Risk versus Reward? Ideally, the greater the risk, the more satisfying the outcome (the greater the reward)…

The junior mining sector is fraught with risk. Most of us already know that. The reward can be weighty though. It’s for this reason we toss bids into these auction arenas.

Mitigating the risk…

When I run due diligence on a company, I always look for ways to mitigate the risk side of the equation. Making sure management is competent is one way, e.g. I’d rather see a Ph.D. in geology than a certificate from Le Cordon Bleu in my CEO.

I remember running due diligence on an interesting tech company back in the late 1990’s. It was interesting right up until I homed in on the CEO’s resume. His claim to fame was decade-long gig running a janitorial company. Don’t get me wrong, I have heaps of respect for hardworking custodian types, but here, I would’ve preferred a CV highlighting a senior position at JPL (Jet Propulsion Laboratory).

Other ways to mitigate risk: make certain the region being explored/developed is in a mining friendly jurisdiction, surrounded by locals immersed in the culture, supported by a gov’t that appreciates the processional benefits development can bring.

One more risk mitigating exercise: DIG. With a bit of probing, and a little luck, you might expose a serious inefficiency in the market, e.g. If Company A sports a deposit with similar economics to Company B, but A is trading at a significant discount to B, you might have unearthed a potentially profitable market anomaly.

If additional due diligence fails to expose any fatal flaws in Company A, your anomaly could pay off handsomely in the end.

Cypress Development (CYP.V) strikes me as one potential anomaly in the lithium space. It may well be substantially mispriced compared to its peers.

First, the lay of the land…

Clayton Valley is CYP’s flagship project. The property is located immediately east of Albemarle’s Silver Peak mine.

Recent exploration in the area has identified an extensive deposit of lithium-bearing claystone.

Clayton Valley is situated in what’s known as an Endorheic Basin. These settings are characterized by limited drainage – no outflow to rivers or other external bodies of water. Runoff from higher elevations is trapped within the topography of the basin. The standing water in the seasonal lakes and swamps equilibrate only through evaporation or seepage. The ideal environment for a lithium deposit.

Clayton Valley highlights:

- CYP controls two claim blocks, Dean and Glory, totalling 4,200 acres.

- 100% owned (3% NSR which can be reduced to 1% for $2 million).

- Orebody is flat lying with no overburden (can’t stress enough how hugely important this feature is to the economics of a project).

- Extensive geological setting is volcanic-derived.

- Lithium is contained in illite and montmorillonite soft clays to a minimum depth of 120 meters below surface.

- No drilling or blasting required to exploit this deposit (again… hugely important).

- Region is steeped in mining history – ample access to experienced labor and contractor services.

- A mature regulatory environment.

- THE best mining jurisdiction in the U.S.A. – ranked 3rd globally by the Fraser Institute’s annual Survey of Mining Countries.

- Good road access through and through.

- Rail system access is 90 miles by road.

- Close proximity to airport in Tonopa.

- Easy access to power – electrical connection possible via the sub-station in Silver Peak.

- Water is available via the Silver Peak municipal water supply.

The resource:

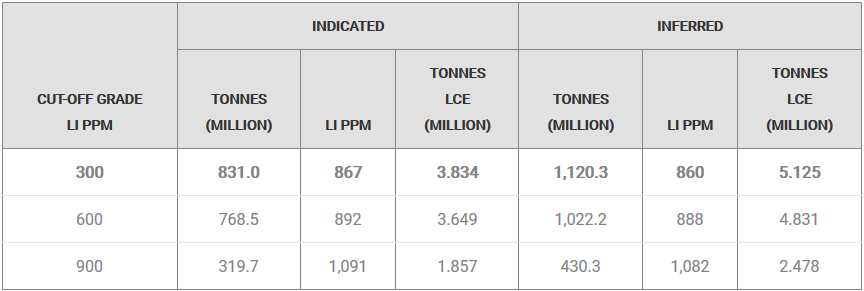

Independent engineering firm, Global Resource Engineering (GRE), prepared a property-wide resource estimate for Clayton Valley outlining nearly 2 billion tonnes of claystone material:

- 3.835 million tonnes of lithium carbonate equivalent (LCE) contained in 831 million tonnes of material at an average grade of 867 ppm Li in the Indicated category.

