EDITOR’S NOTE: We believe, this year, resources will make a pretty hard move, just as cannabis and blockchain did in 2017, and because many of our investor readers are new to the mining space, we decided to bring aboard a writer who can dig deep into the details and explain what matters and why.

Greg Nolan, AKA Dirk Diggler, is a fount of mining knowledge. His brief: Take a look at mining and oil and gas explorers and producers, and tell us what he feels, positive or negative, with no fear nor favour.

We encourage readers, if they come across a phrase or concept that they don’t understand, to let us know in the comments, as we’re putting together a series of pieces that will explain terminology in greater detail. See more of Greg’s work here.

—

What do Pope Francis and Cuban Revolutionary, Ernesto Che Guevara, have in common? Why, they both hail from Argentina. They have even more in common than one might expect – the supreme pontiff also worked as a bar bouncer in Buenos Aires when he was younger. Cool beans!

Aside from spawning great revolutionaries and spiritual leaders, Argentina has also produced some truly astonishing footballers. And Argentinian sports fans know how to support their heros:

- Soccer legend Diego Maradona is the only athlete on the planet who has his own religion and church, one created by his fans where he’s worshiped as a god.

- Lionel Messi may be the greatest footballer of this generation. Authorities in Rosario, Messi’s hometown, have banned parents from naming their children after the legend, fearing it might cause too much confusion for the locals.

One aspect I find particularly appealing about Argentina: its capital, Buenos Aires, houses more psychoanalysts and psychiatrists than any other city in the world. It even has its own psychoanalytic district called “Ville Freud.” My kind of town!

The name Argentina comes from the Latin word for silver, argentum. And it’s on the subject of silver that I found myself taking a close look at Golden Arrow Resources (GRG.V). GRG is all about Argentina… and argentum.

It’s easy (necessary) to dismiss the aspirations of overzealous junior exploration ceo’s, those who are determined to make the leap from explorer to producer, as sheer madness. It’s difficult to take them seriously. I’ve watched too many of these over-ambitious biz-models blow apart at the seams. All too often the company fails to execute. It can’t negotiate the transition from rock-kicker to mine-builder. It then becomes a serial diluter, blowing out its capital-structure, ushering in a downward spiral of endless equity financings and share rollbacks. The process can be absolute torture for loyal, devoted shareholders.

GRG appears to have made that leap, attaining the rank of producer while still maintaining a fairly tight cap-structure. The manner in which it has done so is admirable. It had some help.

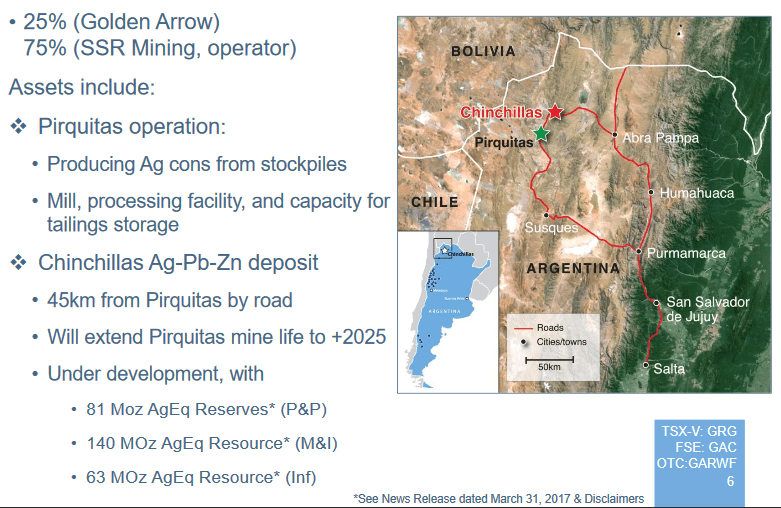

Long story short, GRG formed a joint venture with SSR Mining (SSRM.TSX), one which combines the two companies assets into a single entity. The name given to this business combination is ‘Puna Operations Inc’. It’s a marriage that makes sense: SSRM has run out of ore to feed its mill and processing facility at its Pirquitas mine site located in Jujuy Province, Argentina – just down the road GRG has a large silver, zinc and lead deposit in need of a mining facility. It’s a good marriage. It’s win-win.

