Some companies have trouble telling their story in a pair of sentences. I’ll often ask a CEO to tell me his or her ‘elevator pitch’ – the story he’d tell someone about his company while sharing an elevator to the 20th floor – and half an hour later they’re just getting to the good bit.

Ceylon Graphite (CYL.C) is easy to summarize.

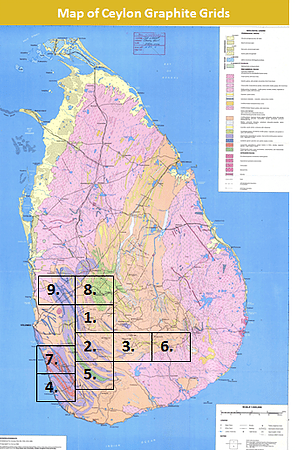

They have the rights to most of Sri Lanka’s known government-held graphite resources, excluding mines already in production, They own a pair of drilling rigs, so they can drill all day, every day, at minimal outlay. And they have exploration licenses on 49 of the most productive areas in that package. To dig any graphite out will be extremely cheap when compared to North American sources, and the government would love as much activity going on there as possible.

That’s the pointy end.

You can add some things to the tale that make it more appealing: Graphite is a major industry in Sri Lanka, but the government hasn’t historically known how to handle it themselves. Graphite is in much demand in North America, where we want it for batteries, which are in increasing demand, but we don’t actually mine it here. And Sri Lanka’s graphite is ridiculously high in grade, as evidenced by activities going on to try to get at graphene elsewhere in the country.

So what’s going against it?

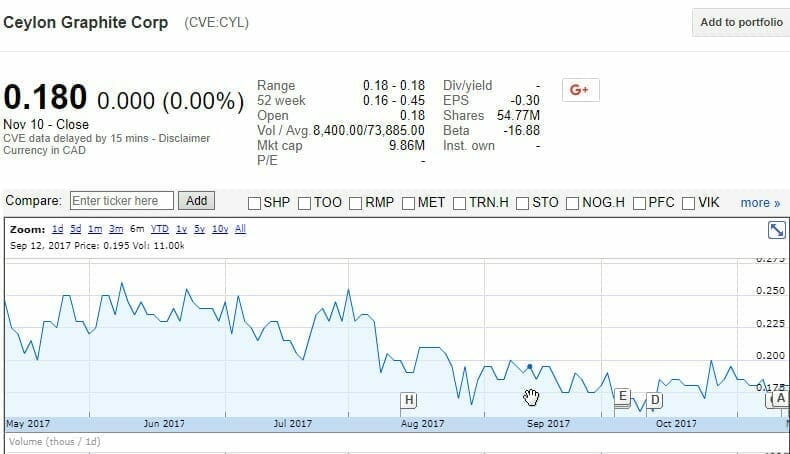

The market. Ceylon Graphite opened its listing at around $0.26, got to around $0.45, but couldn’t sustain itself and eventually drifted to the $0.18 range, where you’ll find it now.

Now, you could see that as a massive downside, sure. It’s not a positive sign when a company is at its low.

But there’s another way to view that; If a company is going to take some time positioning itself and preparing to do real business, a scammy marketing play will chuck out all manner of news to keep the share price inflated. A real business will focus on real business, and if there’s no news to be had because it’s the wet season and no drilling is happening, well it’s on you if you don’t have the stones to stick around when the share price drifts.

Ceylon Graphite, today, is the best deal it’s ever been. The drilling is now kicking in, the share price is as cheap as ever, and they’re not putting out spammy pumpy news pieces.

Ceylon Graphite is expected to take delivery of the [second drill] rig in late November, 2017, with the view of having it operational by early December, 2017. The rig will be used to conduct drilling programs at grids held by Ceylon Graphite to confirm the quality and quantity of the graphite mineralization. It is expected that the rig will drill a minimum of 10 to 12 metres a day. With two operating drilling rigs, Ceylon Graphite anticipates being able to drill an additional three to five grids by the end of the first quarter, 2018.

Upon completion of the drilling program, and provided the results of the program are favourable, Ceylon Graphite intends to apply for a Class B mining licence, with the ultimate goal of establishing mining operations.

You’ve still got time to stand around and watch, waiting for the first metres of drilling to happen, and maybe in doing so this thing will drift to $0.16 or less. But maybe the smart money has been waiting and watching, looking for that moment when they can see news is coming, but the market hasn’t factored it in.

We call that Moneyballing. The market reacts after the front runners make their move, and looking at this chart, and the most recent news, I think this is the golden zone on CYL’s timeline, before the news starts to drop and the low volume brings high volatility – hopefully in an upward direction.

Between May and October, if you were waiting for news from Ceylon, you were crap out of luck. But Ceylon hasn’t been dormant by any stretch; they bought a private Sri Lankan mining concern last month, which brought them five additional graphite exploration permits, which isn’t something you do if you don’t plan to actually do the work. With those permits cam historical records for over 30 drill holes already done. They also brought on a new General Manager of Operations.

More important were the words of the CEO [emphasis mine]:

Bharat Parashar, Ceylon Graphite’s Chief Executive Officer, said: “We welcome Janaka to the Ceylon team, his experience and leadership will greatly strengthen our operational capabilities. We are progressing as per plan albeit a little slower than anticipated due to heavier than expected monsoons. Despite this delay, we expect to enter a production phase by the end of the calendar year. We anticipate that the acquisition of JADS will provide Ceylon with a more substantial resource base and positively impact both the quantum of graphite we will bring to the market and our production time lines.”

To be sure, it’s not the time to throw your pension money on the line. There’s risk inherent, and not an inconsiderable amount. But a side bet of dough that you can live without for a few months might not be a bad option as it appears the engine is beginning to kick over.

Sri Lanka is a cheap place to do business, and the government dearly wants someone to come in and make mines happen so that it doesn’t need to do so itself. Ceylon has been dubbed ‘the one’, and is overdue for a news burst.

If it happens in the next few months, y’all owe me beer.

— Chris Parry

FULL DISCLOSURE: Ceylon Graphite is an Equity.Guru marketing client.