’s current sales numbers at a worth of $20 million in a buyout.

But there’s an important plot twist in that valuation – the Cabo Wabo sales happened in 2007. The Zacapa sale was in 2010. At that time, nobody had ever used the term ‘craft distilling’ in polite company, hipsters were people whose phones didn’t flip, and boy bands were still a thing that people talked about.

This is 2016. I haven’t consumed a beer that has a production run of more than 1500 cases annually since about 2013. Today, Granville Island Brewery is dismissed by consumers as too big. Today, you’re as likely to buy a beer that has elderberry flavouring and the brewer’s beard hairs floating about in it as you are a Budweiser. Artisanal distilling is no new that the word ‘artisanal’ is highlighted by my spellchecker as not being a word. 37% of whiskey drinkers in the US today … are women.

The world has moved forward, and you best be buying into that.

The largest spirit companies on the public markets have been in negative growth mode for some time, so they’re buying market by acquiring small distillers and brands. Eastside? Growing at 46% a year over the last several.

And there’s room to grow – the existing Eastside set-up has a 100k annual case capacity, which is ten times the current sales rate, so no more cash is needed to cover continued explosive growth.

And, lastly, and this is important folks… they’re the only small craft distiller on the public markets. The only pure play if you believe artisan distilling is a growing and evolving sector that warrants investment.

I like to buy stocks of companies that I do business with, and I spend a large enough amount of my monthly income on craft liquor that I think this is a gimme. So I bought in.

No deal, no contract, no financings. Just bought in, because I believe in what they’re doing, in the sector they’re in, and in the chance of a big swing in the positive direction on that share price.

And the Chairman’s name is Grover Wickersham, which is just about perfect for a brand evoking memories of an America past.

If this thing does what I think it will, the next round is on me.

— Chris Parry

I’m in !