Puna Operations is owned 75% by SSRM and 25% by GRG (SSRM is the operator). The benefits to GRG, having given up 75% of the Chinchillas project, are immediately apparent:

- GRG received an upfront US$15 million payment from SSRM representing 25% of Pirquitas mine earnings (less certain expenditures) from October 1, 2015. These funds were deposited into GRG company coffers in mid 2017.

- GRG Immediately benefits from cash flow generated by the currently producing Pirquitas Mine. Though SSRM have ceased digging ore out of the ground at Pirquitas – mining activity concluded in January 2017 – there are stockpiles on the surface which will continue to produce silver until mid 2018. GRG is entitled to 25% of net earnings from the processing of these remaining stockpiles.

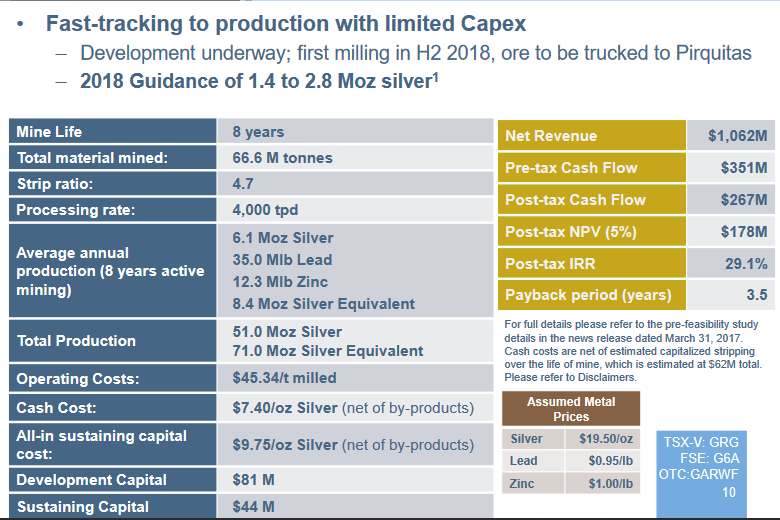

- The joint venture provides GRG with an opportunity to fast-track development of their Chinchillas project, in a capital efficient manner, through the use of the existing production facilities already in place at the Pirquitas Mine. The first ore from Chinchillas is scheduled to be delivered to the Pirquitas mill in the second half of 2018. The operation will continue to ramp-up through the remaining months of 2018.

- Their Chinchillas deposit is in good hands – the operation will be managed and overseen by SSRM’s highly skilled operational management team, a crew with extensive mine construction and operational expertise. This allows GRG management to focus on what it does best: exploring its extensive portfolio of exploration projects, its sights set on making a new discovery.

The Chinchillas Resource:

- Mineral Reserves of 11.7 million tonnes containing 58 million ounces of silver at a grade 154 g/t, 310 million pounds of lead at a grade of 1.20% and 127 million pounds of zinc at a grade of 0.49%.

- Measured and Indicated Mineral Resources (inclusive of Mineral Reserves) of 29.3 million tonnes containing 96 million ounces of silver at a grade 101 g/t, 581 million pounds of lead at a grade of 0.90% and 386 million pounds of zinc at a grade of 0.60%.

The Chinchillas plan:

- Average annual silver equivalent production of 8.4 million ounces over an eight-year mine life at a 4,000 tonne per day plant throughput.

- Robust operating margins based on cash costs of $7.40 per payable ounce of silver sold over the life of mine.

- Post-tax net present value of $178 million using a 5% discount rate and metal prices of $19.50 per ounce silver, $0.95 per pound lead and $1.00 per pound zinc.

- Attractive post-tax internal rate of return of 29%.

As Brian McEwen, VP of Exploration, noted in his presentation at the November 2017 Silver and Gold summit in San Francisco, there may be greater efficiencies to be had than the above numbers suggest (ie) plant throughput has been running closer to 5,000 tonnes per day in recent months, rather than the 4,000 number used in the study.

The Chinchillas Study (PFS):

Shrewd observers might detect a discrepancy in the above numbers via an overly optimistic silver price. This is usually a big red flag, one which often causes me slam the book shut on further study; but this apparent unbridled enthusiasm is completely offset by sufficiently understated Pb and Zn prices (Zinc is currently trading at a hefty $1.58 per lb, Lead at $1.15). Moving along….

The $81M Capex is modest for the development of a resource this size. The infrastructure SSRM has established in the area is the main contributing offset. Though GRG is obliged to pony up its share of development costs, there is an agreement in place which limits its commitment to $10M in the first year.

