If you’ve been around this joint for a while, you’ll have seen us arguing folks would be silly to invest in MedMen (MMEN.C) if hanging on to your money is a thing you aspire to do.

That’s not because we have a hate on for the dude-bros running the show, or because they’re not a client, or because we’re short sellers, or any of the other 50 or so reasons MedMen homers have thrown at us over the last few years as a rationale for us not seeing the company in the same rose-coloured way they do.

It’s because MedMen is, and has always been, shit.

To this day, we have never been wrong.

The capsule review goes as follows:

From ‘We’re the Apple Stores of weed!’ to the insane self-dealing that went on with the ridiculous management bonuses and voting power handed to the founders when it came public, to the advertising in US states where not only do they not have stores but weed stores aren’t allowed, to the bulletproof cars the company bought for its CEO to the endless stories from former staff describing cluelessness at all levels of management, to tip withholding of minimum wage budtenders, to being called douchebags on South Park and somehow feeling like that’s cool, to revelations of bigotry in the boardroom as part of lawsuits against the company by former insiders, to their dumb ass lawyers deciding to threaten to sue us for saying all the above, but mostly to the next level disgusting amount of spending that has gone unchecked for years now, this has always been an utter shit show.

But all of that pales in comparison to the biggest issue of all:

Management is terrible, pays itself insanely well, and can’t be fired because 1) management owns the voting stock, and 2) the golden parachutes owed to them upon firing would make the bankruptcy-inducing bonuses currently being paid to them look like a child’s allowance.

FEAR NOT: MEDMEN IS COST CUTTING!

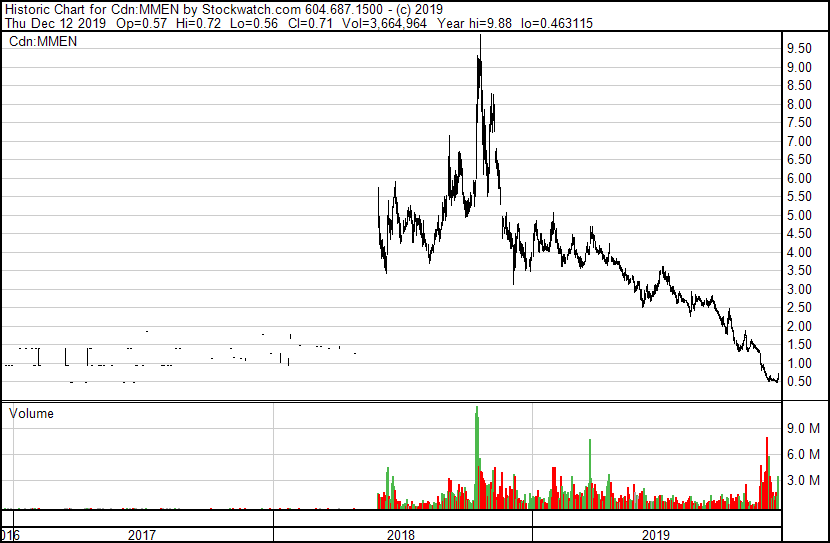

MedMen management is looking to shred some of its quarterly SG&A spend and take it from $85m to $65m, in a hope they can tamp down some of their recent $80m quarterly losses. To that end, there are (among other things) widespread staff cuts happening – just a few weeks before Christmas, naturally, because MedMen decision making has never been alleged to have put its people first.

The revised corporate SG&A target is based on the realization of headcount and cost reduction initiatives. This week, the Company provided layoff notices to an additional 20% of its corporate-level employees. In total, over the past 30 days, the Company has strategically reduced its corporate headcount by over 40%, representing approximately US$20 million in annual salary-related savings.

A few things about that:

1) They’re outsourcing a lot of those people, so the actual cost cutting might not be so hot. To quote the company, “the reduction in headcount does not result in long term reduction in SG&A due to needs to engage outside consultants or advisors.”

2) Either those people have valuable jobs and duties that must be fulfilled and firing them will hurt the company, or they don’t, and their unnecessary hiring in the first place reflects the free-spending habits of the guys at the top.

You know who isn’t being cut?

The guys getting paid most, who have run this thing into the ground EXACTLY the way we said they would on day minus-one.