- 5.126 million tonnes of LCE contained in 1.12 billion tonnes at an average grade of 860 ppm Li in the Inferred category.

It took only 2,000 meters of drilling to delineate this resource. Less than $1M was spent bringing Clayton Valley to the PEA stage (see below).

The deposit remains open at depth – 21 of 23 drill holes ended in lithium mineralization.

Grade continuity is excellent across the entire deposit.

Only 10 additional drill holes (maximum) will be required to upgrade and increase the confidence in this resource… to convert indicated material to the measured category, inferred material to the indicated category.

Where the rubber meets the road – the PEA.

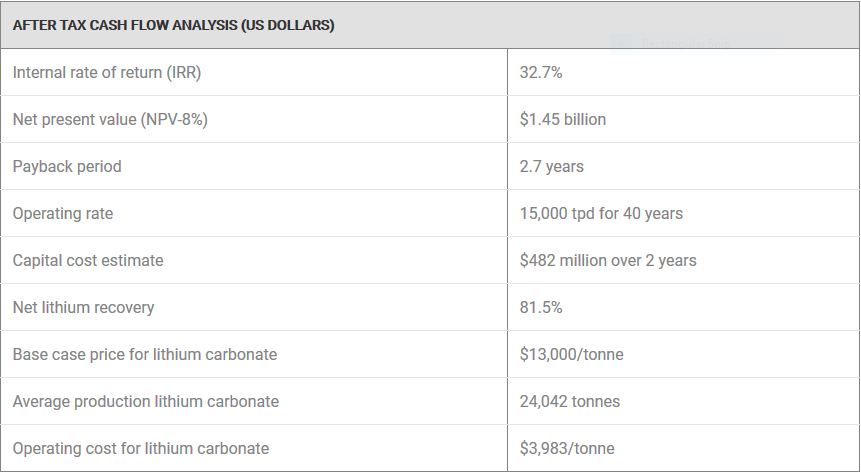

Last month, CYP announced results from a Preliminary Economic Assessment (PEA):

Highlights from this PEA include:

- Net present value of $1.45 billion at 8% discount rate

- An internal rate of return (IRR) of 32.7% (after tax).

- Average annual production rate of 24,042 tonnes of lithium carbonate over 40-year mine life.

- Capex of $482 million, pre-production and operating cost estimate averaging $3,983 per tonne of lithium carbonate.

- An estimated 2.7 year payback period.

It took only 2 years, from the first hole drilled to the release of this PEA. That’s extraordinary. It speaks to the experience and competence of this management team.

Lending validity to the PEA – metallurgy, extraction and recovery…

Early on, it was discovered that by raising the temperature and using a stronger leaching cocktail – sulphuric acid – Clayton Valley’s ore was leachable.

Highlights…

- Low acid consumption at 125 kg/t.

- 2 to 8 hours agitated leach time.

- 81.5% extraction rate indicating that the dominant lithium-bearing minerals present are not hectorite, a refractory clay mineral which requires roasting to liberate the lithium.

- Standard treatment with lime adjusting pH to low impurity solution.

- Recovery to battery grade product on-site.

During the course of the PEA it was discovered that Clayton Valley’s ore also contained rare earth element (REE) values – Scandium, Neodymium, and Dysprosium. Though these values were not incorporated into the PEA, the impact on the project’s economics could be significant. Details pending.

As noted in the above PEA, the project sports an after-tax IRR of 32.7%.

These are compelling numbers.