The aisc of $9.75 per oz of silver (net of Zn and Pb by-products) demonstrates robust economics. Of the $178M shown under ‘Post-tax NPV’, approx $45M has GRG’s name on it. If you believe, as I do, that silver prices are due for a significant adjustment to the upside, this mine could become a serious cash cow.

Ore is expected to begin feeding the Pitriquas mill in H2 of this year. When the mine reaches commercial production, it’ll send approx 2 million silver equivalent ounces GRG’s way on an annual basis. That’s up to $15M in free cash-flow annually.

I’d be remiss in neglecting to mention that the Pirquitas deposit may not be completely exhausted. Aside from the potential for regional exploration upside at both Pirquitas and Chinchillas, there remains an underground resource at Pirquitas that SSRM is currently evaluating. It’s high grade rock. It’s a resource (indicated and inferred) of some 19 million ounces of silver at a grade of > 200 g/t, plus zinc credits running > 5%. If the economic study on this high grade resource rings positive, the plan is to blend the ore with lower grade material from the Chinchillas deposit. This small, understated detail could yield fat results if the numbers prove beneficial.

This is the part I like:

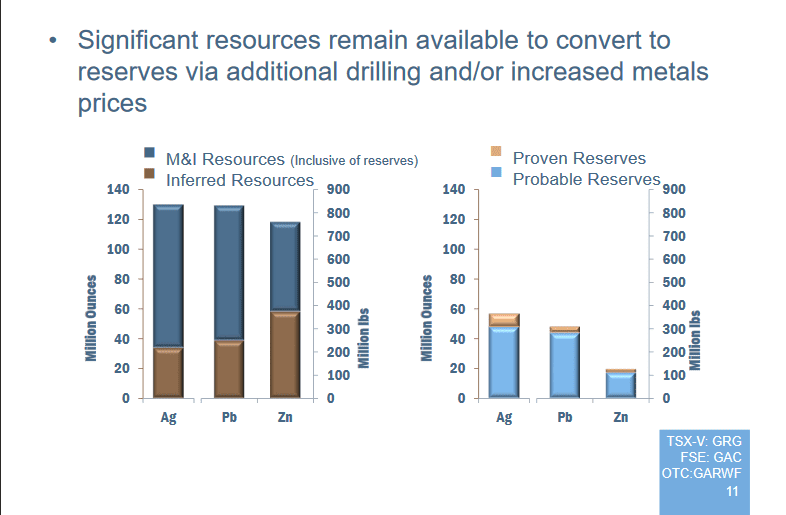

Though the PFS envisages an 8 year mine life, there’s potential life beyond that. In the above pic, the chart on the right illustrates the mineral reserve that has been factored into the current mine plan. The chart on the left demonstrates a resource that could extend the mines life, via confirmation drilling and/or higher metal prices, well beyond its current 8 year lifespan.

[youtube https://www.youtube.com/watch?v=KwLoRi5vy8Q]

DONE! “On The Shelf”:

Now that Chinchillas is in the very capable hands of SSRM – promising to spin off heaps of free cash-flow in the coming months/years – GRG management can now focus on what it does best: EXPLORE.

Exploration:

GRG’s exploration arm is ‘New Golden Exploration Inc’. A GRG subsidiary, it is responsible for running an exploration portfolio encompassing some 200,000 hectares of geologically prospective terrain.

New Golden has been structured to allow for a public spin-out – an IPO is in the works (GRG will remain a majority shareholder). This is a smart move by management imo as it preserves GRG’s capital, setting up the possibility for new acquisitions – this is merely speculation on my part.

The Exploration Projects:

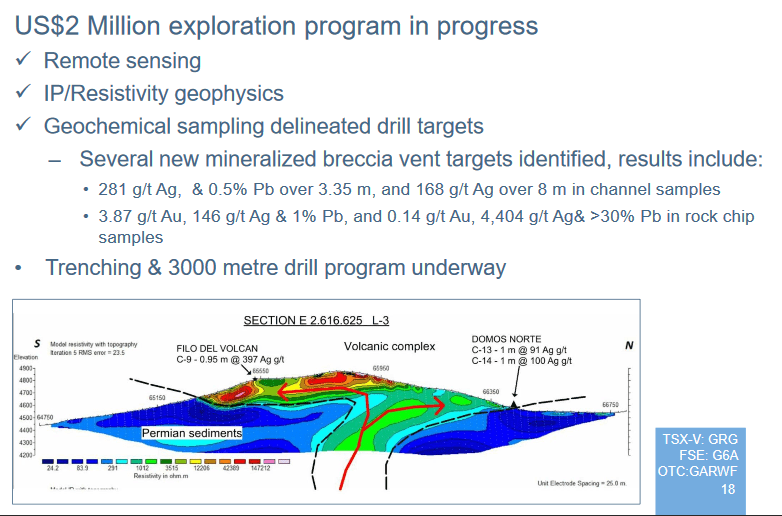

Antofalla encompasses some 8,760 hectares in Catamarca Province. There’s potential here for the discovery of world class silver-gold-base metal deposits, both epithermal and porphyry types. Bearing strong similarities to Chinchillas, it sports a large footprint, a 4 by 5 km zone of hydrothermal alteration. Drilling is currently underway with a 3,000 meter program.

San Juan Exploration Projects:

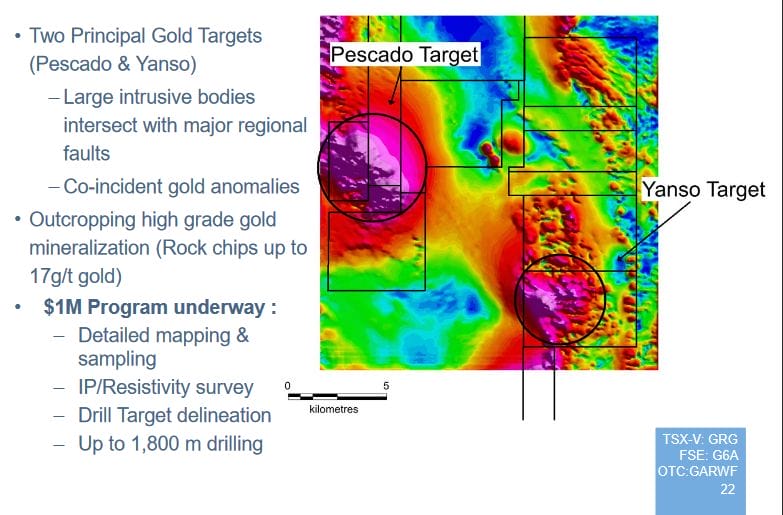

There are 3 projects under this banner. All 3 are in the vicinity of operating mines or known mineralized trends. The targets are for gold, copper and silver epithermal and porphyry type deposits.

There’s potential for multi-million ounce gold deposits here in 2 target areas. The property is 10 kms from Yamana Gold’s Guacamayo Mine which has a resource of 2.8 million ounces of gold. A $1M exploration program, which includes up to 1,800 meters of drilling, is currently underway.

The Potrerillos Au-Ag and Mogote Cu-Au-Ag projects:

Potrerillos is a 5,748 hectare property in the Valle de Cura district. This gold-silver project is located in the world-class El Indio gold silver belt, only 8 km east of Barricks’ Pascua-Lama-Veladero project (27.9 Moz Proven and Probable gold equivalent reserves). There are a number of drill-ready targets on this geologically prospective property. The setting is for epithermal style gold deposits. GRG is seeking a joint venture partner for this one.

Mogote is comprised of some 8.800 hectares. This area is considered to be the southern extension of the Maricunga Gold-Copper Belt, as well as the geologic bridge to the El Indio Gold Belt to the south. The region is host to world-class porphyry and epithermal deposits which include: El Indio-Tambo (10 million ounces gold production, reserves and resources), Pascua-Lama-Veladero (27.9 Moz Proven and Probable gold equivalent reserves) and Marte/Lobo (6.1 million ounces of Proven and Probable gold reserves). GRG is a seeking a jv partner for this one as well.