“The Canadian venture capital markets are a rank pit of vipers that live by sucking on the lifeblood of the foolish, recycling shit into prettier shit, and tapping grandma on the shoulder repeatedly for a financial refill,” said me as this aberration rumbled to the public markets. “But this MedMen (MMEN.C) deal is rank AF.”

[CEO Adam[ Bierman is coming into this deal – stock aside – with $1.5 million in salary, another $15 million annually in ‘incentives’, and $10 million ‘just cus’, or $26.5 million off the top. President Andrew Modlin gets the same deal, so of the $100 million raised in new shares going public, $53 million of it goes straight into the pockets of the big two.

The CFO didn’t do much worse. Also:

..should they need to be removed for any reason, there’s the ‘executive protection’ policy to consider.

That’ll mean Bierman and/or Modlin get three times their salary, five times their bonuses, and a $250k lump sum payment on the first of the following month – and they benefit from this policy for a further three years after they’re terminated.

It goes on:

In the event the enterprise value of MedMen exceeds US$2 billion at any time, Mr. Bierman will be granted a US$4,000,000 cash bonus

And more:

The MedMen presentation and website are very pretty, and that Manhattan store they just opened is very stylish (and insanely expensive), but you’re paying $100m+ for each dispensary they own. Oh – one other thing? If there’s a catastrophe and a liquidation is required, the company documents state the three primary executives mentioned above get their money back before anyone else does.

After pressure from our story saw their stock plunge, and after their threat to sue us for half a billion dollars (which we duly front paged and mocked loudly) sent it further down, the grifters in control decided to alter their bonus schedule, tying some of it to actually increasing the company value rather than having passed a given calendar date.

Those salaries and bonuses are still the biggest line item. But the dudes earning most of the money are not the ones taking a trip to the unemployment office today.

WHAT’S NEW, BROS?

MedMen will no doubt point to Bierman’s announcement today that his co-founder is giving the Chairman of the Board a proxy on his super-voting shares as a sign they’re aligned with shareholder interests.

That’s malarkey.

Co-founder Andrew Modlin has granted Ben Rose, Executive Chairman of the Board a limited proxy in respect of 815,295 Class A Super Voting Shares, which represents 50% of the total Class A Super Voting Shares for a period of one year. Such proxy may not be used to eliminate or change the rights of such shares or otherwise alter or amend the organizational documents of the Company.

Regardless of whether an inability to amend ‘the organizational documents of the company’ is defined as the Chairman having the power to be able to fire him or not, with their golden parachutes, Bierman and Modlin can continue pissing into Gucci urinals for as long as they want, on MedMen’s dime, even as the guy cleaning that urinal is given his walking papers.

That’s because, under Bierman’s guidance, MedMen’s financial state is an absolute mess, and the same announcement that revealed the proxy situation also revealed the company is taking it heavily in the hindquarters in order to bring in the capital it needs to cover the next quarter of losses.

Shaving $20m off the SG&A wont cover an $80m loss. So the company is taking on more debt, at increasingly heavy interest rates, and converting old debt to heavier interest in return for giving it more time to pay that debt off.

Says Bierman:

“Our long-term investors have shown confidence in our strategic direction and industry-leading retail brand. With this strong level of support, we can now further focus management’s attention on maximizing our core assets while also reducing our corporate expenses to achieve positive EBITDA in calendar year 2020.”

Let’s see what that looks like:

Equity Investment: On December 10, 2019, the Company executed a term sheet for its non-brokered offering of subordinate voting shares for aggregate gross proceeds of US$27 million (the “Equity Placement”) at a price per share of US$0.43 with a new strategic investor and an existing investor, Wicklow Capital.

That doesn’t close til December 19, and in order to get the stock to a place where it even covers the US$0.43 (CAN$0.56), a whole lot of buying had to be done over the last few days. I’d expect someone is working hard to keep MMEN stock at this price til Dec 19 or the deal will be repriced or canceled, but maybe that’s just a coincidence.

Hey, great. What else?

On November 27, 2019, the Company closed on an additional US$10 million under the [Gotham Green] Facility.

Actually, the November 27 MedMen release stated, “As part of the amendment to the company’s $250-million senior secured credit facility, Gotham Green Partners has an obligation to finance the $10-million tranche by Nov. 29, 2019.”

An ‘obligati0n’ isn’t really ‘support’, though Bierman is trying to make it appear Gotham Green sees wonderful things happening at MedMen and was all falling over itself to hand them millions more. We’ll agree to disagree, though it makes for interesting reading to see the terms originally demanded by Gothan Green when they took out this deal.