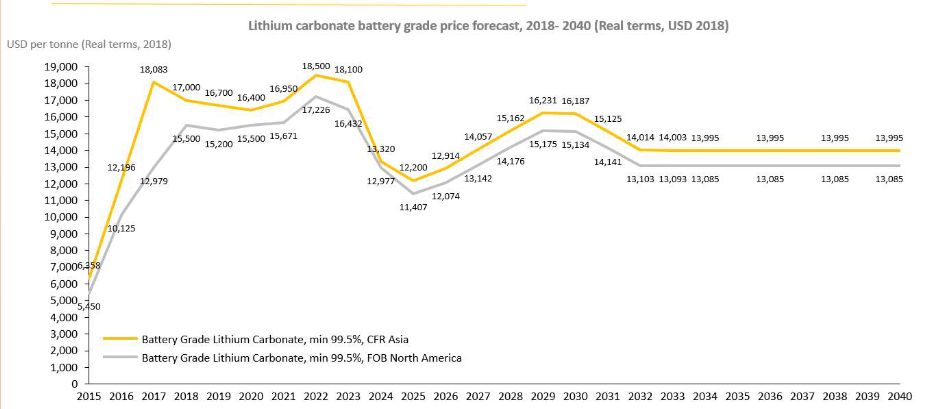

The base case price lithium carbonate used in this study was $13,000 per/tonne, which is in line with the lithium carbonate price trend chart below…

What’s more, these numbers compare well with economic studies covering other claystone deposits under development – Lithium Americas ‘Thacker Pass’ project and Bacanora Lithium’s ‘Sonora’ project.

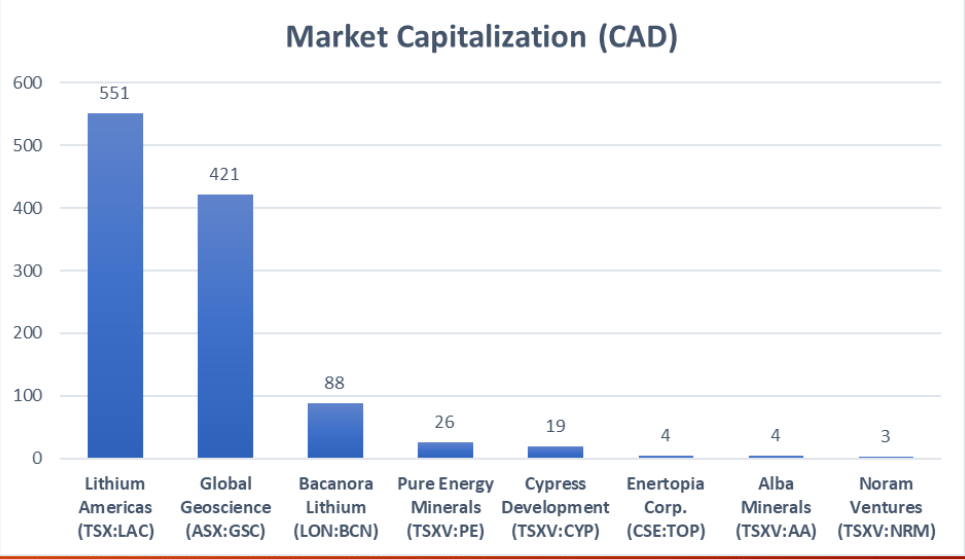

What doesn’t compare well is CYP’s valuation. And herein lies the anomaly I was hinting at in the intro.

Lithium Americas, Global Geoscience, and Bacanora Lithium sport market-caps many multiples higher than CYP’s.

Something appears out of whack here. Either the larger cap companies are way overpriced, or CYP is way undervalued. The latter suits my best guess.

Based on the company’s 62.4 million shares outstanding, the company’s market-cap currently sits at a very modest $14.3 M.

Final Thoughts…

The battery metals story, the push toward a greater reliance on electric vehicles, isn’t going away anytime soon. If you acknowledged the story a few years ago, your conviction should be firmly entrenched by now.

If it was a good time to buy battery metals stocks yesterday, it makes even more sense today.

Cypress management continues to push Clayton Valley along the development curve. Just last week the company began a Prefeasibility Study (PFS) on the project. A PFS is more detailed than a PEA and will fine-tune the project’s economics. It will also set the stage for the permitting process via baseline studies.

This is a busy company developing a lithium project boasting robust economics in a top shelf mining jurisdiction. With a current market-cap of a mere $14.3M, Cypress Development is a worthy shortlist candidate.

END

~ ~ Dirk Diggler

FULL DISCLOSURE: Cypress Development is an Equity Guru client. We own the stock.