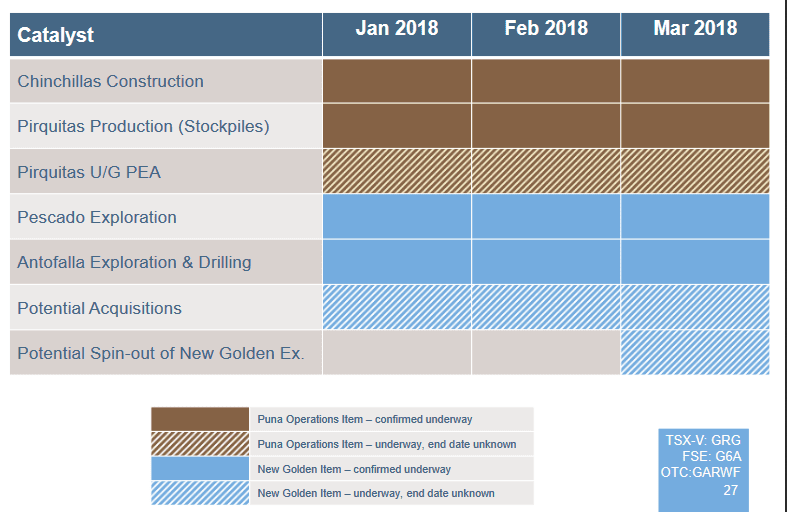

Catalysts:

This is one of the more dynamic companies I’ve come across in the junior exploration arena. There are a fair number of moving parts and management appears to be hitting on all sixes.

What impresses me most about this company is their success in having bridged the abyss between ExplorerCo and Producer, without blowing their cap-structure all to hell. There is always luck involved in this game, but management deserves heaps of credit for what it’s managed to pull off. It should come as no surprise that Golden Arrow has been acknowledged as one of the mining sector’s top performing companies.

Cap-structure and other stuff:

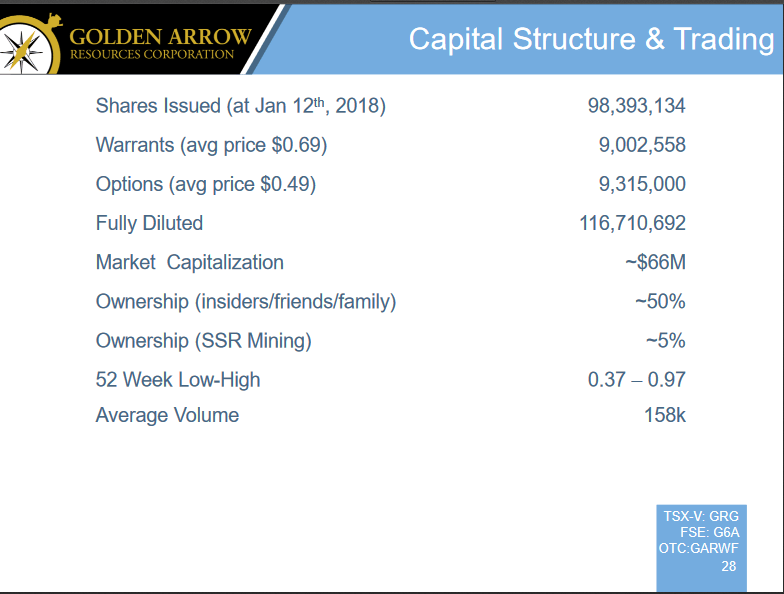

Again, GRG’s cap-structure is very respectable for a junior producer. Based on shares outstanding and its recent trading range, it sports a market-cap of approx $55M.

If all warrants and options are exercised, another $10.7M gets added to GRG’s coffers. The company is currently sitting on approx $16M in cash. No debt.

Judging by the level of insider ownership, management has ample skin in the game, as does SSRM who own 5% of GRG’s outstanding shares.

Final thoughts:

The bear market of the last 6.5 years has been cruel to investors in the precious metals arena. The rout was also a nasty one for producers’, forcing many to dramatically scale back exploration spending. This has lead to a dearth in new discoveries. Without a steady stream of new discoveries on its books, producing companies are depleting their reserve bases at a rapid rate. The situation could become desperate. Every junior company that boasts a significant new discovery, or economic resource, has a bulls eye on its back…. especially those operating in mining friendly jurisdictions like Argentina.

With bond yields and equity prices all over the map, one would think that gold and silver would launch significantly higher from current levels. My guess is that it WILL happen, once investors figure out that precious metals, particularly the companies that produce them, offer decent value when compared against general equities.

Companies like Golden Arrow appear to have all of their ducks in a row – it could outperform in the coming months based on its 25% interest in Chinchillas alone. If GRG management are successful in delivering yet another new discovery (or acquisition) to shareholders, the market will take notice.

End.

— Dirk Diggler

FULL DISCLOSURE: Golden Arrow has no commercial connection to Equity.Guru and is not a client, nor do we own stock in the company. Yet.