Regardless of whether you care or not about what it cost for MedMen to receive this financing, those two deals come to a total of $37m of the $60m or so they’ll still need another $23m to cover the vig.

Have no fear! Part of what they needed that money for has been booted down the road a few years!

On December 10, 2019, the Company executed a binding term sheet in respect of certain amendments to the definitive agreements for the US$78 million senior secured term loan (“October 2018 Loan”) with funds managed by Stable Road Capital and its affiliates (“Term Loan Lenders”). Among other amendments, it is contemplated that the terms and conditions of the October 2018 Loan will be amended as follows:

- The maturity date will be extended from October 1, 2020 to January 31, 2022

Amazing! When Bierman bragged of the ‘strong level of support’ of his financiers, he wasn’t lying. What support!

Oh wait, there’s more…

- To reflect current market conditions, the interest rate will be increased from a fixed rate of 7.5% per annum, payable monthly in cash, to a fixed rate of 15.5% per annum, of which 12.0% will be payable monthly in cash based on the outstanding principal and 3.5% will accrue monthly to the principal amount of the debt as a payment-in-kind

Double interest. OOF.

The Company will cancel the existing warrants issued to the Term Loan Lenders, being 16,211,284 warrants exercisable at US$4.97 per share and 1,023,256 warrants exercisable at US$4.73 per share, and issue to the Term Loan Lenders a total of 40,455,729 warrants exercisable price of US$0.60 per share until December 31, 2022, representing 31% of the loan amount. The warrants to be cancelled represent 100% of the loan amount.

This is how the wealthy stay rich, because even when they completely fuck things up and lend a trainwreck company tens of millions when they’re at the peak of their overvaluation, they only have to wait for said company to get desperate enough that it will hold its ankles happily, gifting them a repricing that will ensure the lender can’t lose.

Of course, you bagholders can lose. But the lenders won’t.

Understand, MedMen homers, after all this borrowing, should MedMen ever go to liquidation, the founders get first stab at whatever is recovered, then the lenders get the rest.

YOU WILL RECEIVE NOTHING.

MedMen pays for storefronts that aren’t legal to open yet. It pays for storefronts that are legal but can’t ever possibly cover their rent. It pays for billboards everywhere and radio ads in markets they don’t exist in and, OMG, did you hear their dispensaries look like Apple Stores? I just got lunch at an A&W and you know what it looked like? A fucking Apple Store. Everything looks like Apple Stores these days. The Equity.Guru office lobby looks like an Apple Store. I’ve taken very comforting shits in places that could accurately compared to Apple Stores.

If you ran your home mortgage this way, you’d be paying double interest for 50 years and your children would petition for guardianship of you because you clearly can’t be trusted to handle your own affairs. Frankly, I suspect if MedMen management received a phone call from Nigeria asking for their bank account details in return for ‘an exclusive license for 20 dispensaries in Abuja’, they’d have a news release set to go before lunch and be sending an intern to Western Union with a check for $30k.

In short, MedMen is the Alzheimer patient of cannabis companies. It’s the old lady with a sequined fedora holding up the line at the 7/11 while she buys $500 in scratchie tickets. It’s the guy on a scooter with his dog in the grocery basket, buying 87 Beanie Babies on the Home Shopping Channel because they come with a certificate of authenticity.

MedMen is the mark. It’s the dumbest guy at the table.

…Except if you buy some.

— Chris Parry

FULL DISCLOSURE: How’s that lawsuit, Adam?

You nailed it again Chris Parry!! Well done and thank you for keeping on top of the trash:)

Bingo.

In the end, it should become a novel for got shit reading.

Love it.

Alot of us folks like the line of products and design keep your short selling to yourself. When you told us to buy supreme at 1.70 you were wrong now you will be wrong again.

Sure, you go ahead and put your mortgage on MMEN. Show me what’s up.

MMEN up 30% since you posted this.

I’m guessing you’re one of those guys that would rather be “right” than make money.

It’s obviously due for a pullback, but will it pull back enough for you to cover your short position?

Also, can you do a story like this on VIVO or FIRE? You know…. Those companies you used to pump endlessly that are now huge piles of burning $hit.

No short position, but obviously it will pull back and more fans will be burned.

I haven’t written about VIVO in four years, but am buying Supreme. Thanks for your concern.